Our Cash Indicator methodology acts as a plan in case of an emergency. This is analogous to the multiple safety systems in a modern automobile, which includes an airbag. Importantly, each of these systems work together to potentially help smooth the ride.

We manage risk within our strategic, long-term allocations based on diversification across equity, fixed income, and alternative assets and a focus on more attractive relative values.

We manage risk tactically over the short-term by investing across a broad array of themes and asset classes including cash. We can either invest opportunistically or defensively depending on the environment.

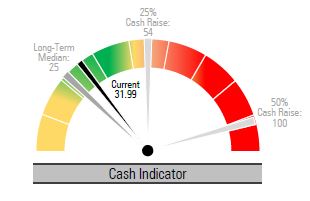

Cash Indicator: Markets are functioning properly but we expect continued volatility.

Our proprietary Cash Indicator (CI) provides insight into the health of the market by monitoring the level of fear using equity and fixed income indicators. This warning system is designed to signal us to either a 25% or 50% cash position to potentially protect principle and provide liquidity to reinvest at lower and more attractive valuations.

Our proprietary Cash Indicator (CI) provides insight into the health of the market by monitoring the level of fear using equity and fixed income indicators. This warning system is designed to signal us to either a 25% or 50% cash position to potentially protect principle and provide liquidity to reinvest at lower and more attractive valuations.

After elevating earlier this year, the CI has fallen back to more normal levels. Equity fear subsided in July and bond markets reflect less concern. While the markets still have a lot of global uncertainty to digest, the CI suggests that markets are operating normally at this level.

Strategic View: The recent market rally makes equities fairly valued and long-term bonds expensive.

Equity Valuations: Equity valuations bounced back with the strong July rally and now look fairly valued overall.

Equity Valuations: Equity valuations bounced back with the strong July rally and now look fairly valued overall.

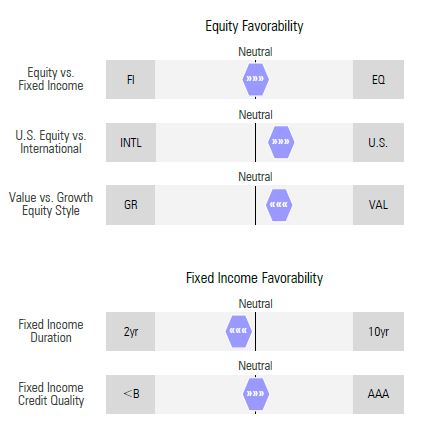

Equity Favorability: We continue to favor U.S. equities over foreign. Though we still hold high quality and defensive foreign assets, in recent months we have reduced our foreign exposure in favor of cash and high yield corporate bonds.

Fixed Income Valuations: Long-term interest rates may be range bound as markets adjust to changing inflation and economic outlooks. The 10-year Treasury yield looks expensive under 3% while very short-term interest rates should move higher based on central bank policy.

Fixed Income Favorability: We have been adding to intermediate-term core and high-quality longer duration positions as the 10-year Treasury moves above 3%. We continue to favor floating rate bonds on the short-end of the yield curve, such as collateralized loan obligations, while adding floating rate Treasuries in addition to short and intermediate duration investment grade mortgage-backed and asset-backed securities.

Tactical View: We favor equities with consistent earnings and intermediate duration fixed income.

Despite the two quarters of GDP decline, our work suggests that the U.S. economy’s solid and slow economic growth will continue. We recently increased our allocation to the information technology sector while also favoring financials, health care, small cap value, global low volatility, and cash. We added floating rate Treasuries and reduced our underweight to fixed income interest rate sensitivity by adding to core assets, high yield corporate bonds, and intermediate duration Treasury bonds.

| Equity | U.S. » financials*, health care*, technology*, small cap value*

Global » low volatility, quality |

| Fixed Income | cash*, high yield bonds*, short and intermediate-duration asset-backed and mortgage-backed securities, floating rate* and intermediate-term Treasuries, taxable munis* |

| Alternatives | multi-sector income, put option overlay strategies* |

*areas that we are tactically emphasizing

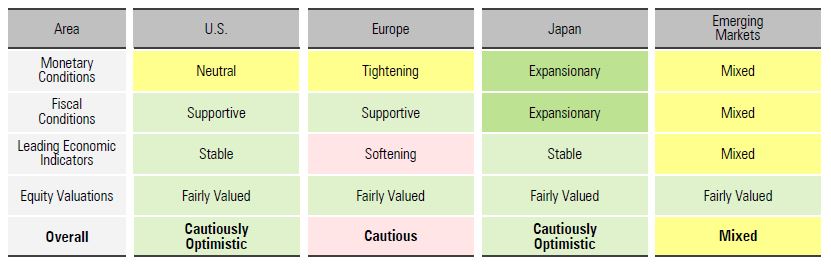

Global Broad Outlook: We are concerned about Europe and cautiously optimistic about most other regions.

Any forecasts, figures, opinions, or investment techniques and strategies explained are Stringer Asset Management LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. The views and opinions expressed are soley those of the original authors and other contributors. This material is for informational purpose only. Investments discussed may not be suitable for all investors. No part of the authors’ compensation was, is, or will be directly or indirectly related to the specific views contained in this report. Information provided is obtained from sources deemed to be reliable; but is not represented as complete, and its accuracy is not guaranteed. Past performance is not indicative of future results. The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.