As I write this, the market is officially in correction territory, with the S&P 500 off 14.5 percent from its all-time close on February 19. It took only six days, in fact, for the S&P to fall 10 percent from its high into a correction—a new record, according to data from Deutsche Bank Global Research.

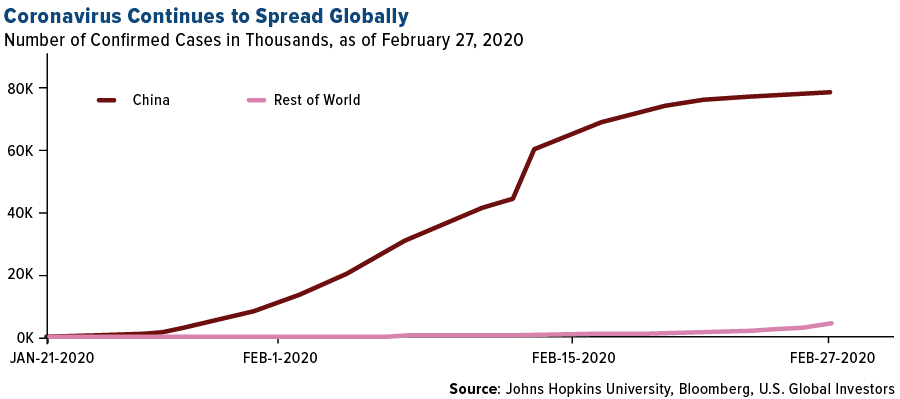

The decline has certainly hurt many equity investors and 401(k)s, and there may still be more pain ahead. Today the World Health Organization (WHO) raised its threat assessment of the coronavirus, or COVID-19, to “very high,” and warned that the illness could soon reach most, “if not all,” countries across the globe in the coming days and weeks.

I choose to remain optimistic, though. The underlying economy is sound. Nothing has changed about that. This selloff is purely incidental to the outbreak, and once it’s contained and the number of new infections begins to plateau, I expect to see stock markets recover sharply. The same goes for the industries that have been hardest hit by the virus, including travel and tourism, airlines and energy.

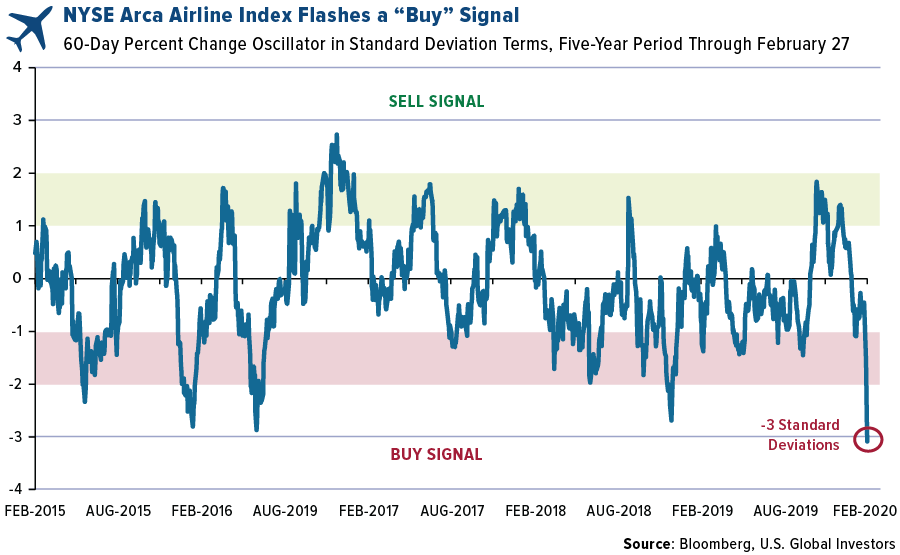

Take a look at the oscillator chart below. It shows that airline stocks are trading down a rare three standard deviations, the most in at least five years. What this means is that airlines are extremely oversold and flashing a “buy” signal. As soon as this outbreak subsides, I believe airlines will begin to soar again.

During his press conference on Wednesday, President Donald Trump appointed Vice President Mike Pence to manage the U.S. response to the outbreak as well as the government’s messaging about the virus. The media is far too negative, Trump said, and there’s a lot of misinformation out there.

|

|

I don’t think I can disagree with him there. A recent survey found that, amazingly, 38 percent of Americans wouldn’t buy Corona “under any circumstances” because of a perceived link between the Mexican beer and the coronavirus. (For the record, there is none.)

This link came up in a humorous way this week at the BMO Global Metals and Mining Conference in Miami, Florida, where Ivanhoe Mines founder and chairman Robert Friedland delivered a spectacular luncheon speech. I had dinner with him later that evening, and he arrived not only wearing gloves but also drinking a Corona. When someone asked Robert, who does not drink, why he had the Corona, he answered that it would prevent the coronavirus.

He meant this as a joke, of course, but there may be some logic to the levity, as one important way to avoid infection is to keep your throat moist.

Another innovative method? Copper-infused facemasks. According to reports, an Israeli textile scientist has found a way to infuse the cotton fibers in facemasks with copper, blocking entry to germs, bacteria and other microscopic pests. In 2014, during the Ebola outbreak, the red metal was also found to be effective at fighting the virus.

Commodity Selloff Presents Attractive Buying Opportunities

Like airlines, commodities look oversold right now based on the 14-day relative strength index (RSI), meaning there could be some potentially attractive buying opportunities. Brent crude oil, the global benchmark, traded below $50 per barrel on Friday for the first time since July 2017, while copper remained mostly range-bound.

Remember, commodities are the building blocks of the world we live in, and we will only need more of them in the years ahead. After all, people are not going to stop having babies, and they’re going to grow up and want the things their parents had and then some—all of which require raw materials.

