It took a high-profile lawsuit and several years for spot bitcoin ETFs to finally be approved. It was well worth the wait. Over six months later, those ETFs continue to gather interest as more investors understand the complementary nature of crypto and ETFs. On July 23, spot ether ETFs started trading and have carried on the momentum from earlier this year. Here is a look at the first day of trading and what the future could hold for spot ether ETFs.

What happened on July 23

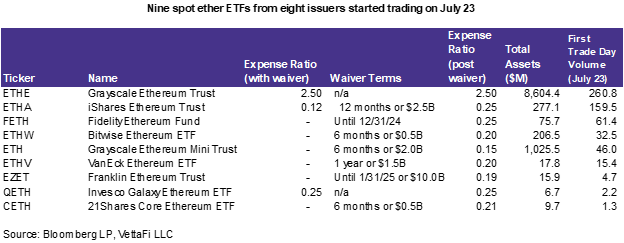

Nine spot ether ETFs from eight different issuers were approved: the iShares Ethereum Trust (ETHA), the Fidelity Ethereum Fund (FETH), the 21Shares Core Ethereum ETF (CETH), the Bitwise Ethereum ETF (ETHW), the VanEck Ethereum ETF (ETHV), the Franklin Ethereum ETF (EZET), the Invesco Galaxy Ethereum ETF (QETH), the conversion of the Grayscale Ethereum Trust (ETHE), and its spinoff the Grayscale Ethereum Mini Trust (ETH).

Like their spot bitcoin counterparts, most of these products have fee waivers for either the first six to 12 months or a certain amount of assets (anywhere from $500 million to $10 billion). The post-waiver fee of spot ether ETFs matches the fee of each issuer’s spot bitcoin ETF. Excluding Grayscale, these fees range from 0.19% to 0.25%. ETHE has a fee of 2.5% while its spinoff, ETH has the lowest fee of the group, at 0.15%. These fees are relatively low. That’s especially so when considering that many spot crypto ETFs in other regions have fees in the 1%-2.5% range. It seems issuers are sacrificing margins to stay competitive and potentially become a trusted name in the crypto ETF world.

Click to enlarge

Big first day for spot ether ETFs with over $1B in trading volume

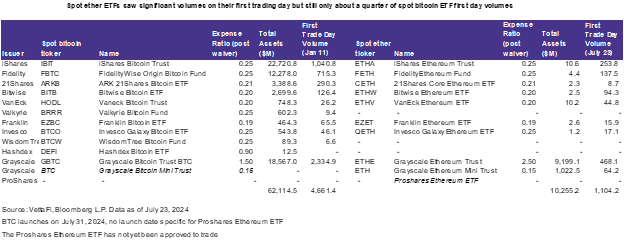

After the first trading day, these nine ETFs had over $1 billion in trading volume. (As of the time this note was written, there is not any flow data available … but there likely will be by the time you read this). But if we assume most of the volume in ETHE (Grayscale’s original Ethereum trust) is outflows and the rest of the ETFs have mostly inflows, there would be between $100M to $200M net inflows.

To compare, spot bitcoin ETFs traded over $4.5 billion in volume on their first day in January. So first day-spot ether ETF volume is between one-fourth to one-fifth of spot bitcoin volume. This isn’t unexpected. Bitcoin is much more popular than ether, with 54% market dominance versus 17% (according to CoinMarketCap). For many investors, bitcoin has become almost synonymous with crypto and can easily be thought of as digital gold. Ether has arguably more use cases than bitcoin for blockchain technology and digital innovation (see previous research note here). But the story can be harder to sell and requires more education.

Click to enlarge

More interest ahead if they follow in the footsteps of spot bitcoin

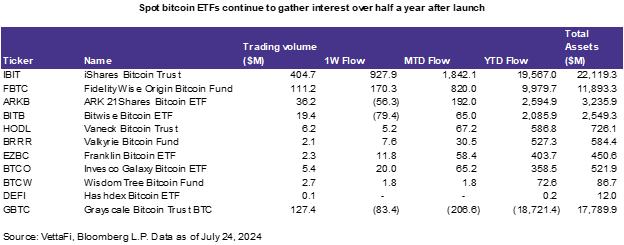

Spot bitcoin ETFs have been the most successful ETF launch ever. Yet demand for spot ether ETFs doesn’t have to be record-breaking for it to be impactful. Just over six months later, these ETFs continue to gather assets. And I expect spot ether ETFs to gather more assets over the long term, especially as more investors begin to understand its use case.

