Thanksgiving is a time to pause and reflect on many things we often take for granted: health, time spent with loved ones, or just getting through another day in this weirdest of years. In such a tumultuous time, it’s easy to forget that we Americans still have a lot to be thankful for. Our doctors, health care workers, teachers, and front-line workers taught us a lesson in courage as they kept our economy and society moving forward this year under extreme duress.

Due to their work and the efforts of policymakers to offset the lockdown-induced economic drop in the spring, US economic activity and sentiment has rebounded sharply from its spring low. Purchasing manager index (PMI) surveys from the US are now close to 60, a level that historically suggests the economy is exiting recession (see chart, right). Employment has also snapped back from its largest collapse on record, though industries related to travel and hospitality remain dislocated.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

‘Ingenuity Over Infection’: Vaccines on The Horizon

We are also very thankful for the ingenuity of scientists. Thanks to unprecedented collaboration across the globe, researchers were able to decode COVID-19’s genetic sequence quickly, allowing the first vaccine to reach trials just 69 days after the identification of the virus. This compares to other recent infamous coronaviruses such as MERS (2014) and SARS (2003), which took 22 and 25 months respectively. In our opinion, because of these advances, countless lives will be saved and the economy will heal more quickly.

Of the more than forty vaccines in clinical trial, five candidate vaccines are now in Phase III (final stage) clinical trials in the US and Europe, and preliminary results have been promising. Moderna and Pfizer’s vaccine candidates both registered 90%+ efficacy and subsequently filed for FDA approval towards the end of October.

Other promising vaccines also have shown well above the minimum efficacy considered to proceed. We believe that at least one or more drugs will be granted approval by the FDA before the end of the year. This should pave the way for distribution to at-risk populations (the elderly, front-line workers) by late 2020 and hopefully widespread distribution to the public in the first half of 2021.

While this is tremendous news for society and for the stock market, complications related to vaccine manufacture, distribution, and administration – not to mention trepidation among some to take a brand-new vaccine – are to be expected. According to some researchers, the US is not likely to reach herd immunity by early 2021, meaning that many vestiges of 2020 – work-from-home, periodic restrictions, mask-wearing requirements, and depressed air travel and restaurant usage may pervade for some or much of next year. But it’s worth stating that if human ingenuity can develop a cure in record time, we believe that same spirit will likely also find novel ways of improving distribution for such a critical mission.

‘Optimism Over Pessimism’: Market at Fresh All-Time Highs as Uncertainty Fades

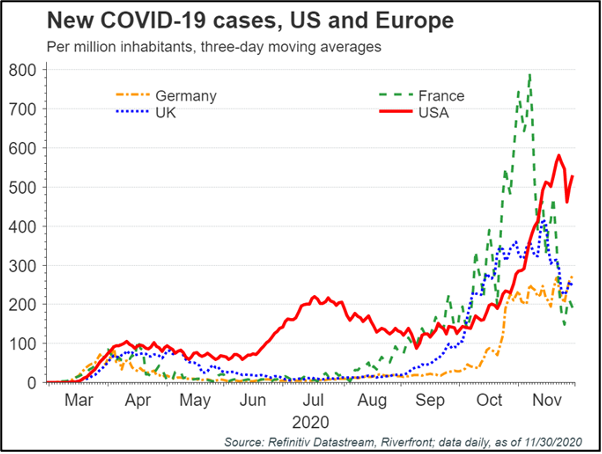

A cure can’t come fast enough; COVID-19 infections in the US and Europe continue to trend the wrong way as colder weather brings people inside and groups gather for the holidays (see chart right). However, the stock market is a forward-looking mechanism, willing to look through another COVID-19-induced economic ‘speedbump’. This is particularly true given that other major 2020 unknowns, such as the US election, are now behind us (see our views on the election in our 11.16.20 Weekly View).

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

The S&P 500 and Nasdaq hit all-time highs numerous times this fall, with the Dow Jones the latest to join in the party last week. While new highs in stock markets may scare investors fearful of a 2000 or 2008-style top, we think they are bullish signals. Participation is broadening with small-caps and value stocks also rising, a condition we view as encouraging for the health of the new bull market. RiverFront’s own proprietary technical tools, based on the slope and trend of the stock market, remain positive for short and intermediate-term time frames.

‘Process Over Prediction’: Riverfront’s Portfolio Positioning

Absolutely nothing about 2020 was predictable, and it’s a great example of why we view process as being more important than prediction in running portfolios. We believe that central bank policy and stock market sentiment hold important clues that can challenge investors’ preconceived notions and can help short-circuit emotional decision making. Our tactical process – focusing on our ‘Three Rules’ – helped guide us through a volatile, surprising and frankly exhausting year (view our 11.09.20 Weekly View for our Three Tactical Rules update).

- We remain overweight stocks vs bonds in our balanced asset allocation portfolios.

- We remain overweight the US as the most stable and strong economic region in our opinion, but have been adding to international stocks recently, given our views of potential further dollar weakness and a more positive trade backdrop with a Joe Biden presidency.

- Within the US, we have been adding to our equity exposure since the election and vaccine news. Our recent purchases have predominately been value-oriented, as we increasingly expect some catch-up for these types of stocks in the first half of the year. A few of our preferred themes here include infrastructure and cyclical industrials.

- We still maintain a preference toward a number of growth themes, as we expect COVID-19-driven changes in consumer and business behavior to persist. In particular, we remain constructive on software and data warehouses, as well as logistics, payment processing, medical devices and services, and selected plays on the US consumer in our longer-horizon portfolios.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Dow Jones Industrial Average Index — measures the stock performance of thirty leading blue-chip U.S. companies.

The Nasdaq Composite Index is a large market-cap-weighted index of more than 2,500 stocks, American depositary receipts (ADRs), and real estate investment trusts (REITs), among others.

The Purchasing Managers Index (PMI) is a measure of the prevailing direction of economic trends in manufacturing.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1430061