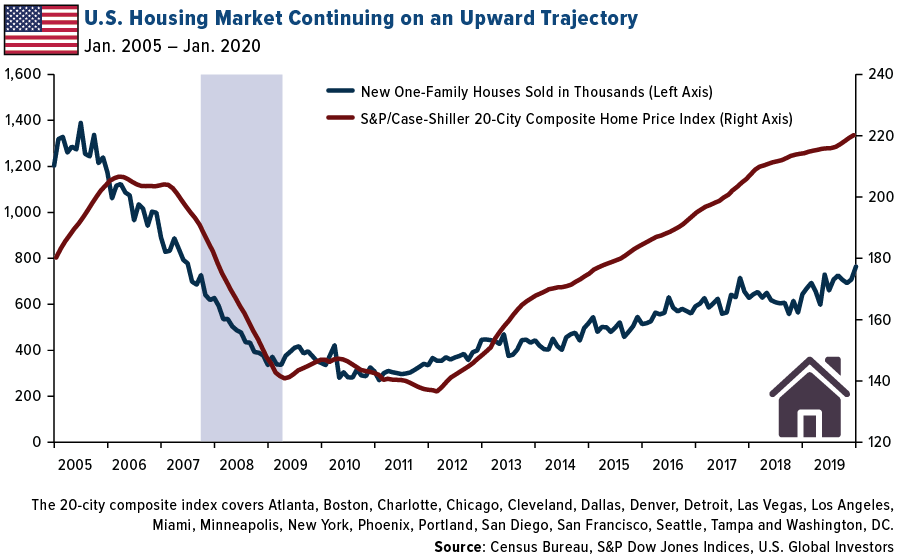

Take housing, for instance. New home sales in the U.S. surged to a 12.5-year high in January, while home prices climbed to a new all-time high. Consider what’s needed to build a typical American home, from the lumber, plumbing and electrical wiring to concrete, insulation and appliances. Consider also that American homes have generally been getting larger over time, requiring even more raw materials.

Gold ETF Holdings Climb to a Record

The price of gold had one of its worst one-day declines in recent years on Friday, dropping below $1,600 per ounce, or about 5 percent at one point.

I actually see this pullback as positive. In the past few days, gold has been the only major asset making steady gains, and now investors are taking profits to cover margin calls. I wouldn’t be surprised if we see a rebound next week as investors take advantage of the discount to add to their exposure.

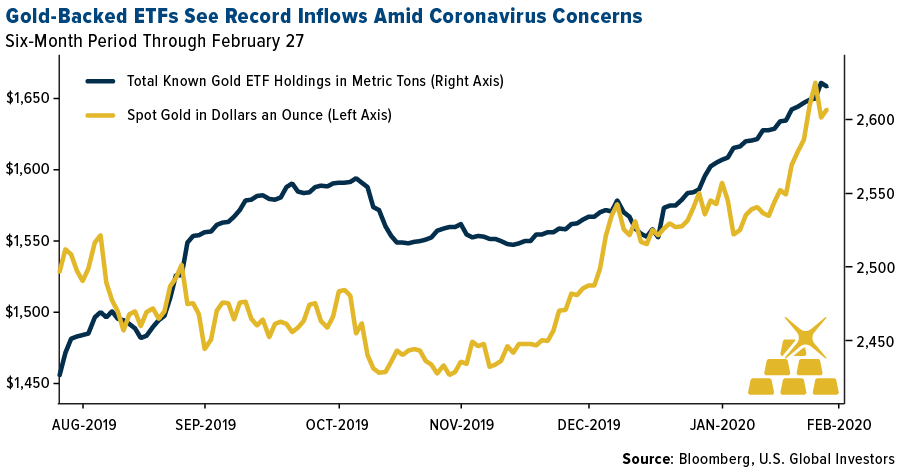

Gold’s longstanding role as a safe haven was on full display this week, as gold-backed ETFs saw their 25th consecutive day of inflows on February 27, a record. At 2,624.7 metric tons (about 93 million ounces) the holdings were the largest ever recorded.

Why Can’t Gold Hit $10,000?

Like I said before, I attended BMO’s metals and mining conference this week, and I had the chance to speak with Kitco’s Paul Harris about where gold could be headed from here. As I told him, we’ve seen palladium jump to more than $2,700 an ounce, rhodium as high as $13,000, up an incredible 114 percent this year alone, on increased demand from the automotive industry. During his presentation, Robert reminded us all that no one a year ago would have ever believed we’d see palladium and rhodium get to where they are today.

There’s no reason why the same can’t happen to gold, I told Paul. With Treasury yields at record-low levels and Federal Reserve Chairman Jerome Powell hinting at an emergency rate cut, what’s stopping gold from soaring to $10,000?

What may also help get us there is the idea of peak gold, which I discussed in this week’s Frank Talk. Barrick CEO Mark Bristow shared the following chart at BMO showing that global gold production is expected to taper off starting next year, and by the end of the decade, should be at multi-year lows.

Demand for the yellow metal will continue to grow as more people in developing countries join the middle class. Supply growth, on the other hand, looks constrained, which may have the effect of pushing prices up.

To see my full interview with Kitco at the BMO Conference, click here!

Gold Market

This week spot gold closed at $1,585.69, down $57.72 per ounce, or 3.51 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 13.31 percent. The S&P/TSX Venture Index came in off 14.60 percent. The U.S. Trade-Weighted Dollar fell 1.17 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-25 | Hong Kong Exports YoY | -3.7% | -22.7% | 3.3% |

| Feb-25 | Conf. Board Consumer Confidence | 132.2 | 130.7 | 130.4 |

| Feb-26 | New Homes Sales | 718k | 764k | 708k |

| Feb-27 | GDP Annualized QoQ | 2.1% | 2.1% | 2.1% |

| Feb-27 | Durable Goods Orders | -1.4% | -0.2% | 2.9% |

| Feb-27 | Initial Jobless Claims | 212k | 219k | 211k |

| Feb-28 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Mar-1 | Caixin China PMI Mfg | 46.0 | — | 21.1 |

| Mar-2 | ISM Manufacturing | 50.5 | — | 50.9 |

| Mar-3 | Eurozone CPI Core YoY | 1.2% | — | 1.1% |

| Mar-4 | ADP Employment Change | 170k | — | 291k |

| Mar-5 | Initial Jobless Claims | 215k | — | 219k |

| Mar-5 | Durable Goods Orders | — | — | -0.2% |

| Mar-6 | Change in Nonfarm Payrolls | 175k | — | 225k |

Strengths

- The best performing metal this week was gold, down 3.51 percent. As of Wednesday, gold-backed ETFs saw 25 consecutive days of inflows and rose to the highest level ever of 2,624.7 tons. Bloomberg reports that after rising 18 percent last year, gold extended its rally into 2020. Turkey’s gold reserves rose $1.1 billion from the previous week to now total $29.7 billion as of February 21, according to weekly figures from the central bank in Ankara.

- Russia’s second largest gold producer, Polymetal International, says it plans to boost its share of female employees as the government opens more mining jobs to women, reports Bloomberg. Polymetal says it wants women to make up at least 30 percent of its workforce. For decades Russia has banned women from working in jobs that are deemed physically challenging, which are most jobs in mining, but it is now reversing that policy.

