While large cap energy names have also struggled, small cap energy names as a group are down nearly 20% since mid-December, over 10% worse than large cap Energy. (It can be noted the small cap energy sector is technically in a bear market, as it has drawn down over 20% since its peak on 1/4/2017).

Taking a slightly longer-term view, small caps significantly outperformed large caps during the Trump Bump and still have a performance edge on large caps since the election. Therefore, this more recent underperformance could just be a bit of market consolidation as we wait for more news to come out of Washington regarding regulations and spending.

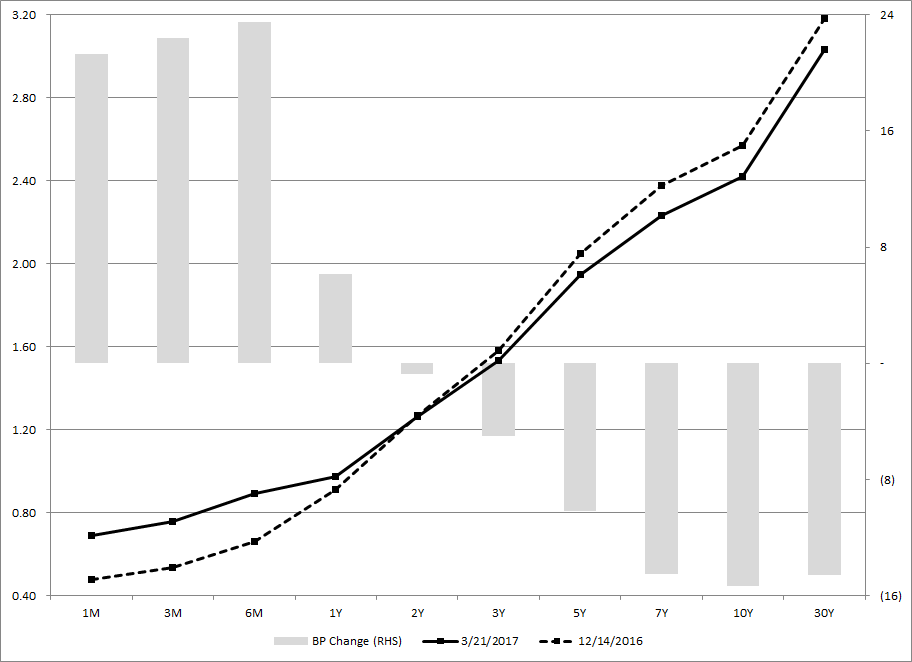

Switching gears slightly to look at how rates have performed over the same period, it is a bit of a tale of two halves (of the curve).

The curve has flattened significantly, as the very shortest end (T-bills) has spiked nearly 20bp on the Federal Reserve raising rates (most of this spike came at the end of February/beginning of March). Conversely, longer dated treasuries have traded nearly 15bp lower since December 14, which coincided with the post-election rate top.

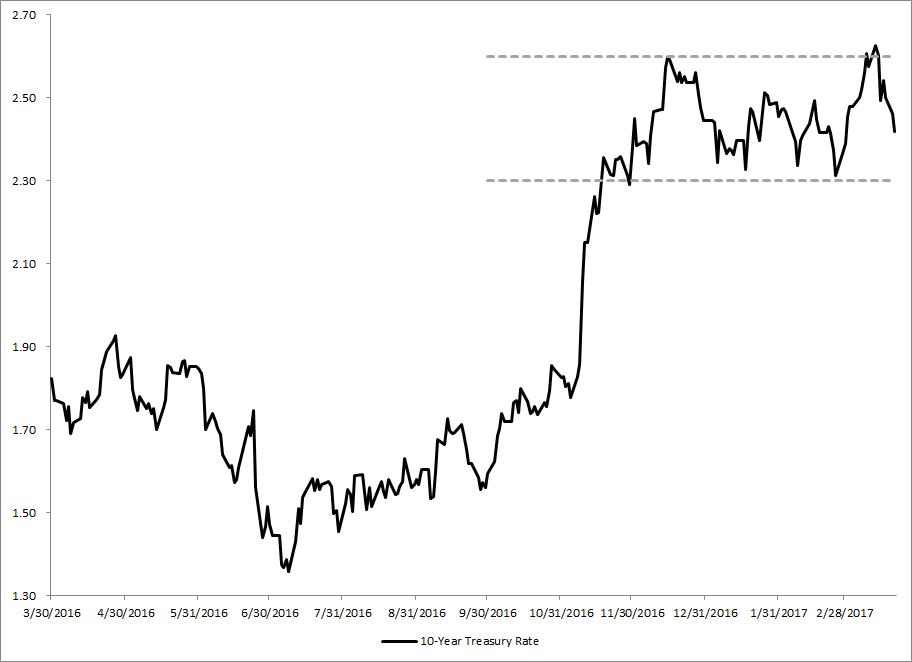

So while rates are lower, they definitely still appear to be rangebound, with the 10-year trading in an approximately 30bp range from 2.3% to 2.6% (of which it is almost in the middle of currently). So interest rates generally seem to be following in the similar complacency trade as equities.

Taking a quick snapshot of other asset class performance since 12/14/16 leaves a bit of a mixed signal as well:

- Gold: +6.83%

- US Dollar: -2.07%

- EAFE (Local): +5.31%

- Emerging Markets (Local): +8.59%

So while international markets have performed admirably (even without the currency effect), which could be a pro-speculation trade, Gold has also ripped higher, which could be a pro-flight to quality trade. Throw in declining and/or continued low levels of volatility in equities, rates, and gold, (and the increasing volatility coming out of Washington!) and it can be a bit of a complicated task predicting what markets will do from here. Therefore, while the complacency trade may be over, we will just have to wait and see on what comes next.

Clayton Fresk is a Portfolio Manager at Stadion Money Management, a participant in the ETF Strategist Channel.

Disclosure Information

Past performance is no guarantee of future results. Investments are subject to risk and any investment strategy may lose money. The investment strategies presented are not appropriate for every investor and financial advisors should review the terms and conditions and risks involved. Some information contained herein was prepared by or obtained from sources that Stadion believes to be reliable. There is no assurance that any of the target prices or other forward-looking statements mentioned will be attained. Any market prices are only indications of market values and are subject to change. Any references to specific securities or market indexes are for informational purposes only. They are not intended as specific investment advice and should not be relied on for making investment decisions. The S&P 500 Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The S&P Small Cap 600 Index, more commonly known as the S&P 600, is a stock market index from Standard & Poor’s that covers roughly the small-cap range of U.S. stocks, using a capitalization-weighted index. The index covers approximately three percent of the total U.S. stock market. The MSCI EAFE (Europe, Australasia, and Far East) Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. The Global Industry Classification Standard (GICS) is a financial industry taxonomy, or classification, system and is used to create industry, or sector, classifications. One cannot invest directly in indexes, which are unmanaged and do not incur fees or charges. Founded in 1993, Stadion Money Management is a privately owned money management firm based near Athens, Georgia. Via its unique approach and suite of nontraditional strategies with a defensive bias, Stadion seeks to help investors—through advisors or retirement plans—protect and grow their “serious money.” Contact Stadion at 800-222-7636 or www.stadionmoney.com. SMM-032017-315