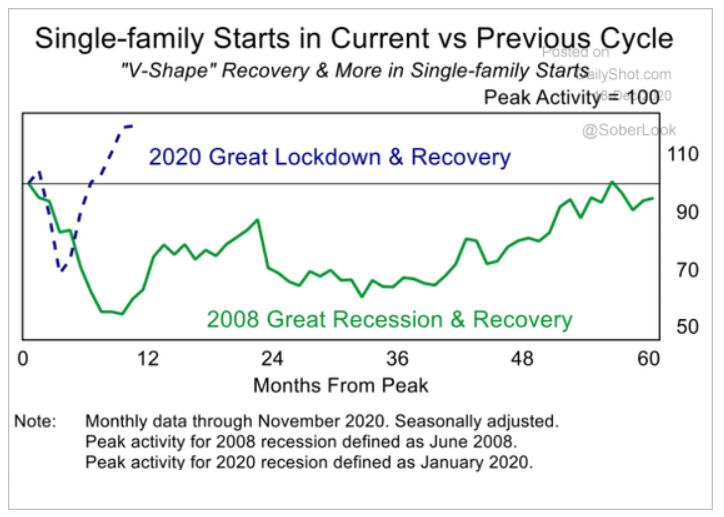

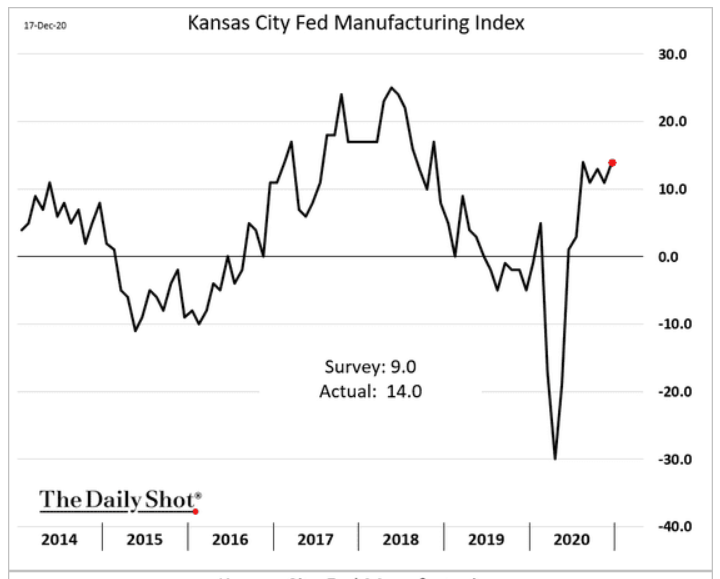

The housing market is still booming and contractors are racing to meet demand, bringing single family housing starts to their highest level since 2007. Manufacturing has softened across the U.S. (despite experiencing a small bump in KC), but the same can’t be said for equities—stocks closed at all-time highs yesterday as anticipation grows for a long-awaited stimulus deal and FDA approval of Moderna’s Covid vaccine. The March market rout and these new record highs aren’t the only reasons it’s been a historic year for equities though. Meanwhile, Bitcoin made headlines again this week, but is it enough to justify bullishness on crypto? And are you keeping an eye on the quality of your investment-grade debt?

