Summary

- Many liquids pipelines adjust their fees each July 1 based on the Federal Energy Regulatory Commission’s (FERC) oil pipeline index, which is based on the Producer Price Index for Finished Goods.

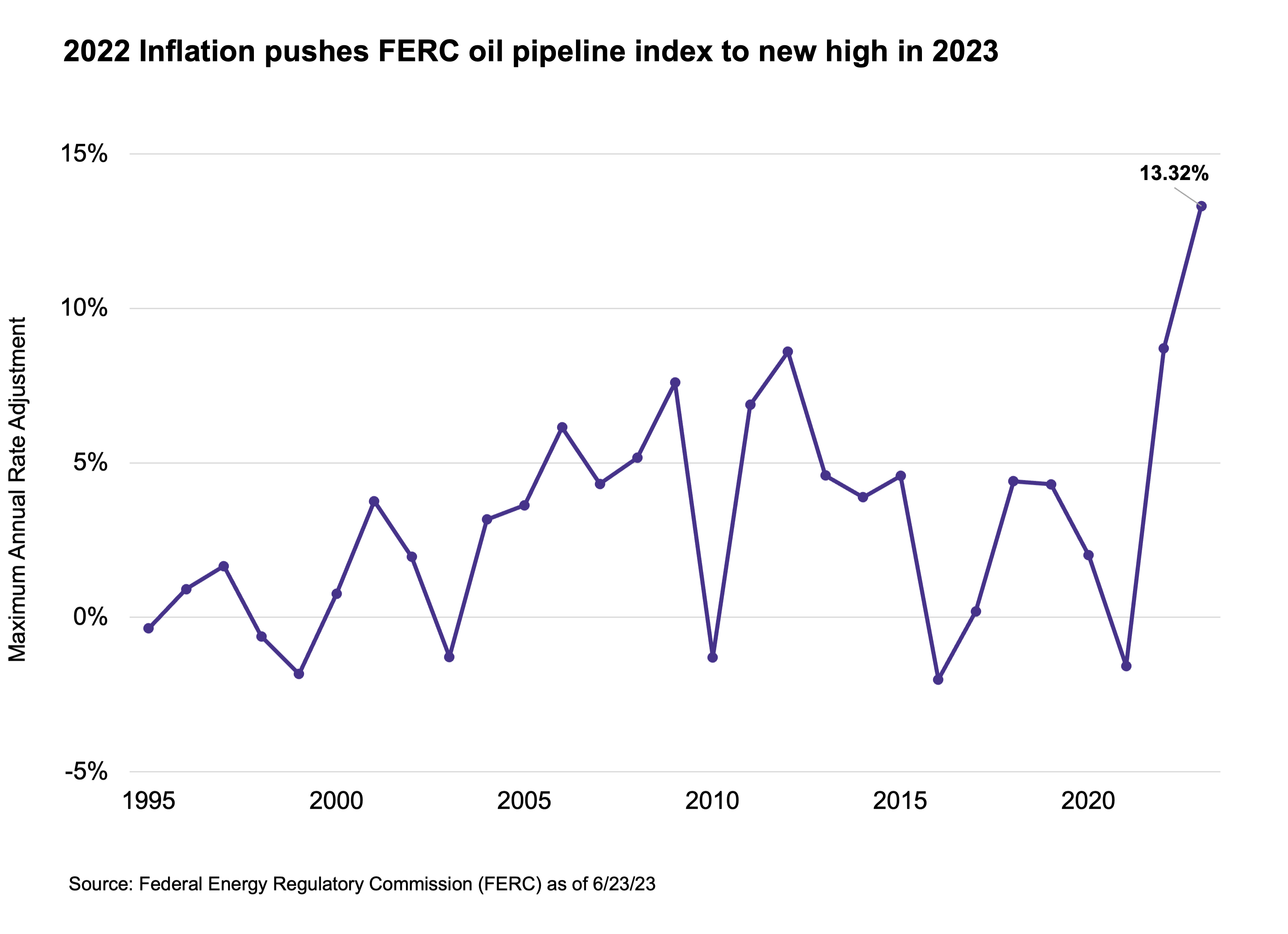

- The elevated inflation seen in 2022 resulted in a fee multiplier of 1.13 (13.32% increase) for this year – the largest increase since the index was introduced in 1995.

