The Fed is set to meet Wednesday of this week to discuss plans for tapering and accelerating the original deadline from June to potentially March. The meeting follows November’s CPI report of continued rising inflation and bond markets giving warning signs of impending economic pullback via the yield curve, reports the Financial Times.

So what exactly is the yield curve, and why does it matter? The yield curve in a developed country is essentially a reflection of investor confidence in the performance of the economy looking forward. It’s a measure of the interest rate that buyers of government debt want for their various term loans, whether they are short- or long-term.

Short-term yields are generally a barometer for investor sentiment towards central bank policies in the immediate future, while longer-term ones are generally a measurement of where investors believe policies are headed in the intermediate to far future when it comes to growth, inflation, and interest rates.

“People get excited about the yield curve because, historically, it has been a good predictor of the onset of recession,” said Richard McGuire, fixed income strategist at Rabobank.

In times of growth and positive investor outlook, the yield curve is steeper because strong economic growth can eventually create inflation as demand begins to outpace supply, and central banks are anticipated to raise rates as a response.

In times of economic slowdown, the yield curve flattens and can even invert, signaling economic recession. Yields for 10-year and 30-year bonds fall in the direction of shorter-maturity bonds as investors bet on reduced interest rates and minimal intervention due to lack of inflationary pressures.

How the Pandemic Has Impacted the Yield Curve

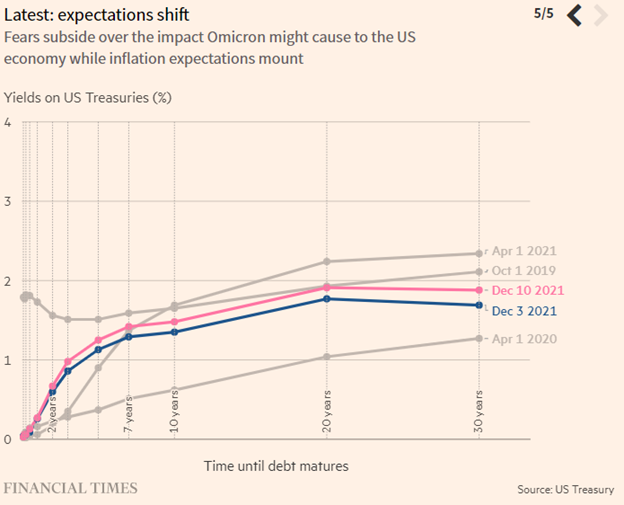

Towards the end of 2019, the yield curve had inverted, signaling an impending recession, and then the pandemic struck, sending the economy spiraling regardless. The yield curve rose sharply in 2021 due to economic recovery and wording from the Fed that indicated continued low interest rates, thereby allowing inflationary pressures to build more strongly and leading to potential higher rate increases down the line.

Image source: The Financial Times

The pandemic has played a bit of yo-yo with the yield curve since then; late spring saw investors expecting long-term economic growth to end sooner than anticipated, and then a rise again towards the end of summer in anticipation of the Fed announcing tapering of its stimulus that was aimed at long-maturity bonds. High inflation drove the yield curve flatter once more at the end of September, and now investors are betting on rapid short-term interest rate increases, thereby driving up short-term yields, and long-term bond yields fell on fears of Omicron’s economic impact.

While the yield curve has traditionally been viewed as the next best thing to a crystal ball for economic growth, some analysts are now arguing that the bond purchases by the Fed have created a distortion within bond markets and affected the accuracy of the yield curve prediction.

With so much uncertainty, particularly about the yield curve and the volatility in markets of late, relying on active management can provide assurance for investors that their portfolios are aligned with current and forward-looking market expectations. Active management helps eliminate much of the noise and stress of investing, particularly within bond markets that are digesting inflationary pressures, Omicron impact fears, and a host of other components.

“One of the reasons many advisors turn to active when it comes to fixed income is that managing duration risk isn’t straightforward,” said Dave Nadig, ETF Trends’ director of research. “The narrative changes almost daily based on economic data and Fed tea leaf reading. Knowing there’s a pro paying attention can often help investors sleep at night.”

Active management firm T. Rowe Price believes in the difference and benefits to active investing and active management. The firm currently offers eight actively managed ETFs for investors that are looking for a variety of options, including the the T. Rowe Price Ultra Short-Term Bond ETF (TBUX) within bonds, an ETF that seeks to have a portfolio with an effective duration of 1.5 years or less. TBUX carries an expense ratio of 0.17%.

For more news, information, and strategy, visit the Active ETF Channel.