Source: The Daily Shot, from 12/18/20

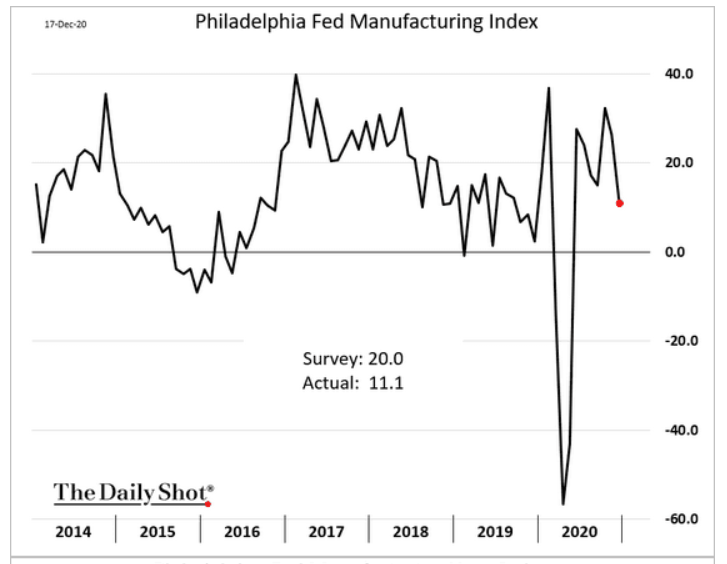

2. Another softening of a regional Fed survey as Covid surges…

Source: The Daily Shot, from 12/18/20

3. The Patrick Mahomes effect?

Source: The Daily Shot, from 12/18/20

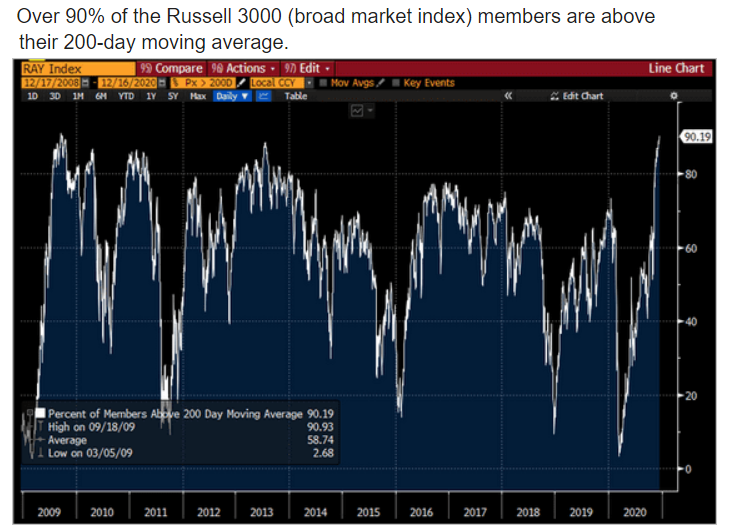

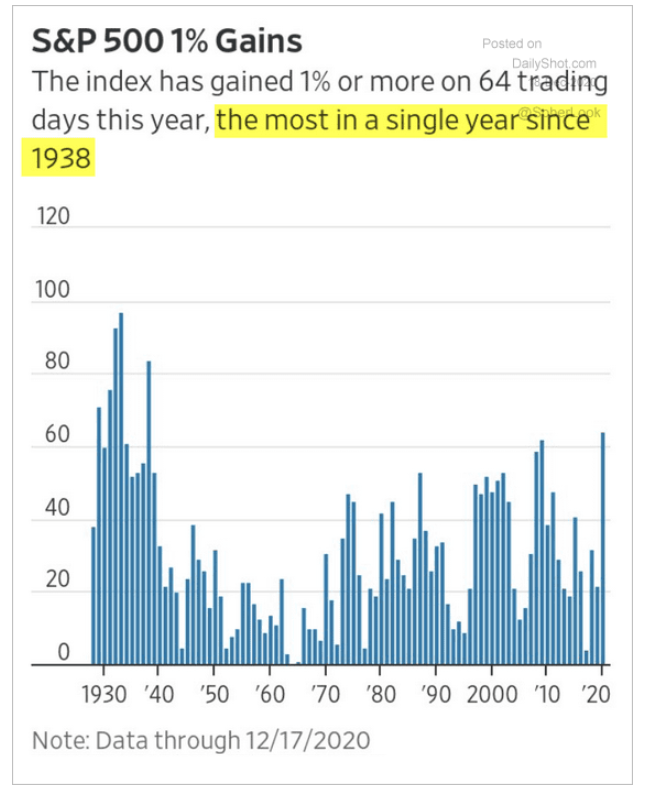

4. Do the markets need to “rest” a bit to keep this rally intact?

Source: The Daily Shot, from 12/18/20

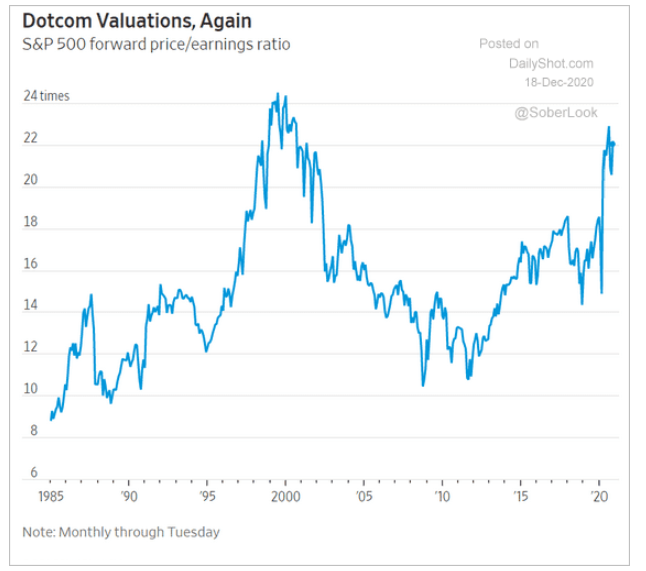

