Though the tax implications of REITs can seem arcane, their above-average dividends make the asset class worth a look.

The average dividend yield for equity REITs is about 5%, compared to 1.9% for stocks in the S&P 500 Index, according to data from the Motley Fool. Meanwhile, mortgage REITs come in at a whopping 10.6%.

However, since REITs are individual companies, the amount of due diligence required for an investor might seem problematic. This is where REIT ETFs can shine. These funds can hold dozens, even hundreds of individual REITs, allowing investors to maintain diversified exposure in the sector without assuming the risk of an individual company. ETFs also tend to carry low expense ratios.

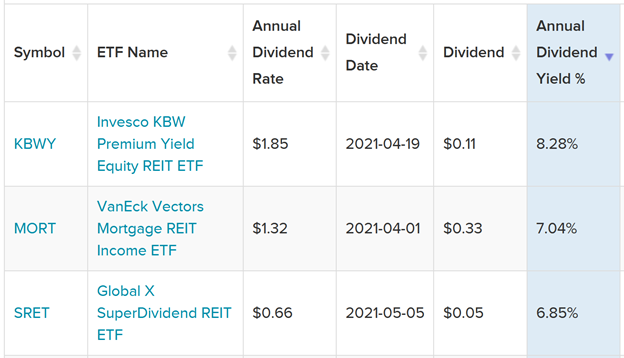

The three REIT ETFs with the highest dividend yields are the Invesco KBW Premium Yield Equity REIT ETF (KBWY) at 8.2%, the VanEck Vectors Mortgage REIT Income ETF (MORT) at 6.99%, and the Global X SuperDividend REIT ETF (SRET) at 6.75%.

Source: ETF Database. Data as of May 17, 2021

REIT Tax Issues Ultimately Not an Issue

To qualify as a REIT, real estate companies are required to pay out 90% of their taxable income to investors—in fact, most REITs pay out more than 100%, as companies can write off depreciation and lower their overall taxable income. That makes them a favorite asset class for investors seeking regular income.

Yet individual REITs tend to have complicated tax structures that can be disadvantageous for an individual investor. Because REIT dividends are often taxed as ordinary income, they’re not eligible for the lower, long-term capital gains rate. However, the majority of those dividends qualify as Qualified Business Income (QBI), which allows taxpayers to deduct 20% of their income above the line.

The 2019 tax reform bill amended the tax code to allow ETF investors to take advantage of this QBI deduction.

Aside from that, REIT ETFs pay dividends according to the same rules as any other dividend-paying ETF: if you hold an ETF for fewer than 60 days before a dividend distribution is made, then the ETF’s dividend is taxed as ordinary income. If you hold the ETF for 60 days or longer, it becomes a “qualified dividend,” taxed at 0%, 15%, or 20%, depending on your tax bracket.

For more news, information, and strategy, visit the Dividend Channel.