2018 is the Biggest Baton Pass in History

By Herb W. Morgan, III, Efficient Market Advisors

Like that party that just keeps going past midnight, it seems nobody told the equity markets 2017 has ended. At this writing, the S&P500 Index is up 6.3% in 2018, the MSCI EAFE Index is up a similar 6.5% and the MSCI Emerging Markets Index tops them all with an 8.7% return[1]. All of this, while echoes of Burns’ Auld Lang Syne are still rattling in our champagne-soaked heads. But soon the market’s momentum will meet the reality of the economic, corporate and geo-political developments of 2018. One cannot live on momentum alone. So, will the fundamentals ultimately deliver more upside or should investors be less sanguine?

I have yet to come across an economic or market pundit who posits that the historic rise in equity prices was not fueled by over $8T in central bank liquidity. Combined, the US Federal Reserve, the European Central Bank, the Bank of Japan and others injected over $8T into global financial markets to successfully fight deflation, encourage risk taking and prevent a global depression. All along, central bankers themselves have argued they should not be fully responsible for the management of their respective economies. The US Fed has acknowledged it is time they began the retreat to the shadows to toil away in green eye-shades until needed again as a lender of last resort.

The US has finally embarked upon a pro-growth fiscal and regulatory regime. Yet both the Fed & private sector are still attached to the baton of responsibility. This baton pass will not be at relay-race speed but rather in ultra-slow motion as a baton drop could prove disastrous to the global economy.

At Efficient Market Advisors (EMA), we don’t think anyone is in a rush when it comes to Quantitative Tightening or QT. But the minute inflation metrics show up the debate is apt to get fierce. With inflation, we suspect our old friend volatility will break up the party faster than the cops at a high-school kegger.

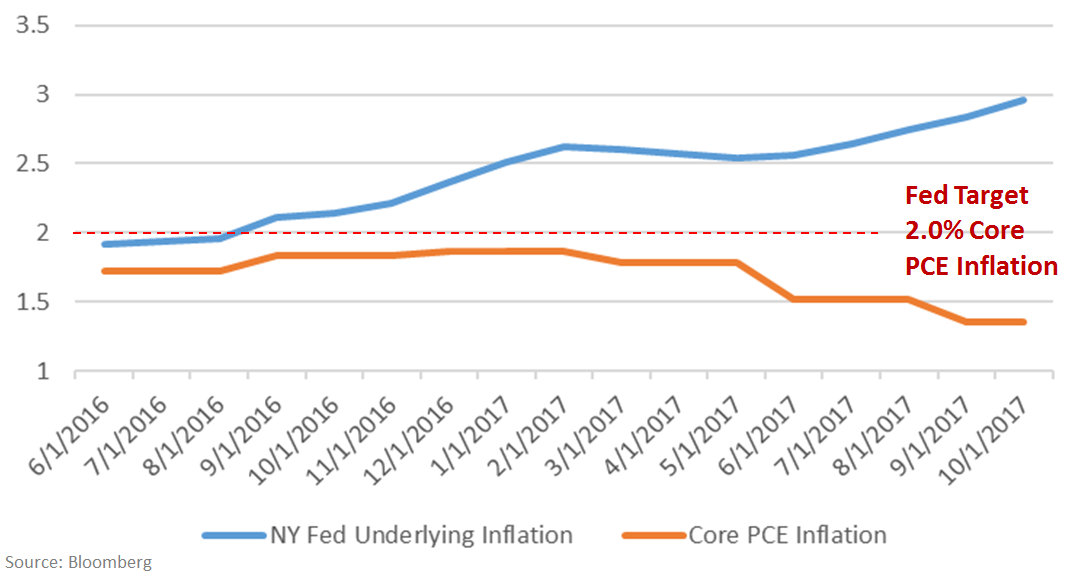

While the Fed assesses its price stability mandate by the level of the Core PCE Price index, there are many other gauges of inflation suggesting that prices are on the rise. One such indicator, the Federal Reserve Bank of New York’s Underlying Inflation Gauge, a highly regarded leading metric of inflation, already has inflation at three percent. With the Core PCE Price Index at 1.5%[2], it’s only a matter of time before the Fed’s own forecasts force them to either slow the economy or cave to the likely political pressure around their Core PCE target by raising it or seeking an entirely different definition of price stability.

Inflation Could Prove a Problem Later in 2018

Inflation Could Prove a Problem Later in 2018

There is no doubt innovation and disruption are supportive of some serious deflationary pressures in many sectors of the economy. However, the reality of rising commodity prices, a tight labor market, rising capacity utilization and a falling US Dollar all support the conclusion that inflation may find its way into the Core PCE Index later in 2018.

The US Federal Funds Rate has been hiked 5 times starting in December 2015[3] and may well be increased three more times in 2018 to pre-emptively stave off inflation. And the Fed began buying fewer bonds in October of 2017 by not reinvesting $10B per month of maturing proceeds. That amount doubled to $20B in January and is expected to rise to $50B a month in the fourth quarter of this year. Further, the ECB is decreasing its monthly purchases and may well end them in 2018. The Bank of Japan remains less predictable. The bottom line is, the QE that drove asset prices higher peaked in March of 2017 and net combined QE of the Fed, BOJ and ECB will likely turn to Quantitative Tightening (QT) by January of 2019[4].

Can asset prices continue to rise in the absence of QE and the onset of outright QT?

To be sure, the US has taken the lead with deregulation, competitive corporate tax rates and stands the best chance of any major economy in achieving a successful baton pass. Still, the risks of a volatile baton pass or an outright fumble are real so we at EMA remain at our policy benchmark weightings in equities.

Fixed income markets, on the other hand, seem to be underpricing the risk of an inflationary uptick. Investors in long duration fixed-income ETFs could be in for a nasty surprise should inflation rise from today’s levels. As such, EMA has positioned client portfolios well below our policy benchmark weight for fixed-income placing the difference into liquid alternative ETFs. Recently we added ETFs Securities Bloomberg All Commodity Strategy K-1 Free ($BCI) to our portfolios. This complements the position in energy MLPs we initiated in early 2016 via both the Alerian MLP ETF ($AMLP) and the Global X MLP ETF ($MLPA).