5. Just how frothy are the markets? Another historical view:

Source: The Daily Shot, as of 12/17/20

6. Another historical metric… and adding Tesla will only make the S&P 500’s P/E go higher…

Source: The Daily Shot, from 12/18/20

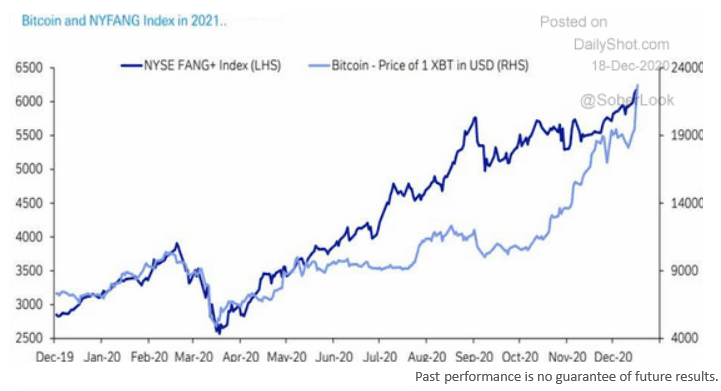

7. Sublime to the ridiculous…FAANG companies have products/services, revenue, earnings, strong market positions, employees, pay taxes, and the ability to increase all of these. Bitcoin has?

