![]() By Michael Jones, RiverFront Investment Group

By Michael Jones, RiverFront Investment Group

Last week the Federal Reserve announced that in October it will begin a long, slow, and cautious process of shrinking its balance sheet. By shrinking its balance sheet the Fed will begin withdrawing some of the Quantitative Easing (QE) stimulus it has provided to the US economy and global financial markets over the past 9 years. We believe that over the next 12 to 18 months the Bank of England, Bank of Japan and European Central Bank will follow the Fed and start winding down their QE stimulus programs.

As the Fed and then other central banks begin shrinking their balance sheets, they will effectively “delete” some of the $10 trillion in new money they have injected into financial markets over the past 9 years. Thus the end of the QE era is likely to have significant consequences for financial markets, in our view. We want to ensure that RiverFront investors understand these potential consequences and the potential impact on portfolio strategy in light of the significant changes in global monetary policy that the Fed initiated with last week’s decisions.

What is QE and How Does it Work?

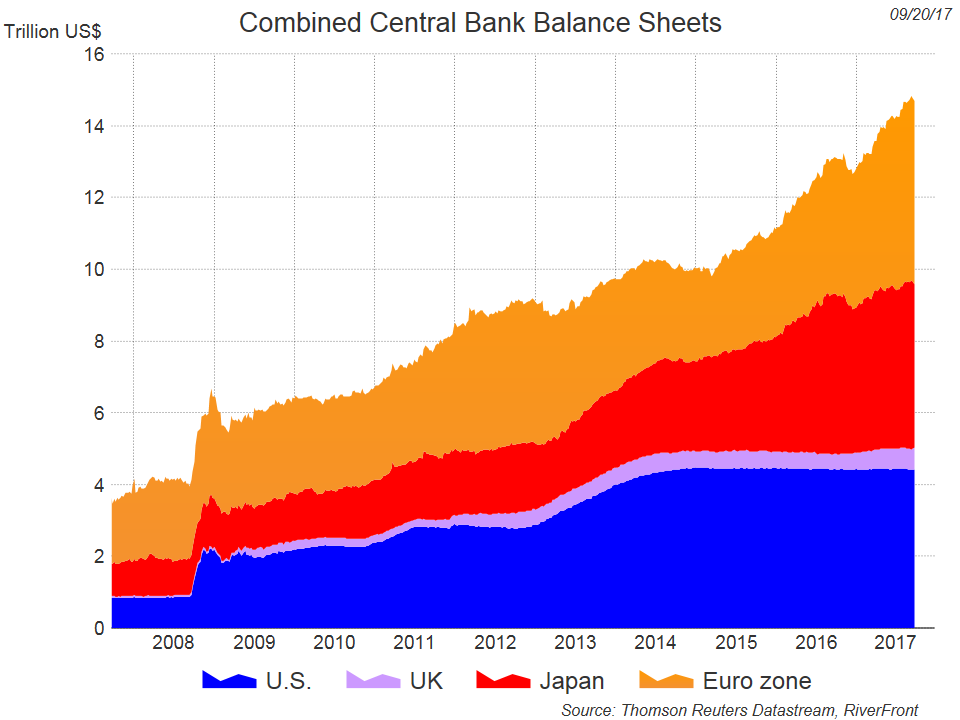

QE is an aggressive monetary policy that the Federal Reserve and other global central banks have used to stimulate their economies in the wake of the 2008 financial crises. Under QE, central banks print money by expanding bank reserves. They use the newly created currency to buy financial assets, primarily government guaranteed bonds. Since bank reserves (the printed money) are a liability for these central banks and the purchased bonds are an asset, one effect of QE is to increase the size of central bank balance sheets. The chart below shows that the major developed economy central banks (US, UK, Japan and Europe) have printed more than $10 trillion dollars since 2008, and have purchased an equal amount of government bonds and other financial assets.

Global Central Banks Have Printed over $10 Trillion Since 2008

By purchasing such a huge amount of government bonds and other financial assets, QE helps keep interest rates low. That makes it easier for governments around the world to finance their budget deficits and for homeowners to refinance into lower mortgage payments. Also, QE injects more money into financial markets (the central banks print it) and takes an equal amount of safe government bonds off the market (the central bank buys them). All that newly printed money has to go somewhere, and therefore QE helps support prices for corporate bonds, equities, real estate and other financial assets.

