ETF issuers are still amending S-1s for spot ether ETFs and hoping for a July approval. But some issuers are already looking ahead to the next category of crypto ETFs — spot Solana ETFs. Two issuers (VanEck and 21Shares) have already filed S-1s and more issuers will likely follow.

While Solana is significantly smaller than bitcoin and ether, this could be another potential milestone for crypto ETFs. If these are approved, it would mean a spot crypto ETF would be able to stand on its own. For months, spot crypto ETFs were clinging to the precedent set by the Grayscale case that if futures are approved, then spot should be approved. But this would be the first time a spot crypto ETF is approved without a futures ETF counterpart. As important as this would be, it is not a guarantee a Solana spot ETF would be approved (more on this later).

First of All, What Is Solana?

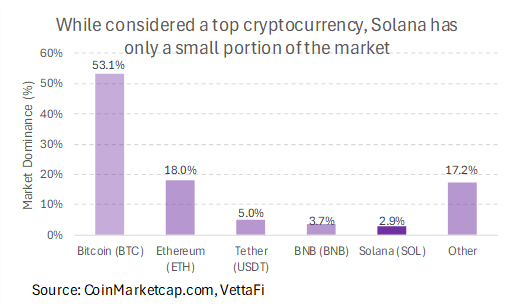

Solana (SOL) is the fifth largest cryptocurrency by market cap. However, market dominance is extremely small (close to 3%) compared to 53% for bitcoin and 18% for ether.

Solana is a smart contract platform like the ethereum network. It was designed to be a new and improved competitor. Both can support digital applications, NFTs, etc., but Solana is:

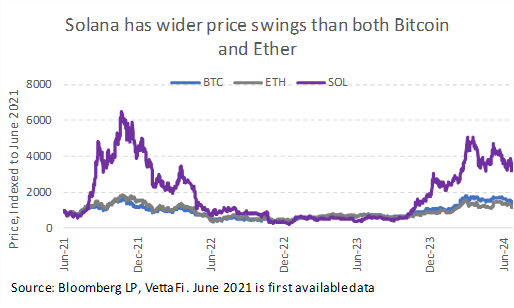

- Newer: Solana was created in 2017 vs. ether in 201,5 so there is less pricing history. A shorter history can be riskier since there is less data for comparison. On the other hand, there can be more room for growth for an early-stage investment. YTD, Solana is up around 39% — only slightly higher than bitcoin (up 37%) and ether (up 34%). But in 2023, Solana was up close to 800% (compared to 156% for bitcoin and 91% for ether).

- More efficient: Like ether, Solana uses a proof-of-stake consensus mechanism. Solana also uses a proof-of-history time-stamping mechanism. Unlike proof-of stake and proof-of work, proof-of-history is not a consensus mechanism. Its purpose is to improve efficiency and is part of the reason Solana is so much faster than ethereum. (Ethereum can process approximately 13 transactions per second vs. Solana, which can process approximately 3,000 per second.) In addition to faster processing speeds, Solana also has lower costs, which makes it attractive for users.

Solana ETFs: 2 SOL Filings

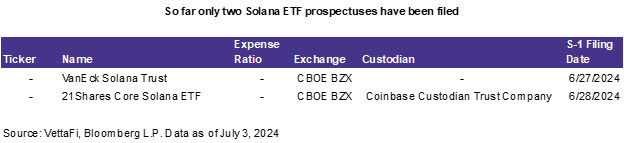

Currently only two issuers have filed for a spot Solana ETF — VanEck on June 27 and 21Shares on June 28. Filings are in their early stages (no tickers or fees yet), and there is very little information available. It seems that both VanEck and 21Shares wanted to capture early mover status. But I believe more issuers will submit spot Solana ETF filings after the spot ether ETFs are finalized. Both VanEck and 21Shares already have Solana products in other countries, which is why their early moves make sense. 21Shares has the 21Shares Solana Staking ETP available in Europe (total assets of $801 million). VanEck has the VanEck Solana ETN, also available in Europe (total assets of $65 million).

