Note: This article appears on the ETFtrends.com Strategist Channel

By Rod Smyth

As active managers, we need the courage to make judgments about the future of market returns and the humility and processes to manage the size of our positions. Currently, we are positive about stocks and corporate bonds relative to cash, and we believe non-US stocks offer better risk-reward strategically and tactically, (i.e. over the next five to seven years, and also over the next year). Risk management is often about increasing or reducing the size of a position because the odds have changed, even if one still believes the outcome will remain the same. Last week, we responded to a change in the odds of the UK remaining in the EU by reducing overall portfolio risk and our exposure to Europe specifically. Following our trades, we still believe our portfolios are still positioned to benefit if the UK remains in the EU. Thus, we have chosen to go into the vote with less riding on the outcome.

We set out our views on Brexit previously in the article Should I Stay or Should I Go. We concluded the UK would stay, but articulated the risks. With the vote set for this Thursday, June 23, swing voters in the UK are starting to indicate how they might vote, and the probability of the UK remaining in the European Union went down last week, as measured by three things:

- A number of polls swung towards a lower chance of the UK remaining in the EU, with many now around 50:50 and thus giving no guidance. Polls have solidly favored staying until recently.

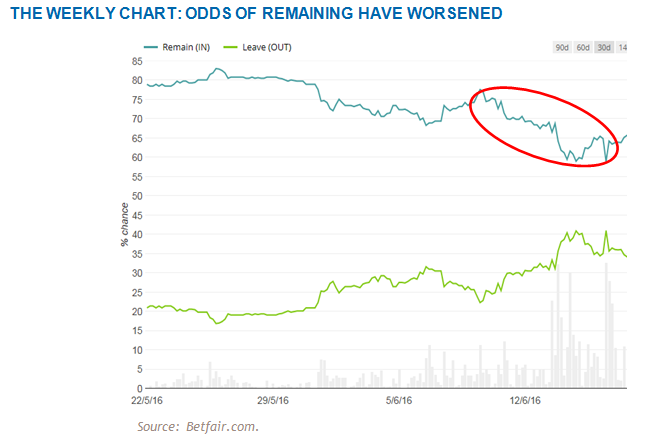

- The odds offered by bookmakers to those wanting to bet on the outcome also changed meaningfully. On June 9, UK bookmaker Betfair had the odds of remaining in the EU at 77%, by the 16th the odds were down to 59%. People betting money on the result are still saying it is more likely that the UK stays, but they are becoming less confident.

- UK and European stocks have fallen over the same time frame, and volatility has increased.

Our allocation to European stocks has never been about taking a position on this vote, but we have always recognized that the result would have a potentially significant impact on markets. We like European stocks because we believe an economic recovery is taking hold that is not fully reflected in stock prices. We have chosen to hedge out more than half our Euro exposure as we still see the potential for currency weakness.

With the odds of Brexit changing, and some of our European positions falling below levels we had ear-marketed as risk triggers, we decided to act. We sold some of our unhedged European exposure and bought long maturity US zero coupon bonds, (known as “strips” because they are stripped of the interest payment). These bonds rise and fall in price with even small movements in interest rates, and thus offer the prospect of price gains should Brexit occur and US interest rates fall.

Due to the price volatility of zero coupon bonds and their sensitivity to interest rates, a relatively small amount can change a portfolio’s risk structure and so using them helps to minimize turnover. Furthermore we believe their price will rise more following an exit than it will fall should the UK remain, offering favorable risk-reward in our view.

{kind=link}

This chart from Betfair.com (a UK website) shows how gamblers are betting on the outcome of the referendum. We have generally found betting exchanges to be more predictive than opinion polls. We believe this is because opinion polls can be influenced by the pollsters’ questions and voters’ opinions, whereas an exchange like this shows how people are betting money, regardless of what they think should happen. The chart above begins on May 22 and goes through last Friday, June 17. The red oval shows just how much less confident those betting on Remain have become relative to those betting on Leave. We are unable to forecast political outcomes, so repositioning our portfolios in light of this and other data seemed prudent to us.