Summary

- MLP yields of ~7% are backed by positive dividend trends and fee-based businesses that generate stable cash flows.

- Beyond income, MLPs provide diversification benefits, real asset exposure, and more defensive energy exposure.

- MLPs are expected to continue generating free cash flow and returning excess cash to investors through distribution growth primarily but also through opportunistic buybacks.

Master Limited Partnerships (MLPs) are an overlooked investment category that offer notable portfolio benefits headlined by healthy yields around 7%. MLPs have seen standout performance in recent years helped by solid free cash flow generation and a focus on returning excess cash to shareholders — tailwinds that are expected to continue. Today’s note provides a brief overview of the investment case for energy infrastructure MLPs using the benchmark Alerian MLP Index (AMZ), which was the first real-time MLP index.

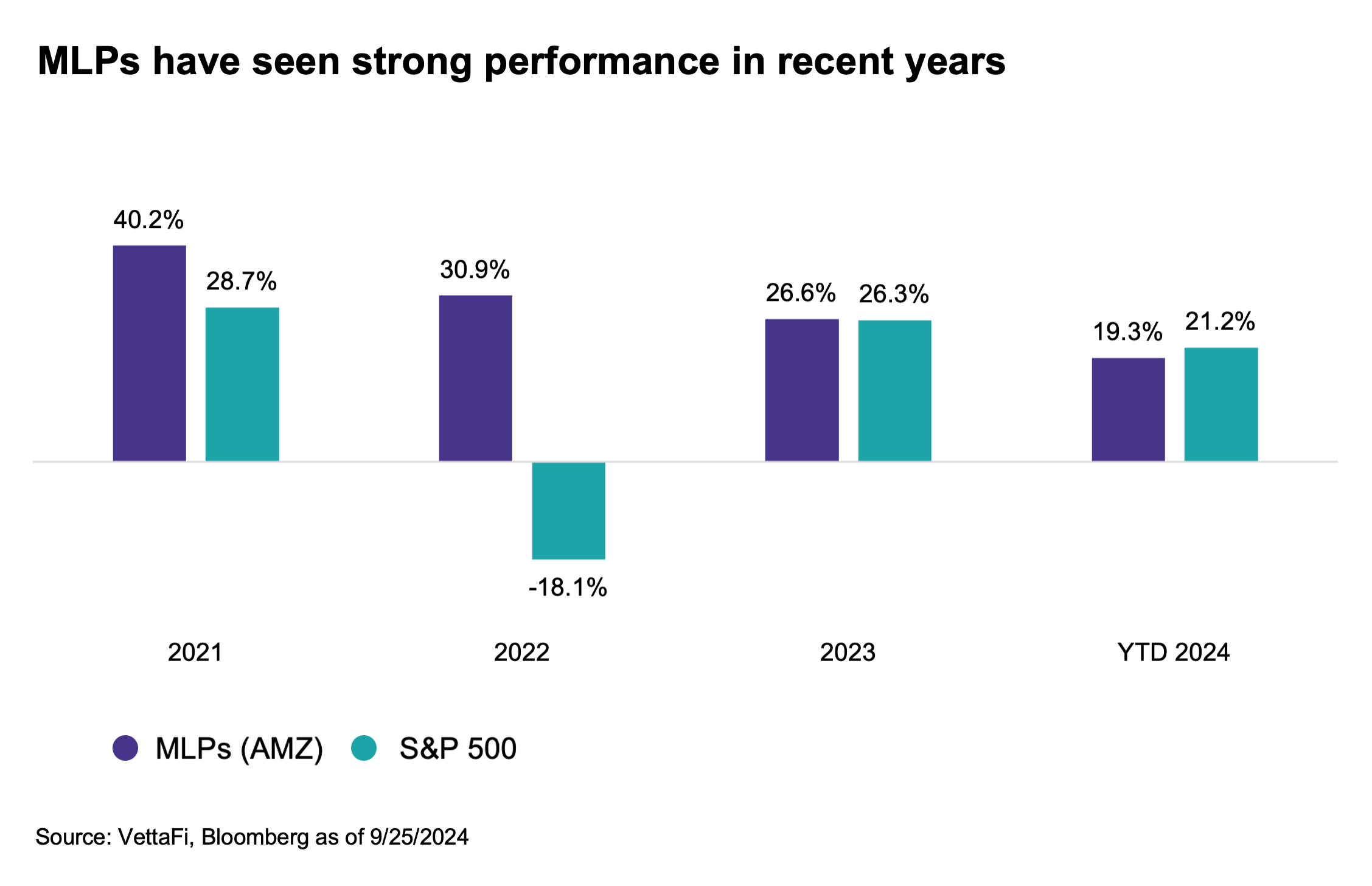

MLPs Outpace the S&P 500 and Even Tech

Despite strong performance in recent years, MLPs tend to fly below the radar of most investors.