- New Gold Inc. formed a partnership with Ontario Teachers’ Pension Plan that gives the miner $300 million in exchange for selling a portion of the free cash flow from its flagship mine, Bloomberg reports. New Gold will sell a 46 percent free cash flow interest from its New Afton Mine. This is a common practice of selling a stream or royalty to help finance developments.

Weaknesses

- The worst performing metal this week was platinum, down 11.19 percent. After surging early in the week, gold joined the bloodshed of the stock market and saw its biggest selloff since 2013. Investors are selling the metal to cover margin calls and some is profit taking. Bloomberg writes that during the later phases of a selloff, gold generally recovers and outperforms, but in the early stages it gets thrown out.

- The coronavirus fears helped gold rally, but investors largely overlooked silver as a safe haven. With most precious metals rising, silver is the cheapest, as the ratio of gold to silver rose to 92. Hopefully investors start to realize this and show some love for the white metal.

- OceanaGold entered into a forward gold sale arrangement to deliver 48,000 gold ounces between September and December 2020, with a pre-payment of $78.5 million, according to a company statement. Although OceanaGold could benefit if gold prices fall, because it locked in the current price, it is not ideal that the company had to make this arrangement in the first place. If gold rises above the price it locked in, OceanaGold will have lost money.

Opportunities

- Gold could continue its upward trajectory because many investors aren’t even exposed to the metal. Peter Grosskpf, CEO of Sprott Inc., said that fewer than 10 percent of investors own gold and the metal probably makes up less than 2 percent of portfolios on average that do hold it. Grosskopf added that “investor participation in gold is still anemic” and argues that a portfolio should have 5 percent exposure to the yellow metal as a form of insurance. Goldman Sachs boosted its forecast for gold to $1,800 in the next 12 months on Thursday as the coronavirus, depressed real rates and focus on the U.S. election continue to drive haven demand, reports Bloomberg.

- Impala Platinum Holdings is bullish on both palladium and rhodium as the precious metal price rally led to its first dividend in more than six years. CEO Nico Muller said “we are confident about the market, we are confident about the future.” Palladium extended its rally and rose 2.5 percent on Wednesday to $2,849.94 per ounce. Norilsk Nickel asked the Russian government to pay for half the cost of renovating its housing stock, reports Bloomberg. The company said the project is the start of a new investment program worth over 2.5 trillion rubles.

- Sibanye CEO Neal Froneman said in an interview at the BMO Global Metal & Mining Conference in Miami this week that the company hopes to buy a gold miner for $4 billion to $5 billion in the next six to nine months. Sibanye already has several takeover targets and met with various companies at the conference. TriStar Gold Inc. announced several positive drill results from its Castelo de Sonhos gold project. Highlights include 3 meters at 9.3 grams per ton from 39 to 42 meters.

Threats

- Gold hit a wall this week despite a brutal selloff in global equities. The yellow metal is typically seen as a safe haven during periods like this. Bloomberg’s Ranjeetha Pakiam and Alix Steel write that there is always a risk during periods of turmoil that investors sell gold, which happened during the 2008 financial crisis. Suki Cooper, precious metals analyst, remained positive on bullion and said in a Bloomberg TV interview that “we think that there will be opportunities to continue to add to long exposure.”

- Credit default swaps surged this week as insurance costs jumped by the most on record. Fears about the coronavirus essentially shut out almost all borrowers looking for fresh cash in the U.S. and Europe. Fed Chairman Jerome Powell said that the virus outbreak poses evolving risks for U.S. growth and signaled that the central bank is prepared to cut interest rates to support expansion if necessary, reports Bloomberg.

- Goldman Sachs Group Inc. economists said on Friday that they now expect the global health concerns to inflict a “short-lived global contraction” on the world economy. They also think it will force the Fed to cut interest rates in the first half of this year as a result.

Index Summary

- The major market indices finished heavily in the red this week. The Dow Jones Industrial Average lost 12.36 percent. The S&P 500 Stock Index fell 11.49 percent, while the Nasdaq Composite fell 10.54 percent. The Russell 2000 small capitalization index lost 12.04 percent this week.

- The Hang Seng Composite lost 4.36 percent this week; while Taiwan was down 3.37 percent and the KOSPI fell 8.13 percent.

- The 10-year Treasury bond yield fell 31 basis points to 1.166 percent.

Domestic Equity Market

Strengths

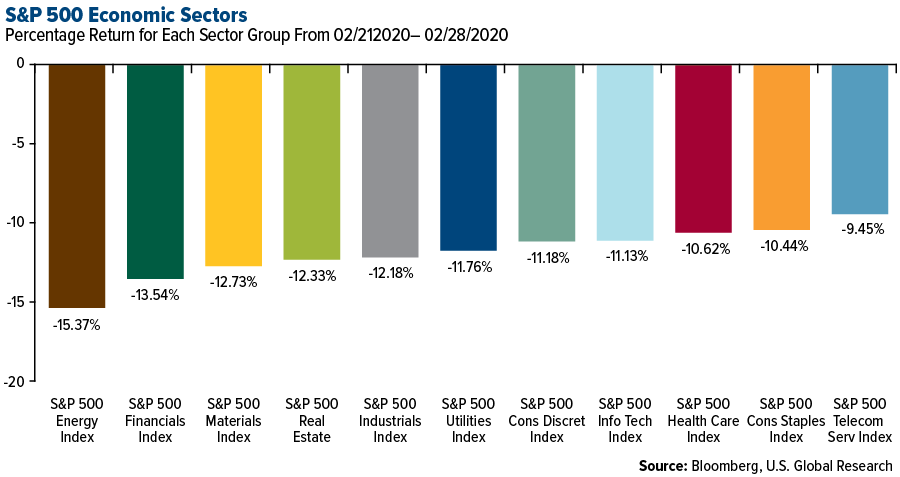

- Communication services was the best performing sector of the week, decreasing by 9.45 percent versus an overall decrease of 11.57 percent for the S&P 500.

- Regeneron Pharmaceuticals was the best performing S&P 500 stock for the week, increasing 10.24 percent.

