The Technology Select Sector SPDR Fund (XLK) rebalanced last week. It swapped a large position in Apple for a large position in Nvidia. While rebalances typically fly under the radar, this one was well-discussed. Why? It resulted in a significant change to holdings involving one of the most high-profile stocks in recent years. Here’s what investors need to know, why it matters, and why it doesn’t.

Background: Index Rules, Rebalances, and More

Sometimes indexing creates a universe that serves as a dataset. But many times, an index is created for the purpose of underlying an ETF. In that case, indexes are constructed to follow a set of diverisfication rules (particularly that abide by the 1940 Act).

The RIC (registered investment company) diversification test which has two criteria: 1) no issuer can be more than 25% of the fund’s assets and 2) positions exceeding 5% cannot be over 50% of the fund’s total assets.

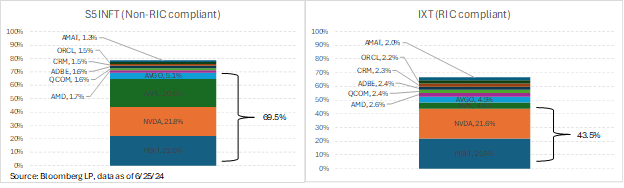

The S&P indexes apply a modified version of these rules with a buffer (i.e., 23% cap for 25% rule and 4.5% cap for 50% rule). To see this rule in effect, we can look at two separate indexes. The S&P 500 Information Technology Sector Index (S5INFT) is a non-RIC compliant index that reflects the broader tech universe, but is not linked to any U.S. ETFs. The Technology Select Sector Index (IXT) is a RIC compliant index which underlies XLK. The S5INFT index weighs constituents by float-adjusted market cap. So, Microsoft Corp (MSFT), Nvidia Corp (NVDA), and Apple Inc (AAPL) all have 20%+ weights in this index. These constituents largely dominate the tech market with around $3 trillion in market cap each. The next largest constituent was Broadcom (AVGO) with only a 5.1% weight. Advanced Micro Devices (AMD) followed with a 1.7% weight.

Rule 1 test: No constituent is above 25% so this rule is not violated.

Rule 2 test: Four constituents have weights over 4.8% and sum up to 69.5%–MSFT, NVDA, AAPL, and AVGO. Therefore the index caps both AAPL and AVGO at 4.5%.

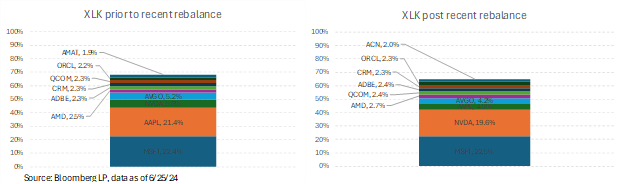

Prior to the June rebalance, NVDA was capped at 4.5% while Apple was 20%+ of the XLK. So after Friday’s rebalance, XLK had to do a sizeable trade of selling around $11 billion of AAPL shares and buying around the $10 billion of NVDA shares. That results in a significantly different weighting of its top holdings.

Too Little Nvidia? Or Too Much?

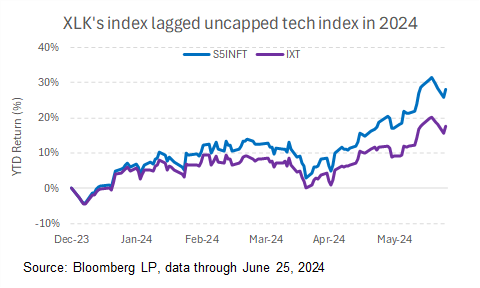

Prior to the recent rebalance, the significant deviation in Nvidia’s weight relative to the market caused some underperformance for XLK. In that case, it seemed like XLK had too little Nvidia and was missing out on gains.

After the recent rebalance, Nvidia shares took a small downturn (but then quickly recovered the next day) causing XLK to fall significantly more than its peers. And regardless of whether you think Nvidia is a good stock or not, it isn’t irrational to assume that artificial intelligence hype has driven valuations to unsustainable levels. In that case, it seemed like XLK had too much Nvidia.

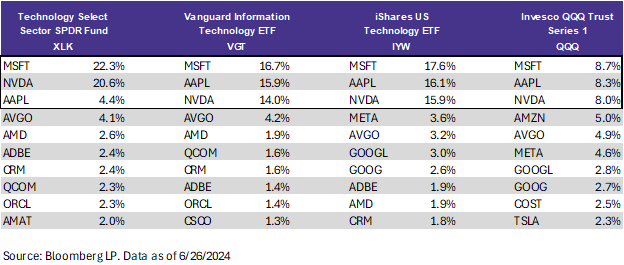

According to S&P Dow Jones Indices’ rebalance FAQs, the index committee “reserves the right to make exceptions when applying the methodology if the need arises” which led many to believe that there could have been an exception made in reweighting these stocks. For example, certain peers have a different weighting methodology where caps aren’t as extreme. The Vanguard Information Technology ETF (VGT), the iShares U.S. Technology ETF (IYW), and the Invesco QQQ Trust Series 1 (QQQ) all apply similar weights to their Microsoft, Nvidia, and Apple holdings. Some of these ETFs still seem overconcentrated in these stocks. However, that is a reflection of the market (and what some consider a disadvantage of market-cap weighted ETFs).

While the weightings look significantly different for XLK, this has not been a disadvantage over the long-term with most of the divergence in recent years.

When Passive Starts to Look Active

I discussed it last week for a completely different group of ETFs, but sometimes building a passive index starts to look more active when you account for various exceptions, exclusion criteria, and weighting methodologies. That’s not always a bad thing—investors can feel like they’re getting a “hands-on” experience at a relatively lower fee. But sometimes it is best to go wherever the market takes us instead of trying to time the market. And in reality, indexes—even passive ones—don’t always reflect the market due to regulations and have to rebalance on a regular schedule even if the timing isn’t necessarily the best. They do, however, make things simpler for investors and take out a lot of “guesswork” out of investment decisions.

FAQ and rules about the rebalance can be found here for the Technology Select Sector Index and here for XLK.

For more news, information, and analysis, visit the Disruptive Technology Channel.