The bulk of our fixed income holdings are held in high yield bonds and preferred stock. This increases our portfolio’s yield and gives us exposure to cyclical assets which have benefitted following the US election. In addition, it gives us significant exposure to US corporate credit spreads, which should tighten as a result of

stimulative economic policy. We also continue to hold a position in US dollar denominated emerging markets bonds.

This helps diversify the portfolio while avoiding foreign currencies.

We have recently increased our position in long duration US Treasury bonds. While we continue to believe that interest rates, inflation, and inflation expectations are in a cyclical uptrend in the US, markets may have discounted too much too quickly. Investor positioning anticipating higher rates has become extreme, which makes markets vulnerable to disappointments in Trumps policy implementation. We have therefore sought to protect our portfolio, which is otherwise positioned to benefit from successful implementation of these

policies, against possible hiccups along the way.

{kind=link}

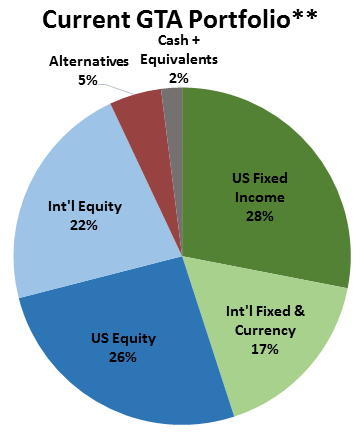

**Individual account allocations may differ slightly from model allocations.

*Some Emerging Markets allocation overlaps with regional allocations.

^Excluding GTA’s 52% fixed income, alternative, and cash positions.

Our equity portfolio favors cyclical over defensive sectors in order to benefit from the acceleration in economic growth likely upon implementation of President-elect Trump’s economic policy platform. In the US we favor financials, technology, biotech, defense, and small cap. Financial stocks have been hurt by persistently low interest rates and a flattening yield curve, and a reversal of that process will support them.

Additionally, we expect the regulatory environment to improve under a Trump presidency. US technology companies are the most innovative in the world and will continue to expand their scope into new industries, displacing many older companies and industries through the process of creative destruction.

Small caps are more US-centric than the broader US equity market. They tend to have much less foreign exposure, both in terms of production and sales, and therefore will benefit from Trump’s “US first” policy philosophy. Biotech stocks have underperformed in expectation of healthcare reform. They therefore represent good relative value and also potentially serve to protect the portfolio against underwhelming progress made towards reform in Washington. We have initiated a position in US defense stocks.

US allies are reconsidering their dependence on the United States for military protection, and will therefore seek to build up their own defense in the coming years. We have trimmed our position in small caps in order to protect the portfolio against disappointment in progress made in Washington. Internationally, we hold positions in European, Japanese, Australian, and Mexican equities.

European equities, and particularly financials, offer strong relative value and should be supported as the political environment becomes clearer over the course of the year. Fiscal and monetary stimulus in Japan will continue to put downward pressure on the Yen, which will support the Japanese equity market. We have maintained our position in Australian equities which are also supported by pro-growth fiscal policy and a recovering commodity market.

Following a major selloff in Mexican equities as a result of Trump’s victory, they offer deep value and a cheap way to protect the portfolio against disappointment in reform implementation. We continue to hold a position in gold. Its status as an alternative currency should support it as global central banks continue to pursue extremely aggressive policies. Furthermore, as an asset with low correlations to most others, it helps lower overall portfolio volatility.

Global Tactical Income Positioning Our Global Tactical Income Portfolio uses the same global macro framework as our other three Global Tactical Portfolios, but due to its income and capital preservation investment goals, its holdings differ to some degree. It does not participate in some equity allocations, and owns some additional fixed income holdings.

Currently, GTI owns Treasury inflation-protected securities and Build America Bonds, in addition to the fixed income holdings common across all four portfolios. These holdings help reduce volatility, while increasing diversification and limiting concentration. Its equity exposure avoids Australia and Mexico in order to reduce volatility.

This article was written by the team at JAForlines, a participant in the ETF Trends Strategist Channel.