By Rusty Vanneman, CFA and Josh Jenkins, CFA

At the mid-year checkpoint, income-oriented ETF portfolios are ripping it up. With a tailwind of lower interest rates and tighter credit spreads, most income-oriented asset classes have handily outperformed the broad market indices.

The risk for many investors now is the desire to chase recent returns. Chasing performance is never a healthy investment strategy. With that in mind, which investors are best suited for high-income strategies? Do they understand the risks involved? When do income strategies perform best? When do they perform worst? How should income strategies be benchmarked? Lastly, what’s our outlook?

Who Are Income Strategies Best Suited For?

Shifting demographic trends in the U.S. have created an opportunity for the investment industry. Based on the most recent census data, nearly 40% of Americans are in, or will soon enter, the distribution phases of their investment careers. This development will require adaptation by investment managers as investor goals shift. Young investors enter the workforce and progress through their careers with a typical focus on accumulation, building the wealth that will one day carry them through retirement. As retirement approaches, investor goals typically transition from accumulation to distribution. Here, the focus shifts to generating an income stream to sustain life after retirement. The investment industry will be forced to pivot in order to satisfy increasing demand from income-focused investors.

Recent Performance

There are some income strategies already available in the marketplace today, and their performance so far this year has been impressive. The typical multi-asset income portfolio is up 5% to 9% through the end of the second quarter, while many globally diversified, balanced portfolios are only up half as much.

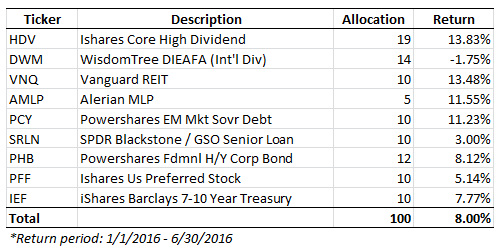

For example, here’s a representative income portfolio that targets a net yield of 3%+ and its year-to-date performance through June 30:

{kind=link}

Several market developments have contributed to this strong relative performance. Interest rates have fallen substantially, providing a strong tailwind to interest-rate-sensitive assets. Brexit fears have fostered the belief that central banks globally will keep benchmark interest rates lower longer, a positive for emerging market assets. Finally, the recovery of oil prices has led to a resurgence in high-yield bonds. Many asset classes affected by these developments, including those above, are staples within many income portfolios.

Beware of Risks

Investors generally associate income strategies with lower overall risk. Depending on the nature of the specific strategy, however, this assumption can prove to be unfounded. For example, income strategies are sensitive to movements in interest rates. After all, if Treasury bonds provided sufficient yield, investors would have little need to take any risk in their portfolios. They could simply own and mature a portfolio of risk-free Treasury bonds. Unfortunately, Treasury bonds don’t provide a sufficient yield. In fact, what they offer is far from it (the 10-year Treasury yield hit an all-time low recently). A consequence of these low yields is a push from investors into higher-risk assets to satisfy their income needs.

The typical income strategy diversifies across asset classes. It provides exposure to traditional dividend-oriented stocks and investment-grade bonds, as well as some non-traditional asset classes, including: high-yield bonds, emerging market bonds, real estate investment trusts (REITs), preferred stocks, and master limited partnerships. These portfolios certainly provide exposure to risky assets.