- Several companies across the energy infrastructure landscape were active with their repurchase programs in 1Q22, albeit at mostly modest amounts.

- Energy infrastructure companies repurchased $370 million of their equity in aggregate during the first quarter of 2022.

- Combining the last four quarters, energy infrastructure companies have spent $2.1 billion on equity repurchases.

The energy infrastructure space has seen several positive developments in recent years, including improvements to balance sheets, the shift to significant free cash flow generation, and progress with ESG metrics. One of the most poignant changes for midstream investors may be the proliferation of buyback programs, particularly given a history of frequently tapping equity markets to fund growth projects. The evolution of midstream/MLPs from frequent equity issuances to self-funding equity to now buying back equity marks a notable transformation. Today’s note recaps energy infrastructure buyback activity in 1Q22 and discusses why the data should be encouraging to investors, despite a lower overall spend on buybacks.

1Q22 buyback spend moderates – no showstoppers but lots of participation trophies.

Energy infrastructure companies repurchased $370 million(1) of their equity in aggregate during the first quarter. This represents a slowdown from the total repurchases seen in 4Q21 and 3Q21 of $650 million and $800 million, respectively, but is above the $300 million spent in 2Q21. Combining the last four quarters, energy infrastructure companies have spent $2.1 billion on equity repurchases. For context, the total North American energy infrastructure market capitalization was $603 billion at the end of the first quarter.

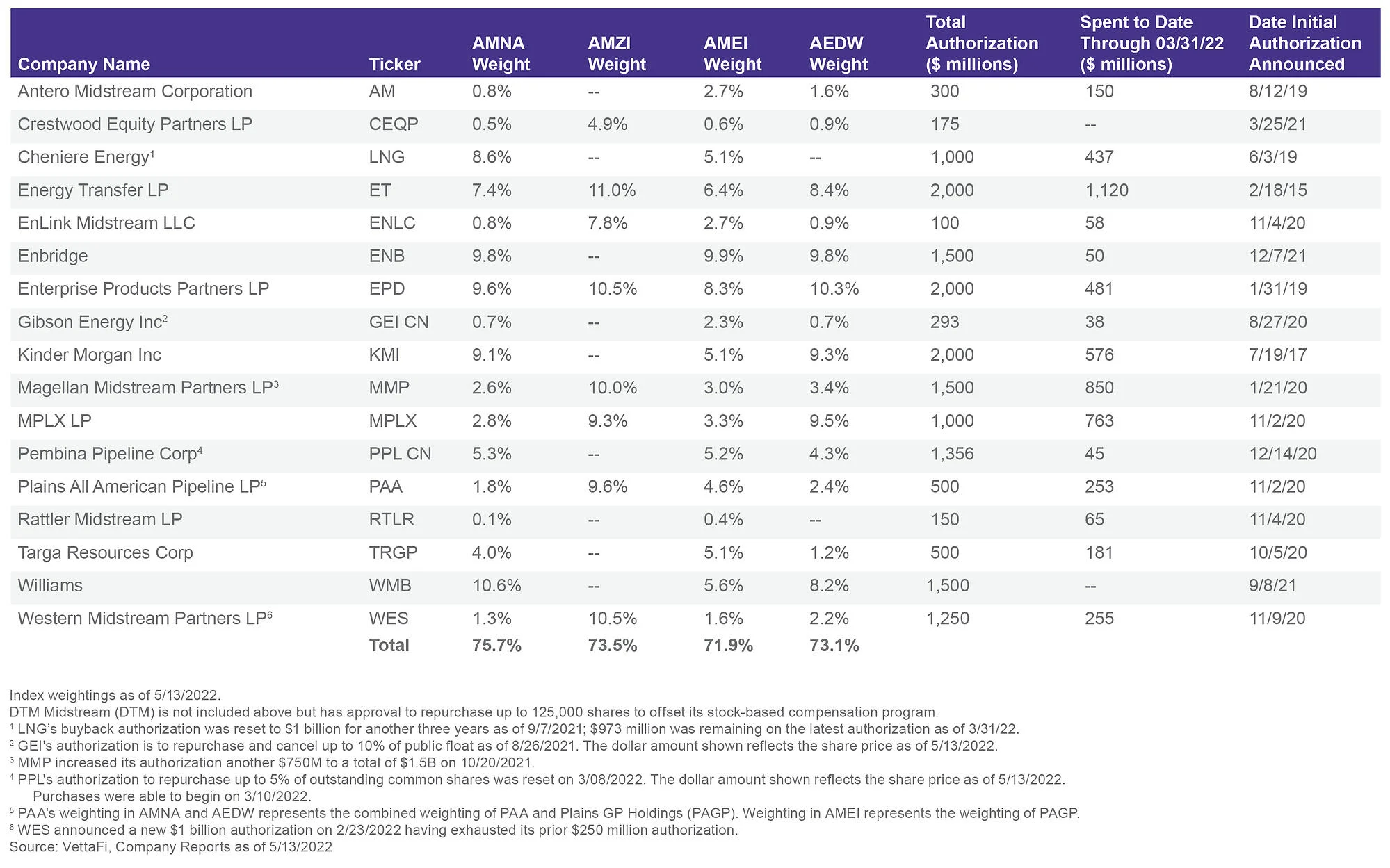

Several companies across the energy infrastructure landscape were active with their repurchase programs in 1Q22, albeit at mostly modest amounts. Leading the way, MPLX (MPLX) spent $100 million on repurchases in the quarter. Targa Resources (TRGP) and Magellan Midstream Partners (MMP) both spent $50 million on buybacks, while Cheniere (LNG), EnLink (ENLC), and Plains All American (PAA) repurchased approximately $25 million of their equity. Turning to Canadian corporations, Enbridge (ENB CN) spent CAD $50 million on buybacks in 1Q22 under its relatively new authorization. Pembina (PPL CN) repurchased CAD $28 million in equity in 1Q22, while Gibson Energy (GEI CN) completed CAD $19 million in buybacks during the quarter.

The table below shows the energy infrastructure companies with buyback authorizations in place, how much each has spent on repurchases, and each company’s weighting in the Alerian Midstream Energy Index (AMNA), Alerian MLP Infrastructure Index (AMZI), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Dividend Index (AEDW) as applicable. Constituents with buyback programs account for more than 70% of each index. For AMNA, the broadest midstream benchmark in the Alerian index suite, just over 75% of the index by weighting has a buyback authorization in place.

What is the takeaway from 1Q22 buyback activity for midstream investors?

With strong performance to start 2022, we flagged the potential for buybacks to moderate, particularly for those that emphasize an opportunistic approach and that have seen significant equity price appreciation. Arguably, most investors would likely prefer companies spend more on buybacks when their equity prices are lower and spend less when equity prices are rising. Quarterly buyback spend is likely to fluctuate as management teams consider equity valuations, capital needs, and returning cash to shareholders through dividends. With midstream names expected to generate significant free cash flow even after dividends, buybacks are likely to remain an attractive option for deploying excess cash flow and can complement growing dividends (read more).

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND).

(1) Aggregate dollar amounts include Canadian dollars for the Canadian corporations with repurchase programs – Enbridge, Gibson Energy, and Pembina Pipeline Corporation.

Related Research:

MLPs Leading the Way for Midstream Buybacks in 4Q21

Midstream/MLPs: Buybacks Accelerated in 3Q21

1Q22 Midstream Dividends and the Outlook for Variable Payouts