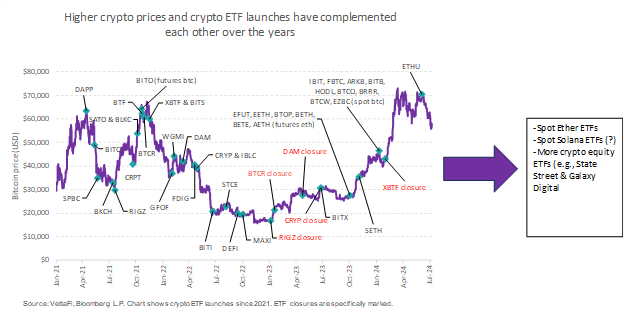

While the spot bitcoin ETF launch was one of the most impactful ETF launches to date — even after six months, the iShares Bitcoin Trust (IBIT) and the Fidelity Wise Origin Bitcoin Fund (FBTC) continue to hold significant interest — I expect the upcoming spot ether launch to have less impact given its smaller market dominance, and the (potential) spot Solana launch to have very minimal demand. Still, there will likely be interest from issuers that want to create a broader crypto ETF offering in the U.S. For example, VanEck currently offers ETNs in Europe for several cryptocurrencies including: bitcoin, ethereum, Solana, Polkadot, TRON, Avalanche, Polygon, Algorand, and Chainlink. 21Shares offers its ETPs in many of the same coins mentioned above in addition to BNB, Ripple, Uniswap, and many others (see here for full list).

What Are the Risks?

I looked through the S-1 documents for both the proposed VanEck product (here) and the proposed 21Shares product (here). I then compared them with the filings for their spot ether counterparts. Neither document outlines many risks unique to Solana that aren’t found with ether. Unique risk factors include a shorter price history and the proof-of-history mechanism, which is a lesser-known mechanism. There is also the risk that a Solana ETF could be less attractive than direct investment in Solana. That is due to the lack of staking (the SEC did not allow staking for spot ether ETFs either, despite staking being allowed in other countries). The biggest issue, in my opinion, is the regulatory risk behind Solana. All crypto has a high level of regulatory risk. But that risk is higher in cryptocurrencies outside of bitcoin and ether, like Solana.

Solana’s Security Status Is the Biggest Hurdle

One of the biggest risks faced by Solana has been whether digital assets should be treated as securities. In June 2023, the SEC brought charges against Binance and Coinbase. The agency alleged that they were trading unregistered securities — including Solana. There are several legal tests that can tell whether an asset is a security. These include the Howey test and the Reves test. The Howey test has been more widely discussed. It asserts that an investment contract requires: 1) an investment of money; 2) a common enterprise; 3) the expectation of profit; and 4) it be derived from the labor of others.

While bitcoin’s status as a security was initially debated, it seemed that the SEC settled on bitcoin as a commodity. Because of its anonymous nature (we don’t even know the real identity of Satoshi Nakamoto), profits are not dependent on the labor of others. While there was some back and forth with ether, it was eventually classified as a commodity. But there has been little direct commentary on something like Solana besides what we know from the earlier lawsuits. Because Solana is so similar to ether, it would make sense that they would eventually have the same classification, but that has not yet been clarified .

If this all sounds confusing, it’s because it is. These rules are not easily translated to something like cryptocurrencies, and it seems like cryptocurrencies will keep head-butting with the SEC like this until someone creates a crypto framework.

Bottom Line:

It is still a big if whether Solana ETFs will be approved at this point, but if they are, that could open up a greater crypto ETF ecosystem in the U.S. that would require an updated regulatory framework. That makes these filings (and a potential launch) significant regardless of the market demand these ETFs would receive.

For more news, information, and strategy, visit the Crypto Channel.