MLPs have outperformed the S&P 500 for three straight years (2021, 2022, and 2023) and are neck-and-neck with the benchmark so far this year. MLPs have even outperformed the information technology sector since the end of 2020. They continue to offer attractive qualities for income and equity portfolios.

MLPs Are Known for Their Income

MLPs have historically been known for their yield. Due to their special tax treatment (read more), MLPs do not pay taxes at the entity level, which has in part supported generous dividends. Additionally, energy infrastructure MLPs provide services for fees under long-term contracts and generate stable cash flows. These services include transporting hydrocarbons through pipelines, storing hydrocarbons, loading ships for export, and processing natural gas for example.

MLP dividends (called distributions) are supported by stable, predictable cash flows. As of Sept. 27, AMZ was yielding 7.0%. With companies largely generating free cash flow, distribution trends for MLPs have been strong in recent years. Based on distributions paid in 3Q24, over 80% of AMZ by weighting has grown its payout within the last year (read more). It also bears mentioning that 64.5% of AMZ by weighting as of Sept. 25 has a buyback authorization in place. Aggregate buybacks from constituents in 2Q24 totaled $165 million.

MLPs Offer Other Portfolio Benefits

Beyond attractive income, MLPs offer other portfolio benefits. MLPs can enhance the diversification of a portfolio given that MLPs are typically excluded from major equity market indexes like the S&P 500. The AMZ has a 10-year correlation with the S&P 500 of 0.5. MLPs also have low correlations with other income investments. AMZ’s 10-year correlation with REITs and utilities is between 0.3 and 0.4. The 10-year correlation with bonds is near 0.

MLPs also offer real asset exposure, which was beneficial in recent periods of elevated inflation. Additionally, MLPs’ long-term contracts often include annual inflation adjustments. When inflation is elevated, as seen in 2021-2023, MLPs tend to outperform the broader market.

Investors can also use MLPs for an energy equity allocation. MLPs tend to be more defensive than other energy subsectors, because their fee-based businesses mitigate their exposure to commodity prices. This defensiveness can be attractive in the current backdrop given a tempered outlook for oil prices and current weakness in natural gas prices (read more).

Why Allocate to MLPs Now?

Although MLPs have seen strong performance in recent years, the investment case remains compelling. Companies are expected to continue generating free cash flow and returning excess cash to investors through distribution growth and opportunistic buybacks. Lower interest rates make MLPs’ generous yields all the more attractive.

Additionally, MLPs are well-positioned to benefit from the expected growth in U.S. natural gas demand and production related to liquefied natural gas exports and power demand (read more). Midstream can be an ideal way to play this long-term trend given healthy income and relative insulation from price volatility in natural gas. Approximately 57.0% of AMZ by weighting is primarily focused on natural gas infrastructure.

With strong performance, investors may be cautious about valuations, but they have not become stretched. AMZ’s weighted average forward EV/EBITDA multiple was 8.7x as of Sept. 25 using Bloomberg consensus estimates for 2025. The 10-year average for energy infrastructure MLPs is approximately 10.0x. For additional context, as of Sept. 25, AMZ was trading ~45% below its all-time high from 2014.

MLP Investing Basics

Investors who own individual MLPs directly will receive a Schedule K-1. But investors can access MLPs through exchange-traded products and other vehicles to receive a Form 1099 (read more). AMZ is the underlying index for three exchange-traded notes (ETNs), including the largest MLP ETN, the Alerian MLP Index ETN (AMJB). ETNs are unsecured debt obligations of a bank, which agrees to pay the return on a specified index less fees.

Relative to other investment vehicles, the advantage of ETNs is their minimal tracking error, which can be desirable for investors who expect MLP stock prices to increase materially. Energy infrastructure ETNs typically pay a quarterly coupon based on the distributions of index constituents. (Note that some ETNs take their fees out of the coupons.) Coupons are reported as ordinary income and taxed at ordinary rates. For this reason, ETNs tend to be best-suited for tax-advantaged accounts like 401(k)s and IRAs (read more).

The Alerian MLP ETF (AMLP), which is the largest product in the category, tracks the Alerian MLP Infrastructure Index (AMZI). AMZI is a subset of AMZ. For investors new to MLPs or in need of a refresher, our MLP primer provides a helpful overview of this space and MLP investing.

Bottom Line:

MLPs represent a compelling investment opportunity for investors seeking income, diversification, or more defensive energy exposure.

Related Research:

Accessing MLPs/Midstream Through ETNs

Understanding the Tax Benefits of MLPs

ETFs, CEFs & More: MLP Investment Products Evolve

2Q24 Midstream Dividend Recap: MLPs Drive Growth

AI, Natural Gas, & Midstream’s Emerging Opportunities

MLP Primer: Investing in Energy Infrastructure MLPs

AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMJB, AMUB, MLPR, AMLP and MLPB, for which it receives an index licensing fee. However, AMJB, AMUB, MLPR, AMLP and MLPB are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMJB, AMUB, MLPR, AMLP and MLPB.

For more news, information, and analysis, visit the Energy Infrastructure Channel.