My colleague Russ Koesterich recently made the case for emerging market (EM) bonds in today’s investment portfolio, stating that several factors make this asset class more attractive than it was just five years ago.

Competitive yields, improving fundamentals and cheap currencies have helped to make this a more attractive investment. But perhaps the biggest story in emerging market debt has been an improvement in credit quality – both in an absolute sense and, perhaps more interestingly, relative to bonds from developed markets.

This last point comes as a surprise to most investors. When you picture bonds from emerging economies, visions of defaults and currency devaluations are likely dancing in your head. [Emerging Market Bond ETFs for Yield]

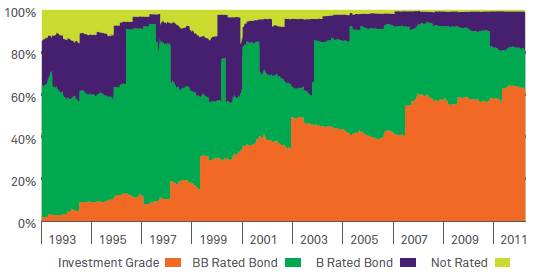

What you may not know is that the credit quality of this asset class has steadily improved over the past twenty years. Many EM debt issuers have learned lessons from the past and as a result, have developed sound fiscal policies which have resulted in more stable economies and, in many cases, investment grade credit ratings (see below). Today over 60% of the emerging market bond universe is rated BBB or above.

Emerging market bonds: Global market capitalization by credit buckets[1]

{kind=link}

So what’s causing this improvement in credit risk among emerging market issuers? There are four key drivers:

1. Better fiscal management. In other words, living within one’s means. For bond issuers this means raising revenue and reducing spending. According to data from the latest IMF World Economic Outlook, emerging economies’ fiscal revenues as a percentage of GDP increased from the high-teens in the 1980s to slightly above 30% today.

2. Stronger balance sheets. It may surprise you to know that compared to the developed markets, emerging markets have been deleveraging. Prior to the financial crisis, the average level of developed market gross government debt as a percentage of GDP was 74%; today, it stands at 110% – a number that, if not quickly reversed, could lead to a secular slowdown in growth. In contrast, EM countries were already repairing balance sheets heading into the financial crisis and have maintained stable debt-to-GDP levels since then (see below)[2].