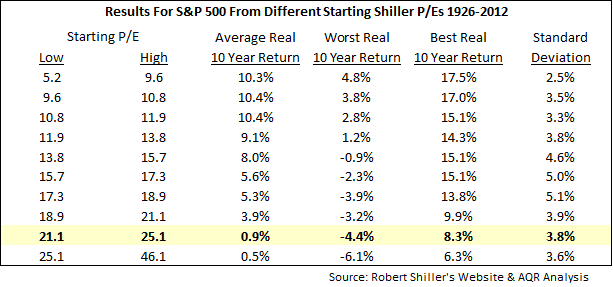

The Shiller P/E looks at earnings over a 10-year period rather than the current or trailing year’s earnings.), we can see that future returns are very likely to trail historical norms. Although investors aren’t necessarily fated to poor equity returns over the next 7-10 years, odds are they will trail the longer term averages.

{kind=link}

As suggested above, many institutional retirement plans have an assumed rate of return built in to their asset/liability equation. Given that 10-year bonds yield less than 2.0% currently, and the chart above would indicate equities may return 3% to 5% (nominal), assumptions of 7% to 8% annual returns for a blended portfolio seem out of reach. While anything can happen, and often does, today’s low interest rate environment (courtesy of global central bank financial repression policies) will continue to penalize savers of all stripes.

Be Opportunistic

Despite the less than stellar backdrop for today’s investor, all is not lost. With market volatility comes opportunity. There are, and will continue to be, asset classes and sectors within asset classes that are for one reason or another mispriced. The patient, analytical investor can avail themselves of these opportunities (as we endeavor to do every day here at Nottingham) when they present themselves. This may mean selling out of a position when prices get ahead of themselves, or diving into a once-dreaded asset class when it gets sufficiently cheap.

We’re watching a few things today that have piqued our interest and should they cheapen up a little more, one may find them in their portfolio. If I were an owner of utilities, or heavily weighted towards the consumer staples sector, I would be very cautious right now – perhaps even to the point of booking some profits. Valuations have become a bit frothy in these sectors and while many of the companies represented here are world class, they remain just too expensive given the low growth environment we’re in. In a mean-reverting world, areas such as Europe and emerging markets look very attractive right now.

Interest Rates

We touched all-time lows on both the Treasury 10-year note and 30-year bond recently. The reasons for this include global central bank quantitative easing, little global growth, low to no inflation and a flight to safety triggered by Brexit and other geopolitical issues. During most of my time as a bond trader, the 30yr Treasury yielded between 5% and 8%. Never would I have believed the yield would drop as low as 2.1%! Then again, with over 40% of the world’s sovereign debt sporting negative yields right now, 2% must seem like a king’s ransom to investors in Japan and the Eurozone.

Our last letter touched on the limits of monetary policy and our belief that we have effectively reached them. It will now be up to Congress to enact some fiscal policy – whether it be infrastructure spending or tax reform – in order to revive growth here in the US. The bond market is currently priced for perfection and any hint of inflation or stronger than expected growth will likely be met by higher interest rates and material losses on longer-dated bonds. Investors should resist the temptation to chase yield and stay patient, focusing on municipal bonds in the 5-7 year range.

Conclusion

Low return environments can be extremely frustrating for investors, especially after 7 years of a bull market. Right now, both US bonds and stocks are near all-time highs, yet investor enthusiasm appears non-existent. Too many macro concerns I guess. With unemployment at 4.9% here in the US, the housing market looking up, and a hint of modest wage inflation in the offing, the US remains the cleanest shirt in a hamper full of dirty ones. Some of the other dirty shirts, however, just might prove more wearable over the next 5 years, but for today, we suggest sticking with the US.

The summer months are notoriously volatile given vacation schedules, thinly traded markets and trading desks staffed by junior associates. At Nottingham, we’ve banned our staff from summer vacations.

Just kidding, they’re actually allowed a day or so. Nonetheless, our efforts are geared toward finding that price dislocation or alpha opportunity wherever it may exist. We owe it to our clients. So as we muddle through this investment purgatory, remember to be patient, remember what got us to this point, and look to embrace volatility. Our fate has yet to be determined, and despite the rhetoric and rancor around the November election, don’t for a minute believe all the negativity.

The U.S is as strong economically, militarily and technologically as it has ever been and will continue to be a world leader for generations to come. Invest accordingly.

Larry Whistler, CFA, is President/Chief Investment Officer at Nottingham Advisors, a participant in the ETF Strategist Channel.