By Natalia Gurushina, Chief Economist, Emerging Markets Fixed Income Strategy, VanEck Global

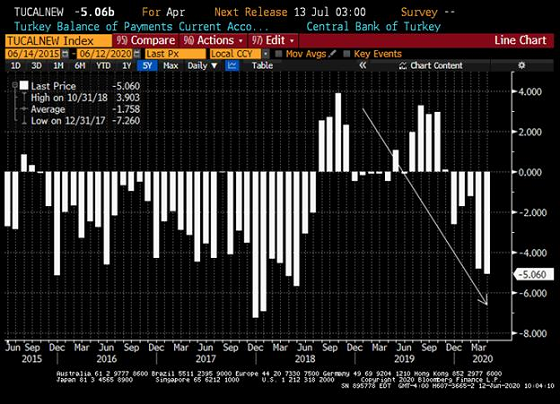

Turkey’s current account deficit widened further in April, adding to concerns about the country’s policy mix. The COVID crisis upended external accounts in many countries, but Turkey’s deterioration looks like an established trend. The 2018/early-2019 improvement had now been mostly reversed (see chart below), and many commentators blame the central bank’s policy of low interest rates (=a boost to domestic demand), currency interventions (=artificially strong exchange rate), and the state-sponsored credit surge. These concerns are reflected in the consensus forecast, which now expects the current account deficit to widen to 2.4% of GDP in 2021 and reach nearly 3% of GDP in 2022. Given that Turkey’s fiscal gap is also expected to widen, the country financing requirements might remain in high single digits (as a percentage of GDP) in the foreseeable future.

The latest buzz on Argentina’s debt restructuring front is that today’s deadline will be extended by another 7-10 days. We think this is a good sign, indicating that the sides are working to reach a compromise. We are also hearing from the local media that the government’s offer will be improved in a meaningful way. We hope this is true, as Economy Minister Martín Guzman reportedly said that this will be the final deal.

LATAM is at the center of the COVID epidemic right now and some governments are eyeing private pension funds to ease the economic pain. Mexico’s President Lopez Obrador reiterated that the country’s pension system should be changed. In comparison, Colombia’s proposal looks more timid – the government is considering withdrawals from pension accounts as part of the anti-COVID response package. This sounds similar to Peru’s initiative a few months back, under which individuals could withdraw up to 25% of their pension deposits.

Chart at a Glance: Turkey’s Current Account Deficit Widened Further in April

Source: Bloomberg LP

IMPORTANT DEFINITIONS & DISCLOSURES

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments.; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan’s index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG – JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.