I think there won’t be too many surprises versus spot bitcoin ETFs. The iShares Bitcoin Trust (IBIT) and the Fidelity Wise Origin Bitcoin Fund (FBTC) have dominated their peers. I expect iShares’ ETHA and Fidelity’s FETH will likely remain on top as well. Many of these issuers are native crypto players and have been deeply involved in the industry. But we cannot underestimate what brand names mean to traditional retail investors. That’s particularly so because a large issuer can sometimes make investing in a higher-risk asset like ether seem more acceptable.

While the Ark 21Shares Bitcoin ETF (ARKB) was the third-most in-demand spot bitcoin ETF, I was surprised to see 21Shares CETH at the bottom of the spot ether list. It seems ARK pulling out of the product affected its popularity. Though 21Shares is a huge player in the crypto universe with a good reputation of its own (more on this later).

Lastly, Grayscale has more of chance to dominate this time around. The Grayscale Bitcoin Trust (BTC) has experienced over $18.7B in net outflows YTD mostly due to its high fee (1.5% vs. 0.20%-0.25% for its peers). But Grayscale spun off ETH from ETHE and will spin off the Grayscale Bitcoin Mini Trust (BTC) from GBTC on July 31. Both of these spinoffs will only have a 0.15% fee and will have a higher amount of assets to start. That will make these an attractive option for investors. ETH, for instance, launched with the most assets besides ETHE. When BTC launches, it will have the sixth-highest amount of assets relative to its peers (after GBTC, IBIT, FBTC, ARKB, and BITB).

Click to enlarge

Two types of spot crypto ETF is a lot different than one

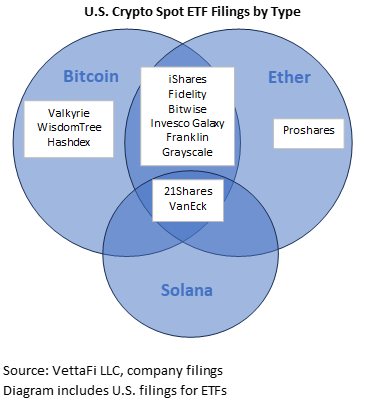

Approval of one type of spot crypto ETF (e.g., bitcoin) can be considered an exception. Two kinds of spot crypto ETFs (e.g., bitcoin and now ether) is not necessarily a rule — but it is close. Some issuers are already eyeing Solana ETFs (see previous coverage here). So it isn’t unreasonable to assume this ecosystem will continue to grow as it does in other countries.

In a recent note, I published a chart that included all issuers involved in the U.S. cryptomarket. I’ve simplified that to just include spot products (including tentative filings). The list becomes more narrow, with only a few overlapping: bitcoin, ether, and Solana. This list is not exclusive, however. And many issuers may be waiting for the spot ether launch to end before focusing on other types of crypto ETFs, like Solana.

I think it’s very likely some of these issuers will attempt to create a suite of crypto ETFs (if allowed by the SEC). 21Shares and VanEck, for example, have crypto suites in other geographical areas like Europe. VanEck offers 12 crypto exchange traded products in Europe. And 21Shares has an even broader offering. Grayscale also offers its line of trusts in the U.S. (GBTC and ETHE were previously part of this line-up) including a Solana trust and Litecoin trust. I would not be surprised if these eventually get converted to ETFs (once again, if it is allowed by the SEC).

There are a few roadblocks with the SEC — like security versus commodity classification. Then there’s also the question of demand and whether ETF investors are focusing on additional digital assets beyond bitcoin and ether. Solana has only 3.5% market dominance compared to 71% for bitcoin and ether combined. These figures tend to align with product demand. For instance, the VanEck bitcoin ETN in Europe has $457 million in net assets, followed by $165 million in net assets for its ethereum ETN, and only $77 million in net assets for its Solana ETN.

Bottom Line

The crypto ETF market has come a long way, and barring any legal roadblocks, may continue to thrive with potentially more products past bitcoin and ether spot ETFs. The spot ether ETF launch has proven that investors do have interest in cryptocurrencies outside of bitcoin. And with more education and resources, we can expect that interest to grow rather than fade away.

For more news, information, and strategy, visit the Crypto Channel.