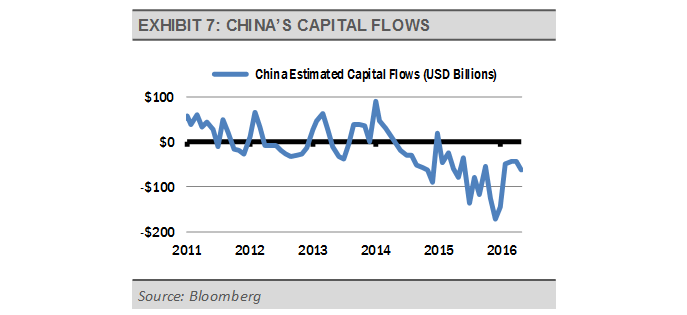

The sharp decline in emerging market capital flows since 2010 has been a significant challenge for these countries and has hampered the domestic growth prospects in many of the emerging economies. Net capital outflows accelerated through 2015 as it became evident the U.S. Federal Reserve (the Fed) would raise rates. We believe, with the recent Brexit vote and other concerns, the Fed will be on pause or at a minimum will not get far with any further rate hikes.

This scenario plays out well for emerging market countries and corporations, as it leads to stronger fundamentals. It also increases the probability of a slowdown in capital outflows for the time being and supports net capital flows for countries such as China (exhibit 7). This is evident in a recent report by The Institute of International Finance, which suggests outflows are expected to taper and there has been a pick-up in inflows, which would be positive for emerging market growth prospects.

{kind=link}

NARROWING RISK SPREADS

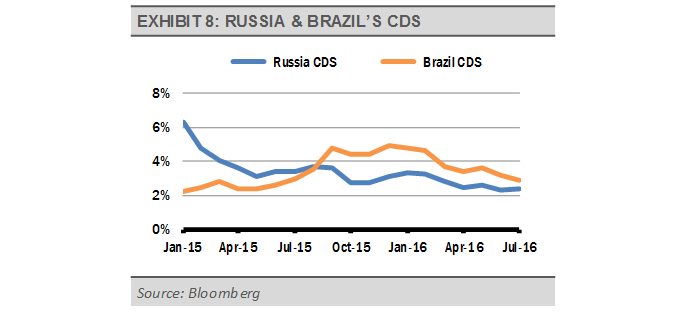

We also see more credit market confidence in emerging market economies in the form of credit default swaps. In recent months, emerging market credit default swaps, which reflect how much investors are willing to pay for insurance against bond defaults, have declined in countries like Brazil and Russia (exhibit 8). This decline in the cost of insurance reflects greater institutional investor confidence in these economies, which increases our confidence.

EMERGING MARKETS ETF OPTIONS

With our increasing confidence in the emerging markets, we think investors with high risk tolerances should consider adding emerging markets exposure through one of the many broad emerging market ETF offerings. We usually do not favor investing in individual emerging market countries, as increased risks resulting from a loss of diversification and increased concentration in more volatile, less liquid markets, outweighs any potential excess return, in our view.