A relatively calm month, August saw mixed results from second quarter corporate revenue and earnings announcements. Market expectations of a Fed interest rate hike increased. Nevertheless, U.S. equity markets continued the bull market rally and closed the month less than 1% from all-time highs.

KEY TAKEAWAYS

• United States equity markets remain strong, reaching all time highs on 08.15.16 and then closing the month, on average, 1% from those highs.

• U.S. Corporate results for Q2 2016 were mixed with actual earnings and actual revenues beating estimates; however actual and estimated earnings growth continues to decline.

• Moving forward we expect asset price volatility during the month

PERFORMANCE

U.S. equity markets continued the trend of positive performance with support coming from multiple expansion instead of earnings growth. During August 2016, the Dow Jones Industrial Average, the S&P 500, and the Russell 3000 returned 0.26%, 0.14%, and 0.26% respectively.

As of 08.31.16 the S&P 500 trades at a 16.9x forward 12-month P/E ratio, a ratio that has been steadily growing since the end of Q3 2015.

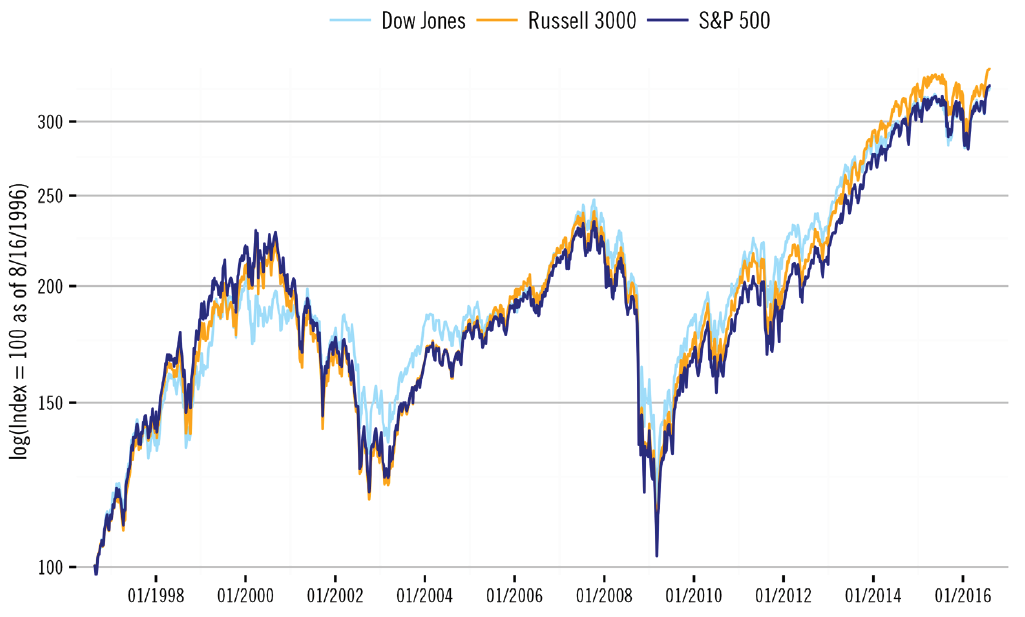

Figure 1 normalizes the S&P 500, Russell 3000, and Dow Jones to a value of 100 as of twenty years ago, and shows the magnitude of recovery that the prevailing bull market has regained since the most recent lows in 2008. The positive trend in U.S. equity markets has coincided with supportive monetary policy. As the market transitions into a month with three major central bank meetings, we expect an increased focused on the effect of monetary policy.

Figure 1 – INDEXED PERFORMANCE OF MAJOR U.S. EQUITY MARKETS OVER TWENTY YEARS

{kind=link}

Monthly price return data from 08.16.1996 to 08.16.2016 SOURCE: Innealta Capital using data from FactSet Research Systems Inc.

ASSET COMPARISON

A comparison of major asset class levels shows that equities, credit, and fixed income sovereign currently trade above their respective 5-year average, while commodities trade below their average levels. Figure 2 displays a comparison of different asset classes by normalizing the current values using Z-scores generated from 5 years of each markets’ history.

The immediate observation is the divergence inforeign exchange relative to the U.S. dollar. At the top of the diagram, we see that the U.S. Dollar is able to buy significantly more GBR Pounds in comparison to the average level over the last 5 years. U.S. Dollar strength relative to the GBR pound is a recent phenomenon following the results of the “Brexit” referendum in late June. The data also highlights the flattening of the U.S. Treasury 2 – 30-year yield curve. The 30-year yield is below while the 2-year yield is above the 5-year average, suggesting an upward yield shift on the short end of the curve and a downward yield shift on the long end of the curve. Despite a recent rally, Gold, Natural Gas, and Oil markets still remain below their respective 5 year average.

