By Gary Stringer, Kim Escue and Chad Keller

The global equity markets have rallied on market confidence after the Brexit shock, as have equity-related investments, such as high yield bonds.

With the U.S. Federal Reserve (the Fed) apparently on hold for now, we think that the global economy can continue to grow, however, at a sluggish pace. This should lead to slow revenue growth and an end to the S&P 500 Index earnings recession in the quarters ahead. Equities can continue to rise along with revenues and earnings, though some areas face more headwinds than others from stretched valuations.

While we think global equity markets can continue to rise from here, we expect more bumps along the road, and are ready to take advantage of the opportunities for investment that these selloffs provide. For example, the Brexit vote and resulting asset price decline signaled a buying opportunity for us. As a result, we quickly moved back into emerging markets and increased our allocations to U.S. midcap value.

SEE MORE: Finding Investing Opportunities In Volatile Times

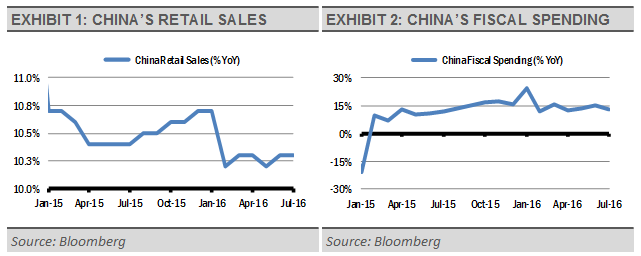

At these current elevated levels, markets are vulnerable to bad news, but our signals suggest that these spasms will be temporary. Economic growth prospects are not great, but may be better than investors expect. For example, growing consumer spending (+10.3% year-over-year) and fiscal stimulus (+13%) in China can translate to better growth than investors currently expect.

{kind=link}

Market-based inflationary expectations suggest a lack in inflationary pressure. Furthermore, monthly jobs creation will likely remain constructive, but in a slowing growth trend. The June and July jobs reports were strong, but the 6-month average jobs growth rate, which smooths out volatility in the monthly jobs growth numbers, is tracking at a decent pace, but well below the cycle highs seen in late 2014 and early 2015.