Source: Bloomberg, from 12/18/20

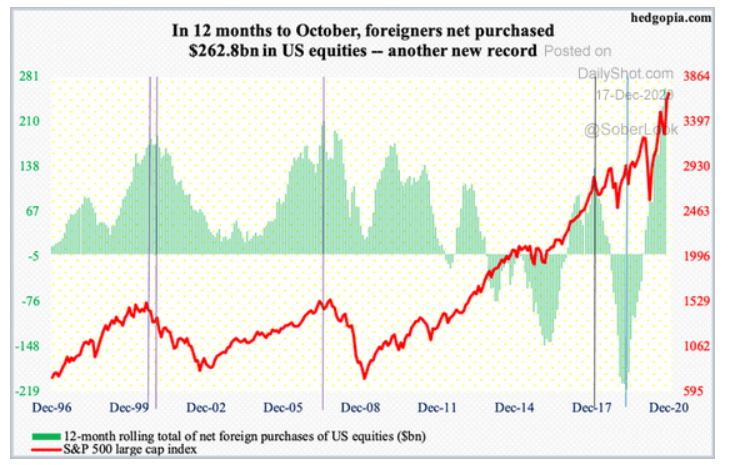

8. Another tailwind for the U.S. stock markets: foreign purchases set a new record…

Source: The Daily Shot, from 12/17/20

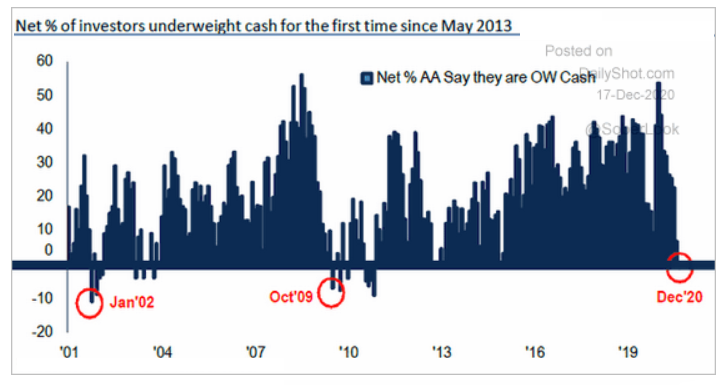

9. However, U.S. investor cash levels are indicating the dry powder is mostly spent.

Source: BofA Global Fund, from 12/17/20

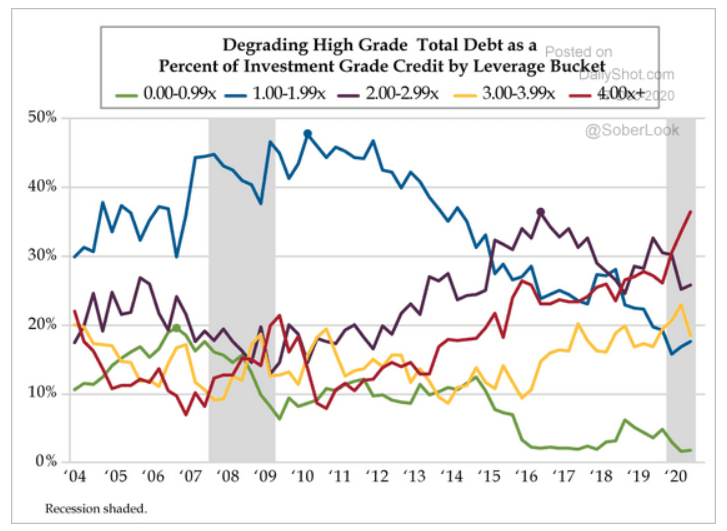

10. The quality of U.S. inv’t grade debt has deteriorated over the last ten years… leverage of 4x or more is now well over a third of the bonds…

Source: Bloomberg, from 12/17/20

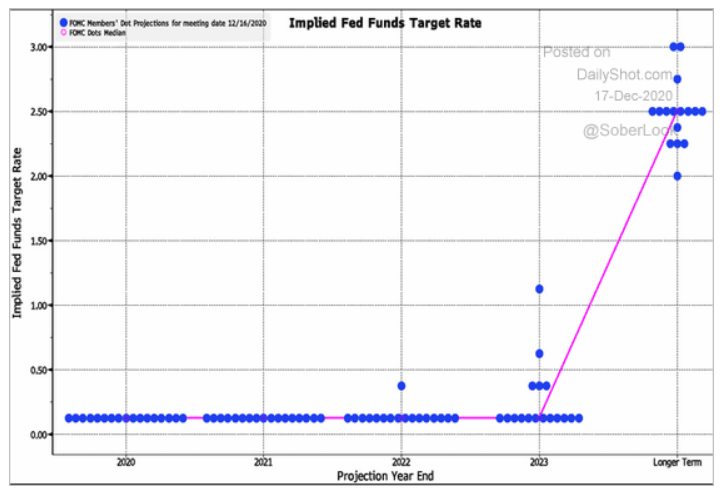

11. The Fed (FOMC) reaffirmed their commitment to near zero interest rates through 2023 as well as their QE of $120 billion/month