Figure 2 – NORMALIZED CURRENT ASSET LEVEL, OVER A 5-YEAR LOOK-BACK PERIOD

{kind=link}

Weekly price and yield data from 09.02.2011 to 08.26.2016 SOURCE: Innealta Capital using data from FactSet Research Systems Inc.

EARNINGS EXPECTATIONS

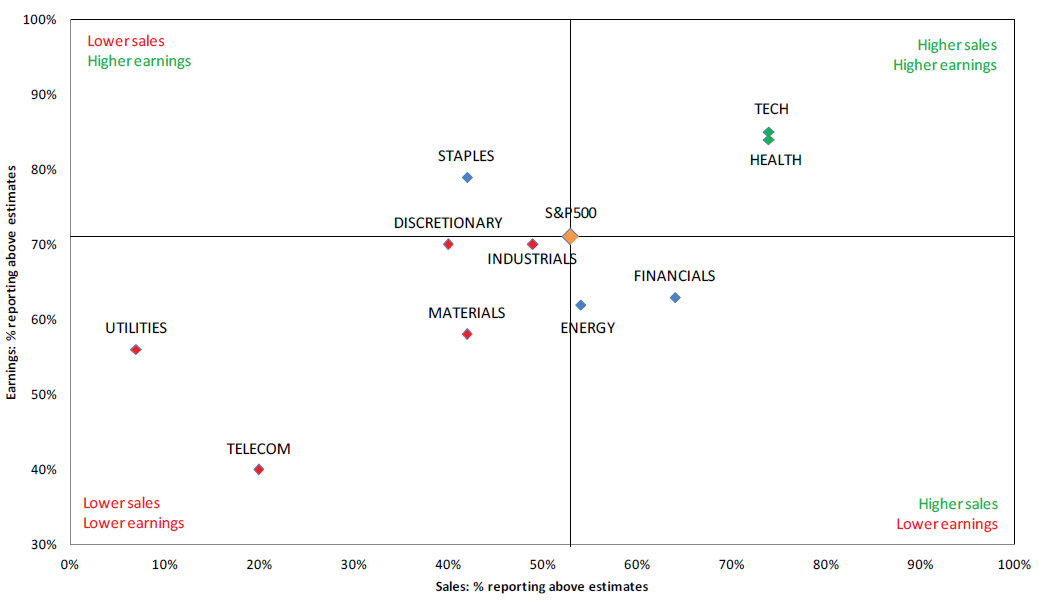

Corporate results from Q2 2016 showed that revenue and earnings beat estimates; however market expectations of future earnings growth remains weak. As of 08.26.2016, 98% of S&P 500 constituents have reported earnings for Q2 2016. 71% of those firms reported earnings that beat the mean estimate and 53% reported sales above the mean estimate. Looking ahead to Q3, 77 S&P 500 firms have already issued negative EPS guidance and 33 S&P 500 firms have issued positive EPS guidance.

Figure 3 shows a S&P 500 Sector Expectations Scorecard for Q2 2016. In this plot, the individual sectors of the S&P 500 are compared against their composite index on the basis of earnings and sales expectations. The largest number of positive earnings and sales surprises came from Tech and Healthcare sector firms, while sales and earnings results in Utilities and Telecom fell short of expectations.

Figure 3 – S&P 500 Q2 2016 EXPECTATIONS SCORECARD

{kind=link}

Data as of 08.26.2016 SOURCE: Innealta Capital using data from FactSet Research Systems Inc.

EARNINGS GROWTH

Despite the positive news of corporate results relative to expectations, actual and expected earnings growth remains a concern. For the second quarter, the year-over-year earnings decline for the S&P 500 is -3.2%, though the estimated earnings decline for the quarter was -5.5%.

In fact, Q2 2016 marks the first time since The Great Recession of 2008 that the S&P 500 has posted five consecutive quarters of year-over-year declines in earnings (Q3 2008 through Q3 2009).