- Regeneron Pharmaceuticals was the only stock in the S&P 500 to record a meaningful weekly gain. In early February the company said it was working with the U.S. Department of Health and Human Services on a treatment for the current strain of coronavirus. Novartis, Regeneron competitor, launched a review of Beovu, a treatment for wet age-related macular degeneration, after a physicians’ group raised concerns about its side effects. Regeneron has a competing product, Eylea. Regeneron shares jumped on the Novartis stumble, but are also up 26 percent over the past month.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 15.37 percent versus an overall decrease of 11.57 percent for the S&P 500.

- American Airlines was the worst performing S&P 500 stock for the week, falling 31.52 percent.

- Tupperware Brands hit a record low this week after warning that profit would drop sharply amid an accounting probe at its Mexican beauty business. The Orlando-based consumer products maker said full-year earnings per share for 2019 would be between breakeven and 34 cents, down from $3.11 the year before.

Opportunities

- The damage from the coronavirus is temporary and global growth will bounce back later this year, strategists at Morgan Stanley and Credit Suisse Group AG said, providing a potential source of optimism for battered equity markets. “It’s probably too early to call a market bottom, but at the same time we believe that the virus will be a temporary event so even after we have reduced our global growth forecasts, we still believe that there’s going to be a recovery in 2020,” Philipp Lisibach, head of global equity strategy at Credit Suisse’s international wealth management unit, said in a phone interview. Morgan Stanley economists called the virus a “transitory, exogenous shock” as opposed to a slowdown caused by an overheated economy facing fundamental problems. They expect a “strong” rebound in growth beginning either in the second or third quarters, on the back of international monetary and fiscal support.

- Income-seeking investors may now be better off with U.S. stocks than with Treasury securities of any maturity. The dividend yield on the S&P 500 Index exceeded the 30-year bond yield Thursday by 24 basis points, the most since March 2009, according to data compiled by Bloomberg.

- Etsy shares rose more than 14 percent during Thursday’s session after the company reported better-than-expected fourth quarter financial results. Revenue rose 35 percent to $270 million, beating consensus estimates by $5.08 million, and earnings per share came in at 25 cents, beating consensus estimates by nine cents. Several analysts increased their price target on the stock, while Oppenheimer upgraded the stock to outperform with a $64 price target.

Threats

- Adidas sales plunged 85 percent in China as coronavirus ravages demand. “We have been experiencing a material negative impact from the coronavirus outbreak on our operations in China,” the German sportswear giant said.

- Daimler warns of “significant adverse effects” of the virus outbreak. The German auto giant said the epidemic could hurt sales and hamper its production, procurement and supply chain.

- Japanese gaming giant Nintendo could face supply shortages as a result of the coronavirus. Bloomberg reports that the company may struggle to supply Switch consoles to the U.S. and Europe as soon as April.

The Economy and Bond Market

Strengths

- U.S. consumer sentiment remained elevated in the second half of February despite the intensifying coronavirus fears that have battered equity markets. The University of Michigan’s final sentiment index for February was little changed at 101 from an initial reading of 100.9.

- The Commerce Department said on Friday that consumer incomes for January rose 0.6 percent, the biggest gain in nearly a year, spurred by bigger paychecks and an increase in Social Security benefits stemming from a cost of living adjustment.

- The economy grew moderately in the fourth quarter, the government confirmed on Thursday. Gross domestic product increased at a 2.1 percent annualized rate, supported by a smaller import bill. That figure was unrevised from last month’s advance estimate and matched the growth pace logged in the July-September quarter.

Weaknesses

- Goldman Sachs Group Inc. economists said they now expect the coronavirus to inflict a “short-lived global contraction” on the world economy that will force the Fed to slash interest rates in the first half of this year, reports Bloomberg. In a report released on Friday, Goldman economists led by Jan Hatzius said the outbreak of the deadly virus meant they now predict global GDP to contract on a quarterly basis in the first two quarters of this year before rebounding in the second half. “All else equal, this would imply a short-lived global contraction that stops short of an outright recession,” the economists wrote.

- The number of Americans filing for unemployment benefits increased by more than expected last week. Initial claims for state unemployment benefits rose 8,000 to a seasonally adjusted 219,000 for the week ended February 22. Data for the prior week was revised to show 1,000 more applications received than previously reported. Economists polled by Reuters had forecast claims increasing to 212,000 in the latest week.

- Orders to U.S. factories for big-ticket manufactured goods fell in January, dragged down by decreased demand for cars, auto parts and military aircraft. The Commerce Department said on Thursday that orders for durable goods slipped 0.2 percent last month after rising 2.9 percent in December.

Opportunities

- Next week, average hourly earnings are forecast to have risen by 3.2 percent year-on-year, while the jobless rate is predicted to hold at 3.6 percent.

- After a solid gain of 225,000 jobs in January, the economy is projected to have added 178,000 jobs in February. This would represent a notable slowdown, but nothing worrying just yet.

- The ISM non-manufacturing gauge that includes the vast services sector is forecast to stay unchanged at 55.5 when released on Wednesday.

Threats

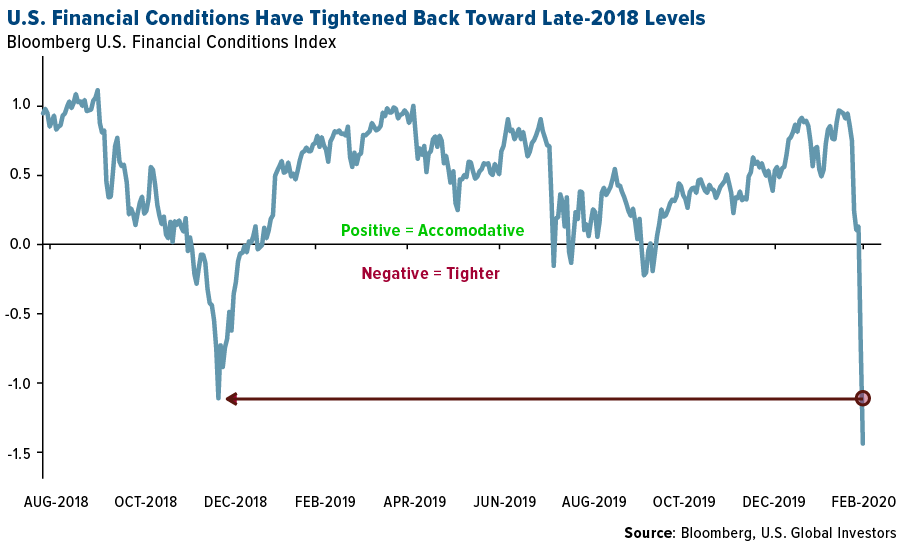

- Strains across U.S. markets are intensifying along with the rapid escalation of coronavirus cases. On a closing basis, the Bloomberg U.S. Financial Conditions Index is back to levels last seen in December 2018, when a slump in stocks and credit markets set the Fed on course for three interest rate cuts last year. Rate futures are now pricing in at least a quarter-point of easing at the March meeting, and Jefferies analysts say a preemptive move could even be imminent.

