Our outlook for 2016 remains mildly bullish, as we are encouraged by the improved market technicals and renewed credit market confidence. We remain more optimistic about international markets, which have undergone a full blown bear market since 2014.

Now, however, the market bottom on February 11th looked to have been capitulative among international equities. International equity valuations are compelling, and international equities, particularly emerging markets (which are attractively valued on a relative basis) are beginning to display relative strength.

While the 2016 elections will probably lead to some short-term volatility, we believe that the most likely market direction after the election will be upwards as uncertainty will finally be resolved.

High Dividend Equity

One of the biggest contributors to market performance this year continues to be historically low interest rates. The result has been positioning across fixed income markets and equity sectors in an effort to benefit from the current environment.

In the first half of 2016, the “bond proxy” sectors such as Telecom and Utilities dramatically outperformed the S&P 500 Index until the 10 year Treasury hit a low of 1.36% in July. Since the July 8th low, the subsequent rise in yields combined with Federal Reserve comments about a possible December rate hike propelled investors out of bond proxy sectors into more growth-oriented sectors such as Technology.

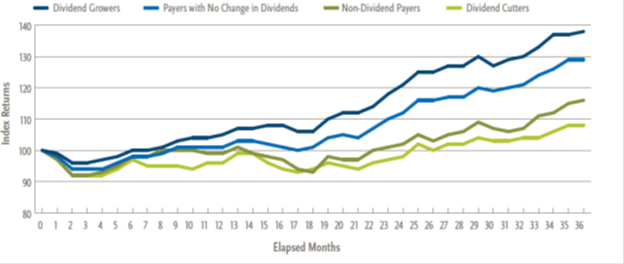

Historically “dividend growth” companies demonstrating earnings growth, strong free cash flow and rising dividends are resilient in a rising interest rate scenario.

Numerous studies point to the last eight Fed fund hikes where “dividend growers” experience strong performance compared to dividend non-payers, cutters and companies that don’t consistently increase their dividend.

{kind=link}

The U.S. bull market continues to forge ahead looking beyond the negative S&P 500 earnings projection for this quarter of -1.1% which would be the sixth negative quarter in a row. In the fourth quarter, greater stability in the dollar and oil prices should help corporate earnings beat lowered expectations.

This quarter we noted a slower pace of several shareholder friendly policies such as share buybacks and dividend growth rates. Despite the shift away from share buybacks, the Materials, Industrials, Financials, Technology and Energy sectors are projected to accelerate their dividend growth along with stronger growth prospects with improving revenues.

Sean Clark is the Chief Investment Officer at Clark Capital Management, which is a participant in the ETF Strategist Channel

Disclosure Information

Past performance is not indicative of future results. This is not a recommendation to buy or sell a particular security. Please see attached disclosures.

The opinions expressed are those of the Clark Capital Management Group Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. There are no guarantee of the future performance of any Clark Capital Investments portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. For educational use only. This information is not intended to serve as investment advice. This material is not intended to be relied upon as a forecast or research. The Investment or strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Past performance does not guarantee future results.

The Dow Jones Industrial Average is a stock market index that shows how 30 large publicly owned companies based in the U.S. have traded during a standard trading session in the stock market.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performers of developed markets outside the U.S. and Canada.

The MSCI Emerging Markets Index is a freefloat-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

The Barclays U.S. Government and Credit Bond Index measures the performance of U.S. dollar denominated U.S. Treasuries, government-related, and investment grade U.S. corporate securities that have a remaining maturity of greater than 1 year. In addition, the securities have $250 million or more of outstanding face value, and must be fixed rate and non-convertible.

The Barclays U.S. Corporate High-Yield Index covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

The Dow Jones Aggressive Portfolio Index measures aggressive stocks, bonds, and cash which are represented by multiple subindexes and is quoted in U.S. dollars.

The Dow Jones Moderately Aggressive Portfolio Index measures moderately aggressive stocks, bonds, and cash which are represented by multiple subindexes and is quoted in U.S. dollars.

The Dow Jones Moderate Portfolio Index measures stocks with moderate risk, bonds, and cash which are represented by multiple subindexes and is quoted in U.S. dollars.

The Dow Jones Moderately Conservative Portfolio Index measures moderately conservative stocks, bonds, and cash which are represented by multiple subindexes and is quoted in U.S. dollars.

The Dow Jones Conservative Portfolio Index measures conservative stocks, bonds, and cash which are represented by multiple subindexes and is quoted in U.S. dollars.

MSCI World Index measures large and mid cap representation across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.

Morningstar is the largest independent research organization serving more than 5.2 million individual investors, 210,000 Financial Advisors, and 1,700 institutional clients around the world.

For each separate account with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a separate account’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of separate accounts in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. The Overall Morningstar Rating for a separate account is derived from a weighted average of the performance figures associated with its three-, five- and ten-year Morningstar Rating metrics.

The relative strength measure is based on historical information and should not be considered a guaranteed prediction of market activity. It is one of many indicators that may be used to analyze market data for investing purposes. The relative strength measure has certain limitations such as the calculation results being impacted by an extreme change in a security price.

© 2012 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. Not every client’s account will have these exact characteristics. The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment.

Clark Capital Management Group, Inc. reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security, sector or industry. There is no assurance that any securities, sectors or industries discussed herein will be included in an account’s portfolio. Asset allocation will vary and the samples shown may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices and which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options. This volatility is meant to be forward looking and is calculated from both calls and puts. The VIX is a widely used measure of market risk. The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities. The Barclays Capital U.S. Aggregate Bond Index is a market capitalization-weighted index, meaning the securities in the index are weighted according to the market size of each bond type. Most U.S. traded investment grade bonds are represented. Municipal bonds, and Treasury Inflation-Protected Securities are excluded, due to tax treatment issues. The index includes Treasury securities, Government agency bonds, Mortgage-backed bonds, Corporate bonds, and a small amount of foreign bonds traded in U.S. The Barclays Capital Aggregate Bond Index is an intermediate term index.

The volatility (beta) of a client’s portfolio may be greater or less than its respective benchmark. It is not possible to invest in these indices.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services and fees can be found in its Form ADV which is available upon request. CCM-676