“Were the FOMC to delay increases in the federal funds rate for too long, it could end up having to tighten policy relatively abruptly, to keep the economy from significantly overshooting both of the Committee’s longer-run policy goals.”

Translation: Yes, we know that if we wait too long we’ll get more inflation than we want. Relax everyone, we’ve got this.

“With the federal funds rate currently only somewhat below estimates of the neutral rate, the stance of monetary policy is likely moderately accommodative, which is appropriate to foster further progress toward the FOMC’s objectives. But because monetary policy is only moderately accommodative, the risk of falling behind the curve in the near future appears limited, and gradual increases in the federal funds rate will likely be sufficient to get to a neutral policy stance over the next few years.”

Translation: We aren’t all that stressed about the level of monetary support in the economy because we think the rate that would exist without our interference isn’t much higher. Since the difference isn’t that big, we don’t think that there is that big of a risk of excess inflation getting ahead of us in the near-term. Do the math Mr. Market, if the difference isn’t all that great and I’m saying we will get to neutral over the next few years, any hikes are going to be wee little ones.

We think this testimony actually reduces the likelihood of a rate hike in December. Chairwoman Yellen just laid out her case for why we shouldn’t get fussed if there is the Fed once again takes a pass on a rate hike.

Add in the slowing of the German economy, and the European Central Banks comments that lay the groundwork for additional stimulus, odds are the recent strength in the US dollar will persist and weigh on export demand.

In other words, currency headwinds are likely to remain without a December interest rate hike. Then there is the uncertainty surrounding President-elect Trump’s economic policies.

Keep in mind as well that Italy is holding a constitutional referendum on Sunday, Dec. 4.

- A vote for “yes” would do a lot to break Italy’s onerous political process, which seems to be utterly incapable of getting anything done in a nation that is in desperate need of reform.

- A “no” vote would solidify the status quo, which would likely lead to capital flight as the market does a face palm on the realization that Italy just isn’t going to get its house in order. Mamma mia!

Currently, polls are indicating that the vote will fail, which would put upward pressure on the dollar. We’re all pretty confident in the accuracy of those polls these days too, right?

They utterly nailed it on Brexit and President Trump — cut to all those face-palming pollsters. Sarcasm folks. Sarcasm!

As we see it, all of this increases the likelihood the Fed hits the pause button on interest rate hike timing until their March 2017 meeting.

As those items we cited above unfold and we get even more economic data ahead of the Fed’s next FOMC meeting on December 14-15, we’ll be on watch for what it all means the Fed is likely to do.

Turning our gaze to next week, which will be a short one due to the Thanksgiving holiday — one of our favorites, and it’s not because of all the pie.

Historically the Wednesday before Thanksgiving tends to be a big travel day for many, and AAA predicts that 49 million Americans will travel 50 miles or more during the upcoming Thanksgiving holiday, with 89% of them traveling by car. Just reading that we too wish the days of the autonomous driving vehicle that is part of our Disruptive Technology investing theme were here today so we could catch a post-pie snooze on the way home.

The shortened week means that Wednesday will be a rather quiet day in the markets, as will Friday, thereby making the busiest days of the week today and tomorrow. Indeed, Tuesday sees a hefty dose of economic data including the weekly MBA Mortgage Index and jobs reports as well as the October reports for Durable Orders and New Home Sales. Also on Tuesday we’ll get the next iteration of the Fed’s FOMC minutes, this time for the Nov. 2nd meeting. With the next FOMC meeting just a few weeks off and the markets once again split on what the Fed will do as it pertains to interest rates, odds are next week’s minutes release will be dissected, parsed and of course scrutinized.

While attention spans are likely to wane as the week goes on as our minds dream of sweet potato casserole while others plot how to get on the road and beat those 49 million travelers, we still have some corporate earnings reports being issued. Granted, roughly 95 percent of the S&P 500 has reported already, but there are still 13 of those 500 companies reporting this shortened week. It is what it is. Given the lightly staffed trading floors and rather low trading volume, Wednesday and the Friday after Thanksgiving are days that companies use to slip in not so good news. Their bet is people will be traveling and or shopping, and the news flies under the radar. Perhaps they need to be reminded about our Connected Society investing theme…