How Do Central Banks Wind Down QE Stimulus Policies?

We believe the central banks currently engaged in QE are likely to follow the Fed’s three step process for winding down these stimulus programs. First, the central bank slowly “tapers” their monthly purchases of government bonds down to zero (if they buy $80 billion this month, they buy $60 billion next month). Once monthly QE bond purchases have tapered to zero, the central bank keeps its balance sheet roughly unchanged by reinvesting the proceeds of all maturing bonds. In the final stage of unwinding QE, the central bank stops reinvesting all of its bond maturities and its bond portfolio begins to shrink. Unreinvested cash from maturing bonds is deleted from the financial system and the total supply of bank reserves (printed money) declines in lock step with the shrinking bond portfolio.

The Fed was the first central bank to aggressively implement QE, the first to taper its purchases to zero (in October of 2014) and is the first central bank to advance to stage 3 and actually begin deleting money from the financial system. The Fed’s plan calls for reinvesting all but $10 billion in maturing securities at first. That means that $10 billion in bank reserves will be deleted from the system in October. This amount will slowly increase until by the end of 2018 the Fed plans to be shrinking its balance sheet and reducing bank reserves by $50 billion per month.

The Bank of England has also tapered its bond purchases to zero and is likely to soon follow the Fed and begin to reverse its QE stimulus by shrinking its balance sheet. The Bank of Japan is slowing tapering its monthly purchases but it has not set any time table for when it hopes to taper to zero.1 The European Central Bank was the last to adopt QE and has not even begun to taper its monthly bond purchases. Based on comments from ECB President Mario Draghi, we expect them to begin tapering their monthly QE purchases early in 2018. Financial markets will not feel the full impact of the end of QE until every major central bank has completed stage 2 and has tapered its bond purchases to zero. Thus we believe the investment implications discussed below are likely to occur gradually over the next 12 to 18 months.

Investment Implications of the End of QE

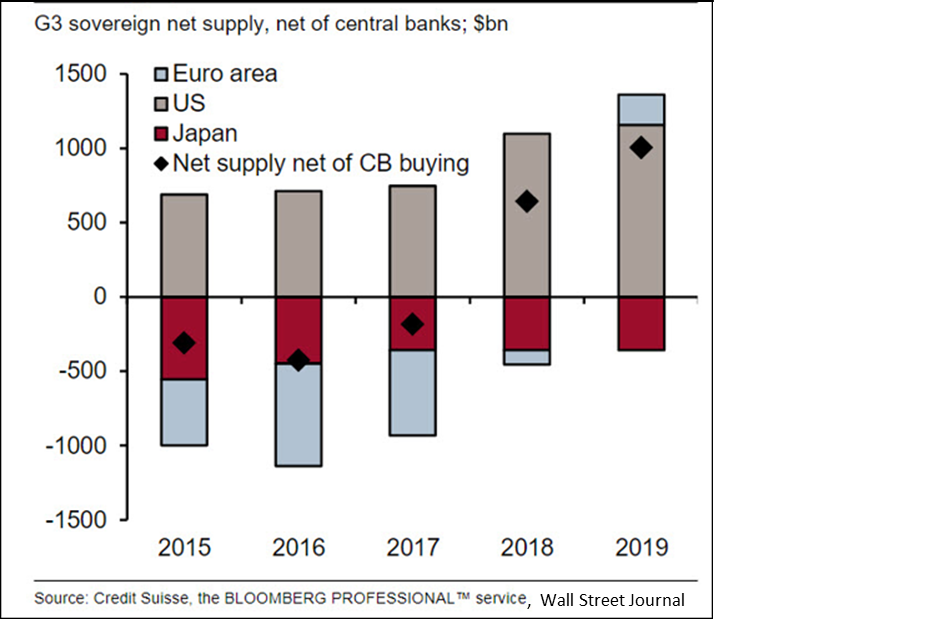

- Long term interest rates are very likely to rise, in our view. We believe the financial market that has been most profoundly impacted by QE is the long term bond market. The $10 trillion of dollars, pounds, yen and euros printed by central banks over the past 9 years were predominately used to buy long term bonds. As shown in the chart below, for the past several years central banks have been buying more bonds than their governments have issued to finance their budget deficits. In other words, developed economy governments, which are normally the biggest sellers of bonds, have for the past several years actually been net buyers of bonds when central bank QE purchases are taken into account. As governments swing back to being net sellers over the next year or two, bond prices are likely to decline and interest rates rise, in our view.

