{kind=link}

By Rod Smyth, RiverFront Investment Group Chief Investment Strategist

We believe U.S. long-term interest rates may have hit a multi-year low, perhaps even an all-time low.

If we are correct then bond portfolios and the bond portion of balanced portfolios require scrutiny in our view.

This is a bold statement, so let’s examine some of the main structural reasons that caused US long-term interest rates to fall to such low levels and seek to explain why we believe three of the structural forces that drove rates down are changing.

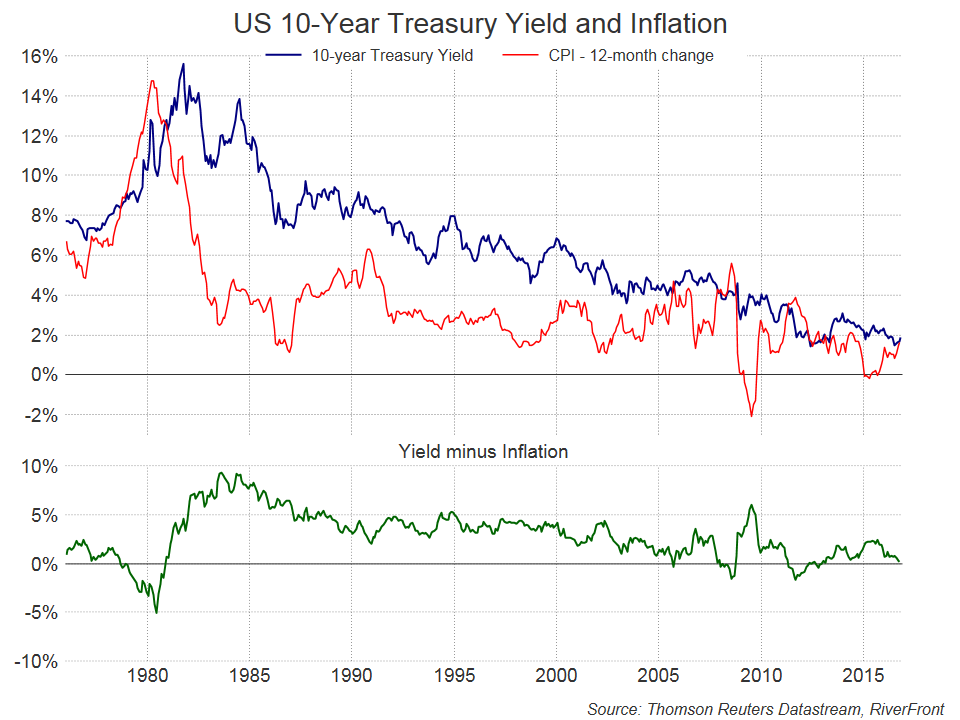

Paul Volker and the battle against inflation

US 10-year Treasury note yields peaked in September 1981 at just over 15% (see chart below). Paul Volker took over as chairman of The Federal Reserve in August 1979 as inflation headed for double digit growth rates. He made reducing inflation the number one priority, implemented a policy of pushing short-term interest rates well above the level of inflation, and accepted the resulting back to back recessions of the early 1980s as an acceptable price.

As inflation fell, so did interest rates, but the legacy of Paul Volker was that 10-year bond yields remained well above the inflation rate for twenty five years beginning in 1982 (see lower clip on the chart below.

During the 2000s investors became much less concerned about inflation and the current Federal Reserve regime could hardly be more different.

Since 2009, both the Bernanke and Yellen Fed have had their primary focus on achieving higher growth and preventing deflation (falling prices).

For much of the last five years 10-year Treasury yields have been close to the level of inflation. Bond investors have not demanded a premium over the prevailing inflation rate.This suggests to us that complacency about inflation is pervasive and that bond investors have little or no protection should inflation accelerate.

{kind=link}

Globalization and the labor “supply shock”

A series of events unfolded in the world economy during the last 25 years that profoundly changed the global labor market. For much of the post war period, the world’s most populace countries were closed economic systems, many embracing a communist economic model. Major economies such as India, the former Soviet Union and China all emerged from behind those closed economic systems during the 1990s and 2000s. Major free trade deals were negotiated, but perhaps the most significant single event was the admission of China into the World Trade Organization in 2001. This sudden and dramatic increase in the supply of global labor greatly reduced the negotiating power of workers in industries which compete in a global market; and, as many have argued, led to the election of President Trump. If the cost of globalization has been lost manufacturing jobs the benefit has been lower prices for all consumers, and thus persistently low levels of inflation as measured by goods prices. If the pendulum of US policy now swings away from free trade in order to protect US jobs, it follows that the risk is higher goods prices. As a result, we believe bond investors may once again require an ‘inflation premium’ i.e. 10-year rates that are above the prevailing inflation level.

The Great Recession

The recession that began in 2008 was much more than a business cycle recession, in our view; it was a balance sheet recession. Consumers and businesses had too much debt, much of it secured against assets that were overvalued and whose value was falling.

Recovery from such recessions has historically taken much longer and the risk of a deflationary depression is very real. Ben Bernanke and his colleagues decided radical monetary action was needed.

Short-term interest rates were cut to around zero and; in addition, the Fed chose to influence the level of long-term interest rates for the first time since the early 1950s.

Their program, which became known as “Quantitative easing” (QE), involved the Fed using its balance sheet to systematically purchase both Treasury and Mortgage bonds. Investors took their lead from the Fed and 10-year Treasury yields fell from around 4% to around 1.5% between 2010 and 2013 even as the economy recovered.

The Fed’s QE program ended in November 2014 and in December 2015 it raised short-term interest rates for the first time in the current expansion (by 0.25%). Despite this, the Federal Reserve has since been at pains to stress that the economy needed very low interest rates for long enough to ensure the expansion (now in its seventh year) wouldn’t falter.

During the last seven years, the unemployment rate has fallen from 10% to its current level of just 4.6% and the Fed has clearly signaled it is ready to raise short-term interest rates again (another 0.25% is widely expected).

How many more times the Fed raises rates in 2017 will likely depend on the extent of policy stimulus enacted by the Trump administration and Congress, but if President Trump comes anywhere close to achieving his goal of faster economic growth, or if his policies result in accelerating inflation (both of which we believe are directionally correct), then both short and long-term interest rates will rise.

As we examine the various scenarios that may unfold in 2017, we will seek to handicap how much rates may rise under different scenarios. That said, last week Chief Fixed Income Officer Tim Anderson clearly outlined how Riverfront is positioning its portfolios for the current environment.

His message was simple: “Our first line of defense in our balanced portfolios is to underweight bonds vs equities. We prefer bonds that act somewhat like stocks (high yield) and investment grade bonds over Treasuries. In our Moderate Growth and Income bond portfolio, we have lowered duration from 7.3 years to 4.1 years”. We believe we are ready to navigate a world of higher rates.

Rod Smyth is the Chief Investment Strategist at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

High yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In a rising interest rate environment, the value of fixed-income securities generally declines.

RiverFront Investment Group, LLC, is an investment advisor registered with the Securities Exchange Commission under the Investment Advisors Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.