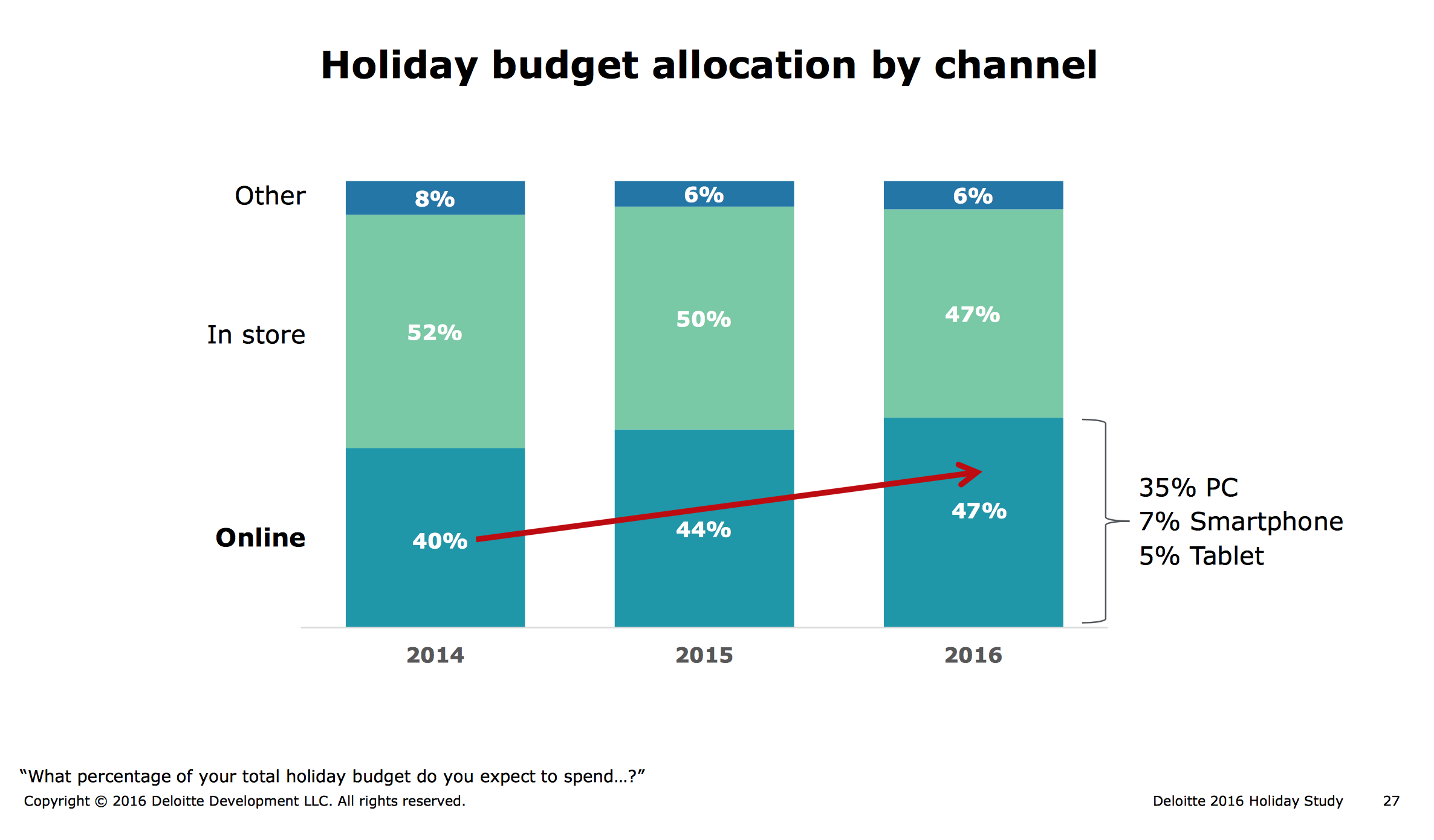

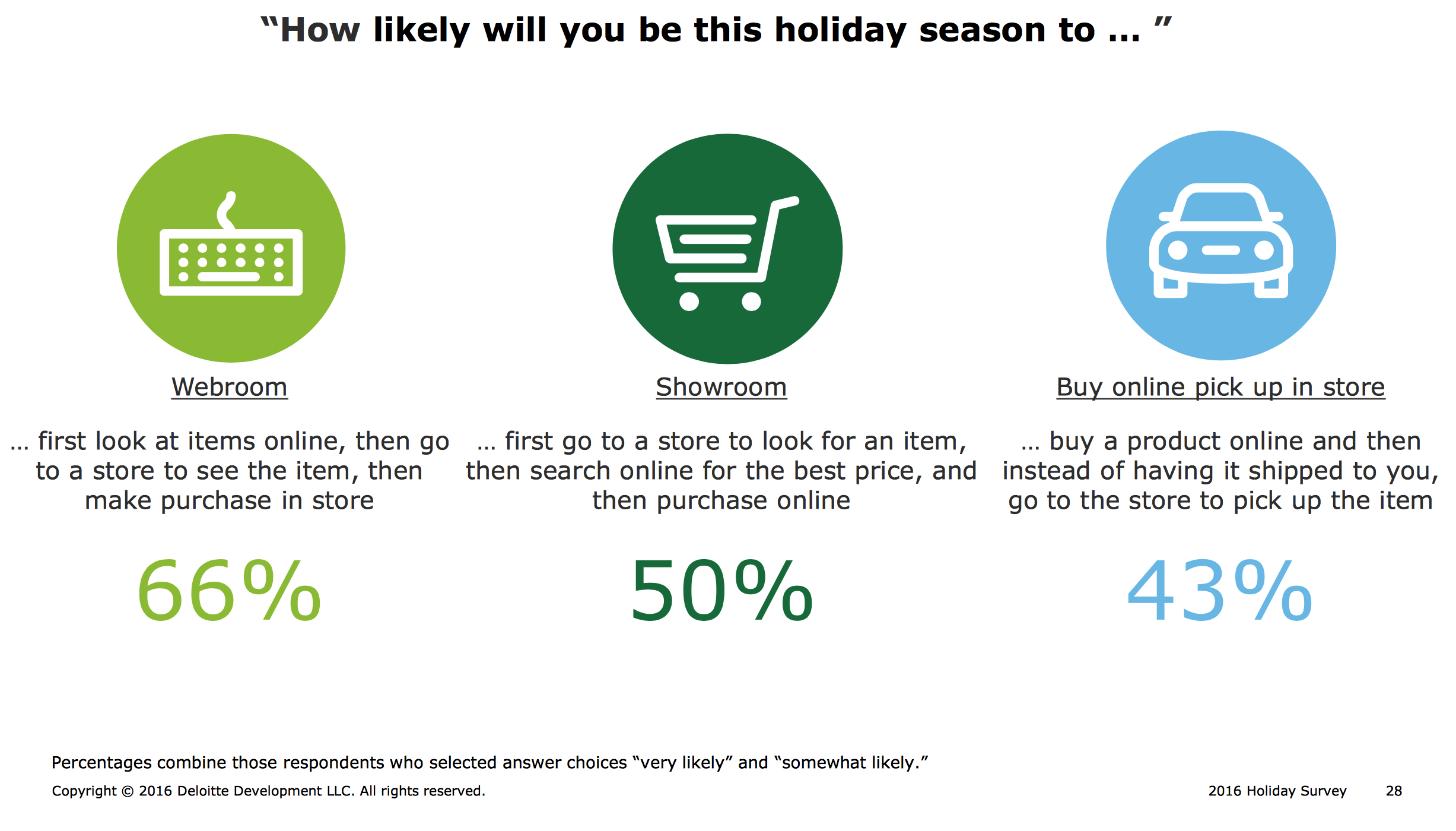

As we just indicated, many will be shopping the day after Thanksgiving, which is far better known to many as Black Friday, the official kickoff to the holiday shopping season. Historically consumers have flocked to retail stores to scoop up deals and help walk off all that Thanksgiving Day pie. This year, however, Deloitte sees digital shopping matching brick & mortar shopping for the first time and we confess we are very much in tune with this aspect of our Connected Society investing theme. Fight the crowds or relax with our feet up and pursue the latest online deals from Amazon (AMZN), William-Sonoma (WSM), Nike (NKE), Under Armour (UA), Moleskine (MLSKF) and dozens of others? It doesn’t seem like much of a choice if you were to ask us.

{kind=link}

Coming out of the holiday shopping weekend, we expect the National Retail Federation to offers its best guesstimate on how much consumers plopped down over the big shopping weekend. Odds are an even clearer picture will be had after Cyber Monday, a day that has become the online shopping equivalent of Black Friday. In our view, Black Friday to Cyber Monday will set the tone for 2016 holiday shopping, and as usual, there will be share gainers and losers as well as the food chain way to play it all.

Affordable Luxury

