By Gary Stringer, Kim Escue and Chad Keller

The global equity markets have rallied on market confidence after the Brexit shock, as have equity-related investments, such as high yield bonds.

With the U.S. Federal Reserve (the Fed) apparently on hold for now, we think that the global economy can continue to grow, however, at a sluggish pace. This should lead to slow revenue growth and an end to the S&P 500 Index earnings recession in the quarters ahead. Equities can continue to rise along with revenues and earnings, though some areas face more headwinds than others from stretched valuations.

While we think global equity markets can continue to rise from here, we expect more bumps along the road, and are ready to take advantage of the opportunities for investment that these selloffs provide. For example, the Brexit vote and resulting asset price decline signaled a buying opportunity for us. As a result, we quickly moved back into emerging markets and increased our allocations to U.S. midcap value.

SEE MORE: Finding Investing Opportunities In Volatile Times

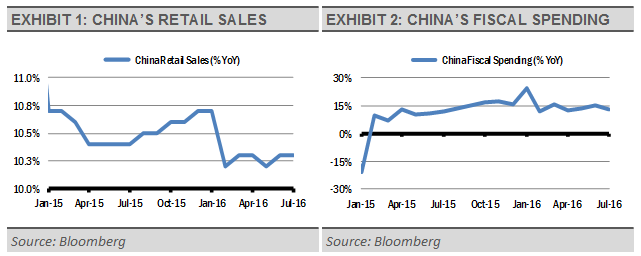

At these current elevated levels, markets are vulnerable to bad news, but our signals suggest that these spasms will be temporary. Economic growth prospects are not great, but may be better than investors expect. For example, growing consumer spending (+10.3% year-over-year) and fiscal stimulus (+13%) in China can translate to better growth than investors currently expect.

{kind=link}

Market-based inflationary expectations suggest a lack in inflationary pressure. Furthermore, monthly jobs creation will likely remain constructive, but in a slowing growth trend. The June and July jobs reports were strong, but the 6-month average jobs growth rate, which smooths out volatility in the monthly jobs growth numbers, is tracking at a decent pace, but well below the cycle highs seen in late 2014 and early 2015.

SEE MORE: Making the Case for Emerging Markets

Acting together, these forces should keep the Fed on hold, while allowing the global economy to continue its sluggish growth pace. We think that the percent change in economic growth will be range bound, not breaking out in one direction or the other. Thus, corporate sales revenue can grow slowly, potentially catching up to nominal GDP. Investors can take advantage of this environment through careful investment selection.

{kind=link}

The global financial markets have been “risk-on” since the Brexit vote, and our strategies have benefited. However, given our subdued view of potential economic growth, we think that risk management should still be our primary focus. Within that context, we are ready to take advantage of market volatility by making additional investments in areas that we think represent attractive valuation opportunities.

[related_stories]DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management LLC and has not been verified or audited by an independent accountant.