- Investors will be dissecting key data next week for any signs that growth in the economy may have already started to falter from the impact of the virus epidemic. First on the radar is the ISM manufacturing PMI on Monday. The index is expected to decline slightly to 50.5 in February to hold just above expansionary territory.

- One indicator policymakers as well as traders will be watching to understand the scale of the damage of the virus on China’s economy is the official manufacturing PMI due on Saturday. Forecasts are for the PMI to drop from 50.0 to 46.0 in February. If markets wake up to a worse-than-expected figure on Monday, the risk-off mood is likely to deepen. Later on Monday, the Caixin manufacturing PMI will be published and it will be interesting to see whether the private survey is in line with the government one.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was coffee, which gained 1.0 percent as supplies are expected to be tight from Brazil this year. French oil major Total SA is a final bidder for a stake in an offshore wind farm that would cost more than $7 billion to develop and operate, reports Bloomberg. British utility SSE Plc is developing the 1,075-megawatt farm in Scotland’s section of the North Sea and is seeking partners for the facility that is the first not to have full state support. The move by Total to potentially invest in the project demonstrates growing interest from major oil companies in renewable assets.

- Eni SpA estimates that its oil and gas production will peak in six years and is targeting an 80 percent cut in net emissions by 2050. CEO Claudio Descalzi said that “the market is changing, our customers are changing” and “we are building a new Eni.” The company hopes for gas to make up 85 percent of total output by 2050.

- Engineering consultant Aurecon Group said on Friday that the Neoen SA-owned Hornsdale Power Reserve in Australia has responded to three major system outages and has helped restore stability to the network and lower the costs of running the grid. The Hornsdale battery is the world’s largest lithium-ion battery and was installed by Tesla in 2017 to help solve a power crisis in South Australia, reports Bloomberg. Aurecon Managing Director Paul Gleeson said in a media release that the battery “demonstrates at scale the potential for battery storage to provide fast-acting supply and demand balancing.”

Weaknesses

- The worst performing major commodity for the week was crude oil, which fell 15.57 percent over fears the corona virus will stifle travel plans. Palm oil had its biggest weekly drop in 11 years – since the financial crisis – as some of the biggest producers warned of demand destruction. Bloomberg reports that the commodity fell more than 11 percent this week. Sime Darby Plantation Bhd said that demand from China has virtually “dried up.” Palm oil is the world’s most consumed edible oil. Crude oil took a giant hit this week, falling past 13-month lows near $40 a barrel, as the world grapples with weaker demand. Zinc fell below $2,000 a ton for the first time in three years as the virus threatens to derail sales of almost every product it’s used in.

- Stockpiles in copper and steel continue to build as demand for the widely used metal continues to drop. Worldwide holdings of copper rose to the highest level since September 2018 as the coronavirus slows growth and hurts corporate supply chains. Benchmark prices for the red metal have sunk more than 8 percent in London so far this year, reports Bloomberg. Nickel and tin led base metals lower this week as global health concerns grow. Citigroup said in a note that “there does not seem to be a strong rationale why the coronavirus will not spread globally over the coming weeks, resulting in governments shutting down a substantial share of the world’s economic activity for up to 1-2 months.”

- Apache Corp. posted a massive $3 billion write down on its Alpine High project, a shale discovery in West Texas from 2016 that bombed when it was found out that it held more natural gas than oil. This comes at a time when natural gas prices are falling and it is not economical to extract the fuel. The company will instead focus on offshore deposits in Suriname, where it recently found crude oil and partnered with Total SA.

Opportunities

- BNP Paribas Asset Management is looking for commodity prices to push lower by 5 percent to 10 percent to consider them a buy. Colin Harte, portfolio manager at BNP, said in a Bloomberg interview that if industrial metals such as copper, iron ore and nickel fall from current prices then the asset manager “will certainly build up very aggressive long positions in them.” Bloomberg reports that they have been neutral and cautious on industrial metals and oil, with gold as a long-term hedge against potential risks.

- South Africa’s troubled Eskom Holdings is working on a 3,000-megawatt gas-fired plant that could help alleviate a serious electricity shortage in the nation. South Africa has faced rolling blackouts as Eskom works to repair poorly maintained coal-fire facilities, reports Bloomberg. The project is waiting on government approval before it can move forward and the costs are still unknown.

- Codelco announced that its $1 billion expansion of the Salvador copper mine was approved by Chile’s environmental regulators. The project, known as Rajo Inca, is expected to boost copper production by 90,000 tons per year, up from 60,000 tons, and extend the mine life by 40 years.

Threats

- The T. Boone Pickens fossil fuel fund that was rebranded into a renewable energy ETF has failed just five months after the transition. The Pickens Morningstar Renewable Energy Response ETF closed this week after failing to attract investors. Bloomberg writes that the fund was billed as a way to give investors exposure to companies that use, rather than produce, renewable energy, but the fund charged fees five times higher than rival offerings. Investor demand for renewable and “greener” funds continues to rise, but competition remains steep for smaller asset managers to stand up against the low fees of the largest players.

- ING Bank NV alleges that Agritrade International Pte, its CEO and his father mispresented the company’s financial position to several bank lenders, reports Bloomberg. According to the ING Bank filing, a group of 15 lenders held $600 million of Agritrade’s $1.5 billion of liabilities. Agritrade is one of many firms to come under financial strain amid low coal and oil prices.

- The chemical industry is the latest to be negatively impacted by the coronavirus’ effects on demand. BASF SE warned that it could have the lowest growth in production since the financial crisis and have a second straight year of falling profit. BASF is a major supplier of plastics and additives. The company said the epidemic will a major impact in the first two quarters of this year, which will not be fully offset during the second half of the year.

Emerging Europe

Strengths

- Turkey was the best relative performing country this week, losing 9.3 percent. Equities trading on the Istanbul exchange sold off sharply in the past five days, but still outperformed other markets in the region with support from domestic regulations. Reports over the coronavirus cases rapidly growing outside of China and escalating geopolitical tension in the Middle East prompted investors to sell.