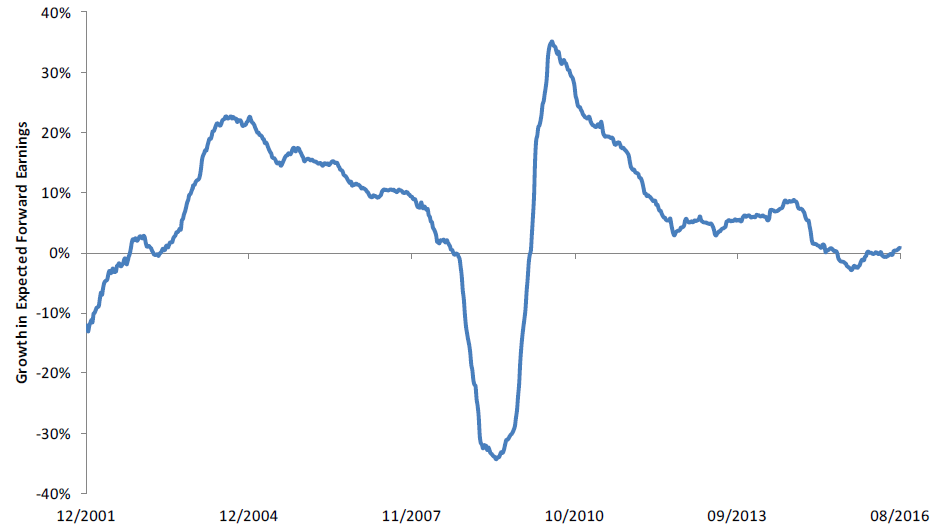

Forward 12-month EPS has fluctuated around $125.00 for 2 years, the most recent estimate is $128.77. However, as evidenced by Figure 4, growth in forward earnings expectations has fallen off significantly since Q4 2010, and currently stands at 0.9%.

Figure 4 – ROLLING FORWARD 12-MONTH EXPECTED EARNINGS YEAR-OVER YEAR CHANGE (%)

{kind=link}

Weekly price and EPS data from 12.28.2000 to 08.26.2016 SOURCE: Innealta Capital using data from FactSet Research Systems Inc.

LOOKING FORWARD

Monetary policy has been a key driver for asset performance over the past several years, and with three major central banks holding meetings we expect September to be an exciting month, especially after the Fed’s lackluster rhetoric from Jackson Hole.

During her speech, Fed Chairperson Janet Yellen said that she sees a stronger case for increasing the Fed Funds Effective Rate (FFER) in the near future. We must exercise patience to see whether or not this will come to fruition. The last increase in the FFER came in December of 2015, at which time the market forecasted four more increases in 2016. We are still waiting for the first increase in 2016. The implied probability from the Federal Funds Futures market of a 25 basis point interest rate hike in September increased from 19.2% to 35.7% during the month of August.

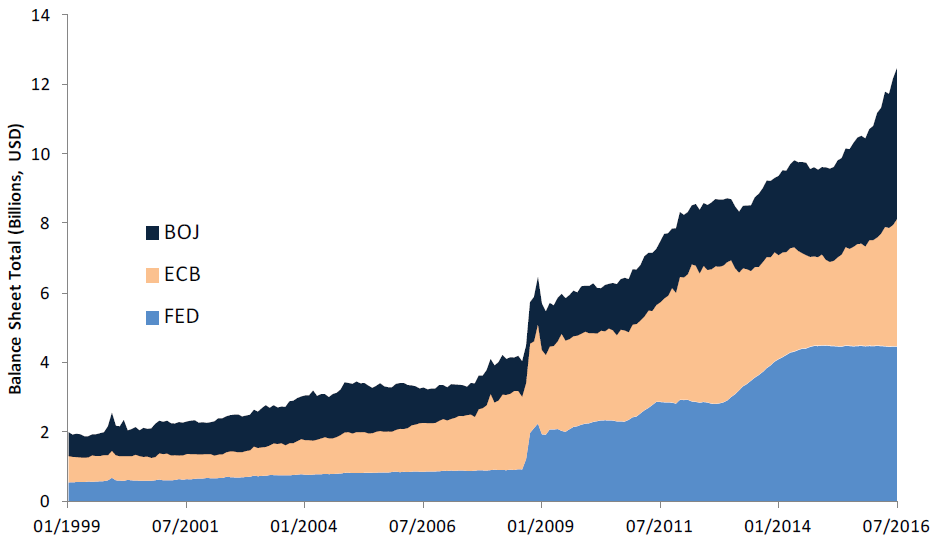

Additionally, the implied probability of 25 basis point rate hike through December rose from 31.5% to 45%.The September meetings of the Federal Open Market Committee, the Bank of Japan, and the European Central Bank will impact monetary policy expectations for the remainder of 2016. Collectively central bank balance sheets, as shown in Figure 5, continue to expand. Without earnings growth, and equity investors relying on multiple expansion, any change to monetary policy could have significant impact.