In 2015 and 2016, QE purchases from developed economy central banks exceeded government bond issuance by $500 billion per year (see chart below). US budget deficits are expected to rise over the next 12 to 18 months, the Fed will begin shrinking its balance sheet and more central banks are expected to taper their QE purchases. As a result, the $500 billion of net government bond purchases (central bank QE minus government budget deficits) is expected to shrink to $250 billion by the end of 2017 and swing to net bond sales of $500 billion in 2018 and more than $1 trillion in 2019. Thus the net supply of government bonds will increase by about $1.5 trillion from 2016 to 2019 (-$500 billion in 2016 to +$1 trillion in 2019). We believe private investors can easily finance this additional $1.5 trillion in incremental bond supply, but that 10-year treasury rates in the US will likely need to rise above 3% for them to do so.

Supply of Government Bonds Soars when QE Ends

- For equity investors, we believe that the retreat from QE is occurring at an opportune time. As outlined in our midyear outlook, Faster Growth + Low Inflation = Global Disinflationary Boom, we believe that improving policies and economic conditions across the global economy are fueling an acceleration in global growth. At the same time, structural forces are constraining inflationary pressures. Subdued inflation pressures should allow central banks to be very slow and cautious in withdrawing QE stimulus, avoiding the kind of interest rate increases that have historically prompted recessions and ended equity bull markets. If we are correct that global growth will accelerate and inflation remain low, then we believe earnings growth should be more than sufficient to keep equity markets rising despite modestly higher interest rates.

- Market volatility is likely to increase in our view. We believe that rising earnings, not QE, explains the strong increase in equity prices since 2009. However, QE helped make the market advance much less volatile than would otherwise have been the case, with fewer 10% and 15% market pullbacks than a normal bull market, in our view. For the past 5 years, as more central banks embraced QE, volatility for the S&P 500 has averaged about 11.5%. This compares to a long term average volatility of more than 16%. As the QE era draws to a close, equity investors will likely need to prepare for a return to normal, much higher levels of market volatility. We think that is likely to mean more frequent “normal” 10% and 15% market corrections.

- Implications for our portfolio strategies:

- Underweight bonds and keep portfolio duration low.

- Overweight equities, especially developed international equities where we believe valuations are cheaper and QE will continue for a longer period of time.

- Tactical risk management will become increasingly important as volatility rises. We think investors may lose patience with passive investment strategies if those strategies expose them to more frequent market corrections.

A Note of Caution: We Don’t Know What We Don’t Know

Our relatively positive outlook for equity markets as QE policies are unwound assumes that the cautious, incremental plan approved at the Fed’s September meeting forms a blueprint for every central bank’s QE exit strategy. However, Fed Chairman Janet Yellen’s term expires in January and she may not be reappointed for a second term. President Trump could replace her and fill the three open seats on the Federal Reserve Open Market Committee (FOMC) with more ideological candidates. Similarly, Germany is lobbying hard for a conservative Bundesbank nominee to replace Mario Draghi at the ECB. The Fed’s current plan has overwhelming support and was adopted unanimously, but until we have more clarity about central bank leadership we can’t be certain that central banks will be as cautious as we hope as they unwind their QE policies.

An additional source of uncertainty is the somewhat unprecedented nature of the current policy environment. QE is not new – the Fed helped finance World War 2 and the early years of the Korean War by printing money and buying government bonds. By 1951 the Fed’s balance sheet was almost as big as a percentage of the economy as it is currently (21% versus 26%, according to a 2015 paper by Niall Ferguson2). In the 1940s and 1950s, the Fed targeted interest rates and bought as many government bonds as necessary to achieve its interest rate targets. The Fed backed away from QE by raising its interest rate targets, and as a result the impact on the bond market was known in advance.