- Most pipeline companies likely have some exposure to the FERC index. Companies could generate incremental margin, but windfall profits are unlikely.

The energy infrastructure space largely provides services under long-term contracts that typically include annual adjustments for inflation, resulting in stable, inflation-protected cash flows. For many liquids pipelines, rates adjust on July 1. Given the high inflation seen in 2022, this year’s rate adjustment marks the highest recorded. Today’s note discusses the oil pipeline index, the recent rate adjustment, and its implications for midstream corporations and MLPs.

Oil pipeline index sees highest rate increase ever.

Many interstate liquids pipelines adjust rates annually based on the Federal Energy Regulatory Commission’s (FERC) oil pipeline index. The index establishes the annual maximum rate increase for select pipelines. Despite its name, the index can be used by a variety of pipelines that transport liquids, including natural gas liquids (NGLs) and refined products like gasoline and diesel, in addition to oil. The index is based on the Producer Price Index for Finished Goods (PPI-FG) with an adjustment. The adjustment factor is typically set every five years.

Currently, the index is based on PPI-FG minus 0.21%. The high inflation seen in 2022 resulted in a fee multiplier of 1.13 (13.32% increase) for this year. This represents the highest ceiling increase since the index was introduced in 1995 as shown in the chart below. The higher rate becomes effective July 1 and will remain in place for the next year until rates adjust on July 1, 2024.

Higher fees for liquids pipelines should drive increased revenue for midstream/MLPs in 2H23 and 1H24. While not all liquids pipelines follow the index, most pipeline operators likely have some exposure to the oil pipeline index through crude, NGL, or refined product pipelines. For context, companies primarily focused on petroleum pipelines represented over 45% of the Alerian MLP Infrastructure Index (AMZI) by weighting as of June 26.

What are the implications for midstream?

The headline rate increase for liquids pipelines is very healthy, but it should be viewed in context. Incremental margin is certainly possible, but windfall profits are unlikely. First, not all pipelines increased their rates by 13.3% on July 1. The index does not impact natural gas pipelines, and even for liquids pipelines there are other types of rate mechanisms (read more).

Some companies provide helpful detail around their exposure to indexed rates. For Magellan Midstream Partners (MMP), 30% of their refined product pipeline revenue is subject to the oil pipeline index and 70% is market based or regulated by states. As of early May, MMP expected to increase rates for all its refined product pipelines on July 1 by 11% on average. For NuStar (NS), approximately 95% of contracted product pipeline revenue is tied to PPI-FG.

Another factor to consider is that midstream companies are likely seeing inflationary pressures for various costs (labor, materials, power, etc.). However, cost controls and efficiencies implemented in 2020 may help manage some cost creep (read more). To the extent revenue increases outpace rising costs, bottom lines will benefit, but this will vary by company.

At their January Investor Day, Kinder Morgan’s (KMI) management highlighted the significant portion of revenue from their refined product and terminal businesses with inflation escalators. Specifically, two-thirds of refined product earnings have annual inflation adjustments largely driven by the FERC index. Management noted that they have historically been able to keep rising costs from outpacing the revenue increases, implying incremental margin.

Bottom Line

The inflation protection built into midstream contracts and fee mechanisms is beneficial for the space. Companies can potentially enjoy incremental margin if the higher revenues more than offset rising costs, but the record high ceiling rate increase this year is not likely to result in windfall profits.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

Related Research:

Understanding the Inflation Tailwind for Midstream/MLPs

For more news, information, and analysis, visit the Energy Infrastructure Channel.

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP and MLPB, for which it receives an index licensing fee. However, AMLP and MLPB, are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP and MLPB.