Figure 5 – CENTRAL BANK BALANCE SHEETS

{kind=link}

SUMMARY

August was a fairly quiet month, though possibly the calm before the storm of September’s central bank policy meetings. A large percentage of S&P 500 firms beat earnings estimates, yet mixed signals from declining earnings growth creates apprehension as the equity market has reached all-time highs. Heading into September we expect the market to focus on the scope and effect of monetary policy.

This article was written by Innealta Capital, a participant in the ETF Strategist Channel.

[related_stories]IMPORTANT INFORMATION

1. Data from FactSet Research Systems Inc., 8.26.2016

The information provided comes from independent sources believed reliable, but accuracy is not guaranteed and has not been independently verified. The security information, portfolio management and tactical decision process are opinions of Innealta Capital (Innealta), a division of AFAM Capital, Inc. and the performance results of such recommendations are subject to risks and uncertainties. For more information about AFAM Capital, Inc. please visit afamcapital.com. Past performance is not a guarantee of future results. Any investment is subject to risk. Exchange traded funds (ETFs) are subject to risks similar to those of stocks, such as market risk, and investors that have their funds invested in accordance with the portfolios may experience losses. Additionally, fixed income (bond) ETFs are subject to interest rate risk which is the risk that debt securities in a portfolio will decline in value because of increases in market interest rates. The value of an investment and the return on invested capital will fluctuate over time and, when sold or redeemed, may be worth less than its original cost. This material is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a solicitation or an offer, or a recommendation, to buy a security. Investors should consult with an investment advisor to determine the appropriate investment vehicle. Investment decisions should be made based on the investor’s specific financial needs and objectives, goals, time horizon and risk tolerance. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice.

The Russell 3000 Index measures the performance of 3,000 publicly held US companies based on total market capitalization, which represents approximately 98% of the investable US equity market.

The S&P 500 Index (Large Cap Equity) measures the performance of the large capitalization sector of the U.S. equity market and is considered one of the best representations of the domestic economy.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ.

Pounds per USD denotes the amount of GBPs that 1 USD can buy. The iBoxx USD Liquid Investment Grade Index is an index composed of U.S. dollar-denominated, investment-grade corporate bonds. The Dow Jones U.S. Select REIT Index intends to measure the performance of publicly traded REITs and REIT-like securities. US Benchmark Bond 2 year refers to the FactSet total return index of owning 2-year U.S. Treasuries. The iBoxx USD Liquid High Yield Index is an index composed of U.S. dollar-denominated, investment-grade corporate bonds. The MSCI AC Asia ex Japan Index captures large and mid cap representation across 2 of 3 Developed Markets countries (excluding Japan) and 8 Emerging Markets countries in Asia. U.S. benchmark bond 30 year refers to the FactSet total return index of owning 30 year U.S. treasuries. US benchmark bond 10 year refers to the FactSet total return index of owning 10 year U.S. treasuries. US benchmark bond 5 year refers to the FactSet total return index of owning 5 year U.S. treasuries. Yen per USD denotes the amount of Japanese yen that 1 U.S. dollar can purchase. NZ$ per USD denotes the amount of New Zealand dollars that 1 U.S. dollar can purchase. Eurostoxx 50 market capitalization weighted index of the leading 50 stocks covering Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal and Spain. Japan Nikkei 225 price weighted index of the 225 top-rated companies listed in the First Section of the Toyko Stock Exchange. Francs per USD denotes the amount of Swiss Francs that 1 U.S. dollar can purchase. Aussie$ per USD denotes the amount of Australian Dollars that 1 U.S. dollar can purchase. Euros per USD denotes the amount of Euros that 1 U.S. dollar can purchase. Loonie per USD denotes the amount of Canadian Dollars that 1 U.S. dollar can purchase. The MSCI ACWI ex. U.S. Index is a market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets excluding the United States.

Z-score communicates where a numerical value (in this case, current price) is in relation to where it has been over a stated and measurable period.

Registration of an investment adviser does not imply any certain level of skill or training.

AFAM Capital, Inc. is an Investment Adviser, registered with the Securities & Exchange Commission and notice filed in the State of California and various other states. For more information, please visit afamcapital.com. Registration as an investment advisor does not imply any certain level of skill or training. Innealta is an asset manager specializing in the active management of portfolios of ETFs. Contact your financial advisor for additional information. 301-AFAM-9/6/2016