- Luxottica (LUX)

- Movado Group (MOV)

Aging of the Population

- Everyday Health (EVDY)

- Patterson Cos. (PDCO)

Cash-strapped Consumer

- Dillards Inc. (DDS)

- Burlington Stores (BURL)

- Campbell Soup (CPB)

- Dollar Tree (DLTR)

- DSW Inc. (DSW)

- Hormel Foods (HRL)

Connected Society

- Dycom Industries (DY)

Content is King

- Gamestop Corp. (GME)

Economic Acceleration/Deceleration

- Jacobs Engineering (JEC)

Fattening of the Population

- Jack in the Box (JACK)

- Hostess Brands (TWNK)

Rise & Fall of the Middle Class

- Tyson Foods (TSN)

- Citi Trends (CTRN)

- Signet Jewelers (SIG)

- Urban Outfitter (URBN)

Scarce Resources

- Canadian Solar (CSIQ)

About Author

Chris Versace’s thematic investing insights are the culmination of more than 20 years analyzing industries and companies in a variety of roles as an equity analyst, portfolio manager, investment banker and strategic consultant.

As the Chief Investment Officer of Tematica Research, Mr. Versace is editor in chief of Tematica Investing and Tematica Insights, as well as the author of the Monday Morning Kickoff, which has become a must-read publication for RIA’s and Money-Managers around the world, as well as many in the Financial Media. Mr. Versace is also the co-author of the book Cocktail Investing: Distilling Everyday Noise into Clear Investment Signals for Better Returns.