Source: The Daily Shot, from 12/17/20

12. Near-zero rates in the U.S. look generous…

Source: The Daily Shot, from 12/17/20

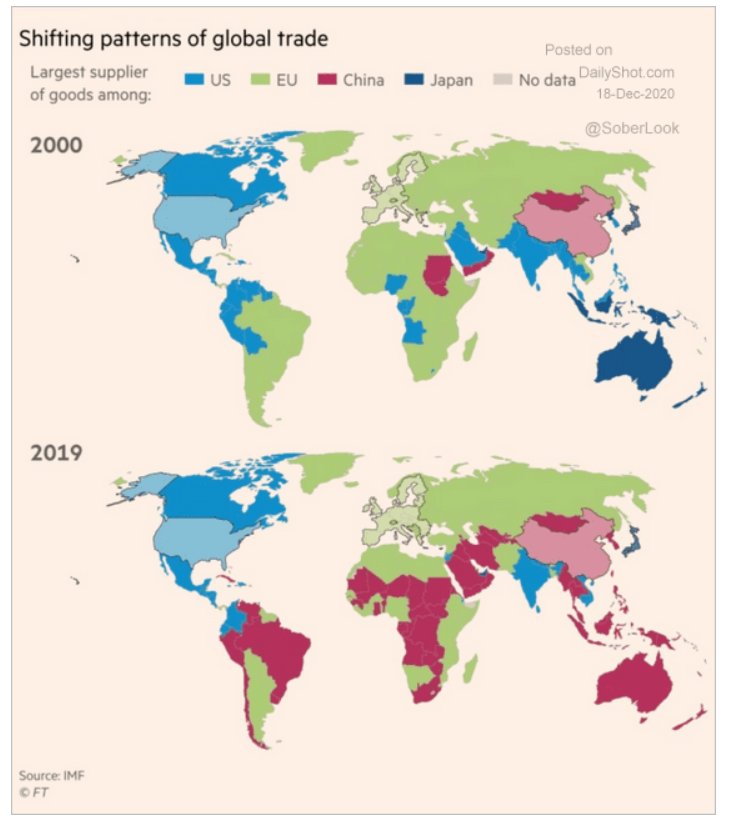

13. Trade brings influence…

Source: The Daily Shot, from 12/18/20

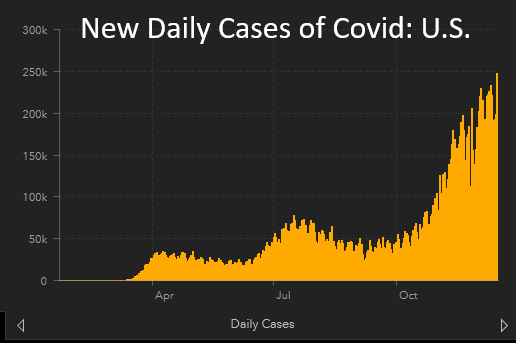

14. New daily cases of Covid has reached 250,000 in the U.S., ~600,000/day worldwide…

Source: JHU CSSE, from 12/17/20

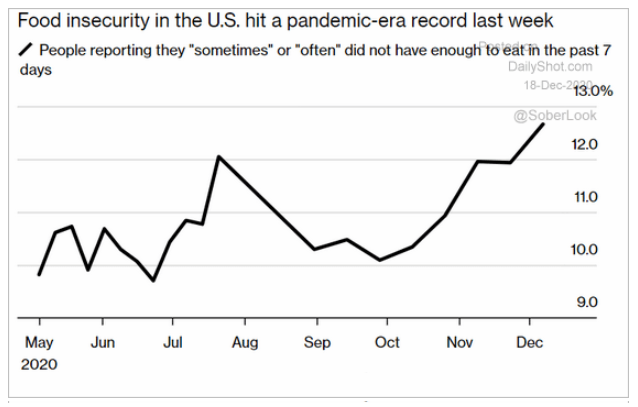

15. Please, help if you can…

Source: The Daily Shot, from 12/18/20