- The euro was the best performing currency this week, gaining 1.7 percent. Single market currency appreciated after the U.S. dollar lost 1 percent in the past five days. Federal Reserve in the U.S. indicated that further rate cuts are possible if the coronavirus develops into worldwide pandemic.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 19.3 percent. The Greek banking index declined by 24 percent.

- The Russian ruble was the worst performing currency in the region this week, losing 4 percent. Weakness in the oil price and tensions with Turkey affected the price of the ruble. Brent crude oil dropped by 14.5 percent and fighting between Syrian forces (backed by Russia) and the Turkish army intensified in Northern Syria, with increased causalities on both sides.

- Consumer discretionary was the worst performing sector among eastern European markets this week.

Opportunities

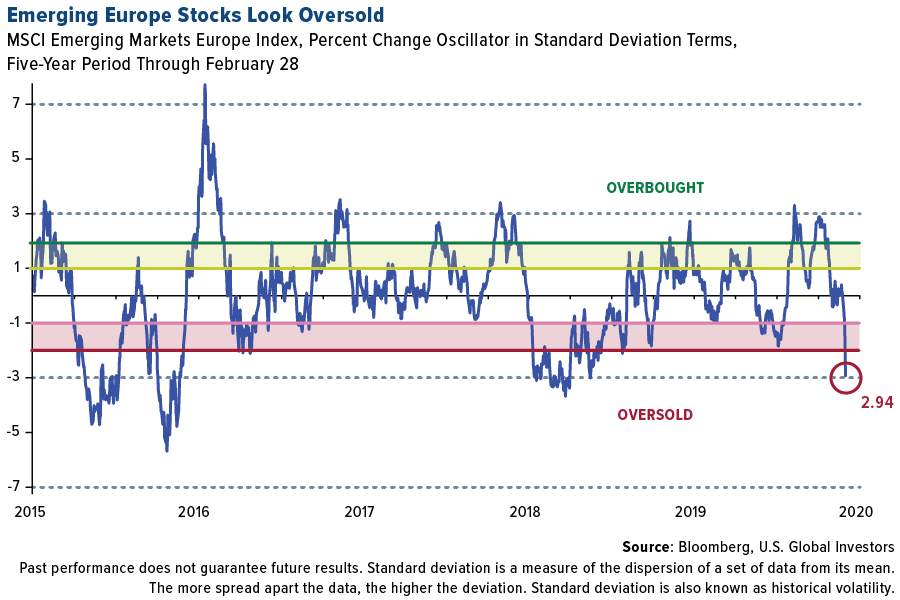

- Eastern European stocks, as measured by the MSCI Emerging Markets Europe Index, fell into oversold territory this week, and usually it presents a good buying opportunity.

- The Czech Republic may be ready for a recovery according to Bloomberg. The government, in power since 2018, already took advantage of better-than-expected tax collections to raise pensions and salaries for public workers. The country is well positioned to further increase spending, especially if growth slows below the annual 2 percent, as it has the lowest debt level in the European Union.

- Eurozone consumer confidence was stronger in the month of February at 103.5 versus an expected reading of 102.8. All sectors, except for construction, saw confidence improve or remain flat. The good news is that the manufacturing sector is bottoming out and with the inventory correction ending, the sector is set for a recovery. The bad news is that with the distortion of supply chains and trade flows caused by the coronavirus, the upturn will face delay.

Threats

- European airlines sold off this week on the threat that coronavirus will further hurt demand for air travel. Shares of Wizz Air, a low cost Hungarian airline, and Aegean, a Greek airline, lost more than 24 percent of their market share in the past five days. Shares of Lufthansa, Pegasus and Arofloat were also down over 20 percent.

- According to Bloomberg calculations, Turkey’s net foreign-currency reserves have dropped around $9 billion from the peak of late December, now standing at $35 billion, which only covers one fifth of Turkey’s foreign obligations over the next 12 months. “We are getting close to uncomfortable levels,” said Kaan Nazil, a senior economist and portfolio manager at Neuberger Berman in The Hague. He estimates Turkey has $6 billion in financing needs in the coming two months.

- Coronavirus cases in Italy are growing with the number of deaths at 12 as of late Thursday. Wood & Company believes that this creates strong downside risks for GDP growth for the eurozone. Central Emerging Europe, Russia and Turkey appear better positioned to weather this storm on the margin than the eurozone as they have full fiscal and monetary policy flexibility, according to Jarek Tomczynski.

China Region

Strengths

- Malaysia’s FTSE Bursa Malaysia KLCI closed down 3.14 on the week, while Taiwan’s Capitalization Weighted Stock Index finished down a “mere” 3.37 percent (it was closed Friday), while Hong Kong’s Hang Seng Composite Index (HSCI) finished down 4.36 percent.

- Properties and construction constituted the best relative sector performance in the HSCI for the week, falling only 1.68 percent.

- Estimates and media reports covering China are saying some 60 to 70 percent of people are now back to work, and China’s number of new reported cases have now, for multiple days, been outpaced by the rest of the world. This is admittedly a bit of a bizarre “strength,” and one hopes that all numbers globally begin dropping as soon as possible, but there is at least some measure of hope that China’s attempts at containment may have borne at least some fruit, either slowing or minimizing further spread of the virus even as it raised concerns and awareness.

Weaknesses

- Thailand’s SET Index led the way down this week, off by 10.19 percent even as coronavirus concerns rose in that country—among others—meaning Thailand had plenty of company down in the red on the week. South Korea’s KOSPI Index closed down 8.13 percent, the Philippines’ PSE Composite Index closed down 7.90 percent and Indonesia’s Jakarta Composite Index finished down 6.74 percent. Indonesia still has no reported cases of coronavirus at this point, however.

- Energy was the worst-performing sector in the HSCI for the week, declining by 9.15 percent.

- China is set to release purchasing manager’s index (PMI) data heading into the weekend on Friday evening. Manufacturing PMI data will almost certainly—given the quarantines and shut downs around the lengthy holiday stretch—mark a significant drop into contractionary territory. The question is, of course, where we go from here.

Opportunites

- While the cash handout from the Hong Kong government to all permanent residents 18 and over—of some roughly $1284 USD—may not be seen until later in the year, Hong Kong’s Financial Secretary Paul Chan did announce it as part of a HK$120 billion spending package within the upcoming annual budget, which could provide useful stimulus to the troubled SAR that has, in the last year, been rocked by issues from trade war to violent protests to coronavirus concerns. HK sees its first budget deficit since 2004 expanding into 2021 to a record. The planned budget also entails various measures to target, Bloomberg reports, homebuyers, students, investors and small businesses. All told, the package represents some 4.2 percent of 2018 GDP.

- The blue-chip Hang Seng Index in Hong Kong now stands at a price-earnings ratio of 10.88. The S&P 500 is now at 19.48.

- While it very much remains open to be seen precisely how everything in U.S. presidential races play out through the primary season and into November, one notable development—one that may matter less as time goes on, or perhaps more—is former New York mayor Michael Bloomberg is more firmly pledging to de-escalate trade tension with China. Of course, at this stage in the race—long before anything is set in stone and when, to be blunt, “talk is cheap,” obviously—it may not even be worthy of much note to readers. But, at the same time, and as the former mayor is surely betting, simply starting a dialogue about starting a different dialogue could set up a platform for more discussion about China and trade policy down the road. This is not to say or make any argument either for or against any one candidate nor indeed make any commentary on present policy—remember, we’ve only just concluded Phase One signings under the Trump administration as we headed into Lunar New Year and the coronavirus issue—as much as it is simply to point out perhaps, from either or both sides, as China and trade policy eventually return to the forefront, we’ll see further development of ideas or possibilities that may make for intriguing economic opportunities.

Threats

- Coronavirus confirmed-case concerns continue. The World Health Organization (WHO) raised the global risk outlook from “high” to “very high,” though they’ve held off the “P” word of pandemic at this point. But with more than 84,000 cases worldwide, nearly 3,000 deaths, and a rising threat of a community spread, markets got a bit jittery this week. Commentary over the last few days from Centers for Disease Control and Prevention (CDC) officials that community spread in the U.S. is a fait accompli (“… not so much a question of if this will happen anymore but rather more a question of exactly when …”) did not appear to help market perceptions. Markets are, however, notoriously jittery, and also extrapolate out into the future, weighing possibilities and sometimes overreacting. Nonetheless, while it is encouraging that China’s pace of infections has slowed and much of the country appears to be returning to work, we have—as mentioned above—now had consecutive days of more cases confirmed outside China than in. At some point, one imagines, a true pandemic could trigger reinfections and continued cross-border disruptions to commerce globally and in the China Region.

- The threat and flipside from the stated opportunity about the new HK budget is that, as Financial Secretary Chan pointed out, the SAR’s first quarter GDP will likely be “rather bad.”

- The 94 year-old prime minister Mahathir Mohamad of Malaysia has submitted his resignation and exited the ruling coalition, receiving an appointment from the king as Interim PM until a successor emerges from the ensuing leadership struggle. Malaysia, still reeling, in some ways, from the 1MDB scandal, now faces a degree of additional uncertainty even as coronavirus concerns have hit the broader region.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 28 was WhiteCoin, up 142.00 percent.

- CoinDesk reports that Hong-Kong based crypto derivatives exchange FTX saw record high volumes in ether futures on Wednesday despite a selloff in the coin’s price. The exchange is just nine months old and hit a daily trading volume high of $245 million, according to Skew Markets, which is a 51 percent increase from the day prior. Trading activity had been slow in early January, but grew exponentially over the last four weeks.

- In a shareholder letter released this week, Square’s Cash App said that nearly half of its revenue for the fourth quarter came from bitcoin. The company reported bitcoin revenue of $178 million – up 50 percent over the prior two quarters.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 28 was SounDAC, down 77.60 percent.

- The Securities and Exchange Commission (SEC) rejected the latest attempt at creating a bitcoin-based ETF. In a filing this week, the securities regulator noted that the alternative financial firm Wilshire Phoenix “had not proven the bitcoin market is sufficiently resistant to market manipulation,” according to an article in Coinbase.

- The SEC fined actor Steven Seagal for failing to disclose that he was paid to promote a digital token. Bloomberg reports that Seagal was promised $250,000 in cash and $750,000 worth of token for promoting an initial coin offering from Bitcoiin2Gen on social media posts. Seagal will settle the SEC’s allegations and pay a $157,000 fine and the same amount in disgorgement.

Opportunities

- An article this week in MIT Technology Review makes the case that the wind boom in Texas, home to U.S. Global Investors, may “redraw the global map of the bitcoin mining network,” becoming the next big “promised land for bitcoin miners.” This is thanks not only to the Lone Star State’s cheap wind-generated electricity, but also its welcoming regulatory environment. Some big players have already shifted projects to Texas in recent months, including Peter Thiel-backed Layer1 Technology and Bitmain, Chain’s leading mining chipmaker.

- The Bank of Canada announced this week that it is looking into the feasibility of creating its own cryptocurrency, should there be a need for one. Although the bank’s deputy governor, Tim Lane, does not see a compelling reason for one at the moment, he and the bank are keeping their options open. “The bank would do this as a trusted public institution,” Lane commented, “creating an official digital currency that is designed with the interest of the public as its top priority.”

- Chamath Palihapitiya, former Facebook executive and current Virgin Galactic chairman, said this week that everyone’s portfolio should have about a 1 percent weighting in bitcoin. Even retail investors “should view an investment in bitcoin as a sort of crisis insurance, which they keep under the mattress and hope they never need,” Palihapitiya said, adding that the virtual coin “will protect you because it will have a value of hundreds of thousands or millions of dollars per coin.”

Threats

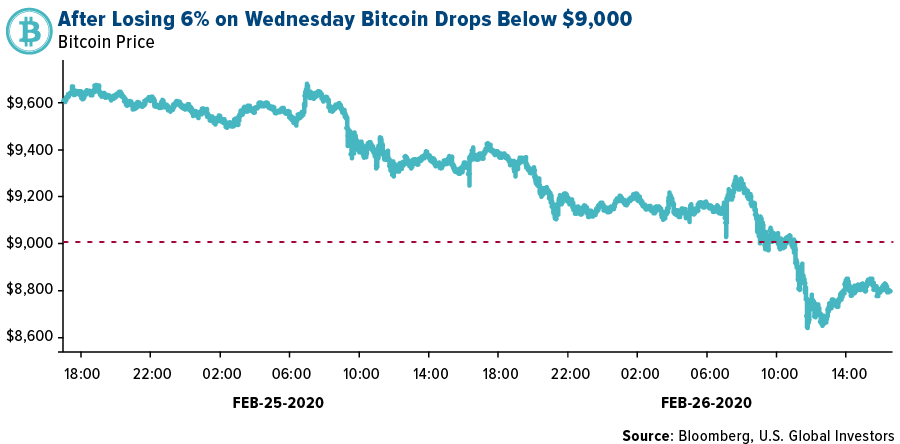

- The price of bitcoin tumbled this week along with global equities, calling into question its status as a store of value. From its 30-day high on February 13, the world’s largest digital currency by market-cap had lost as much as 15 percent through February 27. The rout wasn’t limited to bitcoin, either. The total market capitalization of all known cryptocurrencies declined some 8 percent in the seven-day period through February 27, from $276 billion to $254 billion.

- Finland’s customs agency has a stockpile of 1,666 bitcoin that it confiscated in an online dark market bust in 2016. Since then, the agency has been struggling with what to do with the coins, as it worries that auctioning them off would attract the wrong kind of attention, reports CoinDesk. Director Pekka Pylkkanen said to local media that “from our point of view, the problems are specifically related to the risk of money laundering. The buyers of [cryptocurrency]rarely use them for normal endeavors.”

- Japan’s Finance Minister Taro Aso warned against China’s digital yuan, which is expected to be released later this year, saying that more work is needed before issuance, reports Bloomberg. Aso told reporters at the G-20 financia chief meeting this week that “there is a big risk in a central bank digital currency unless the regulation is well-sorted.”

February 28, 2020Why Can’t Gold Go to $10,000? |

February 20, 2020Frank Holmes Says Invest in Gold Using Stocks and Jewelry |

February 19, 2020Why Frank Holmes Is Bullish on Mining Stocks |

|||

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.17 | -0.31 | -20.79% |

| Oil Futures | 45.16 | -8.22 | -15.40% |

| Hang Seng Composite Index | 3,601.21 | -164.18 | -4.36% |

| S&P Basic Materials | 330.67 | -48.24 | -12.73% |

| Korean KOSPI Index | 1,987.01 | -175.83 | -8.13% |

| S&P Energy | 343.53 | -62.40 | -15.37% |

| Nasdaq | 8,567.37 | -1,009.22 | -10.54% |

| DJIA | 25,409.36 | -3,583.05 | -12.36% |

| Russell 2000 | 1,476.43 | -202.18 | -12.04% |

| S&P 500 | 2,954.22 | -383.53 | -11.49% |

| Gold Futures | 1,580.90 | -67.90 | -4.12% |

| XAU | 94.15 | -16.91 | -15.23% |

| S&P/TSX VENTURE COMP IDX | 497.61 | -85.06 | -14.60% |

| S&P/TSX Global Gold Index | 249.01 | -33.92 | -11.99% |

| Natural Gas Futures | 1.70 | -0.21 | -10.97% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 1,987.01 | -198.27 | -9.07% |

| 10-Yr Treasury Bond | 1.17 | -0.42 | -26.44% |

| Gold Futures | 1,580.90 | +4.90 | +0.31% |

| S&P Basic Materials | 330.67 | -41.68 | -11.19% |

| S&P 500 | 2,954.22 | -319.18 | -9.75% |

| DJIA | 25,409.36 | -3,325.09 | -11.57% |

| Nasdaq | 8,567.37 | -707.80 | -7.63% |

| Oil Futures | 45.16 | -8.17 | -15.32% |

| Hang Seng Composite Index | 3,601.21 | -106.42 | -2.87% |

| S&P/TSX Global Gold Index | 249.01 | -14.25 | -5.41% |

| XAU | 94.15 | -8.96 | -8.69% |

| Russell 2000 | 1,476.43 | -172.79 | -10.48% |

| S&P Energy | 343.53 | -71.59 | -17.25% |

| S&P/TSX VENTURE COMP IDX | 497.61 | -79.88 | -13.83% |

| Natural Gas Futures | 1.70 | -0.18 | -9.64% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 94.15 | +0.22 | +0.23% |

| S&P/TSX Global Gold Index | 249.01 | +7.83 | +3.25% |

| Gold Futures | 1,580.90 | +114.90 | +7.84% |

| DJIA | 25,409.36 | -2,754.64 | -9.78% |

| S&P 500 | 2,954.22 | -199.41 | -6.32% |

| Nasdaq | 8,567.37 | -137.81 | -1.58% |

| Korean KOSPI Index | 1,987.01 | -131.59 | -6.21% |

| Natural Gas Futures | 1.70 | -0.81 | -32.19% |

| S&P Basic Materials | 330.67 | -46.29 | -12.28% |

| Russell 2000 | 1,476.43 | -157.67 | -9.65% |

| Oil Futures | 45.16 | -12.95 | -22.29% |

| Hang Seng Composite Index | 3,601.21 | -48.18 | -1.32% |

| S&P/TSX VENTURE COMP IDX | 497.61 | -34.70 | -6.52% |

| S&P Energy | 343.53 | -92.25 | -21.17% |

| 10-Yr Treasury Bond | 1.17 | -0.60 | -34.01% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

Aegean Airlines SA

WizzAir Holdings Plc

Deutsche Lufthansa AG

Pegasus Hava Tasimaciligi AS

Eni SpA

Polymetal International PLC

New Gold Inc

OceanaGold Corp

Impala Platinum Holdings Ltd

MMC Norilsk Nickel PJSC

TriStar Gold Inc

American Airlines Group Inc

Adidas AG

Ivanhoe Mines Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MSCI Emerging Markets Europe Index captures large and mid-cap representation across 6 Emerging Markets (EM) countries in Europe. With 70 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Bloomberg U.S. Financial Conditions Index provides a daily statistical measure of the relative strength of the U.S. money markets, bond markets, and equity markets, and is considered an accurate gauge of the overall conditions in U.S. financial and credit markets. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility. The relative strength index (RSI) is a momentum indicator developed by noted technical analyst Welles Wilder, that compares the magnitude of recent gains and losses over a specified time period to measure speed and change of price movements of a security. It is primarily used to attempt to identify overbought or oversold conditions in the trading of an asset. The Stock Exchange of Thailand SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand. The FTSE Bursa Malaysia Index Series is a broad range of real-time indices, which cover all eligible companies listed on the Bursa Malaysia Main and ACE Markets. The indices are designed to measure the performance of the major capital segments of the Malaysian market, dividing it into large, mid, small cap, fledgling and Shariah-compliant series, giving market participants a wide selection and the flexibility to measure, invest and create products in these distinct segments. The Philippine Stock Exchange PSEi Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services, Holding Firms, Financial and Mining & Oil Sectors of the PSE. The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange. Free cash flow represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.