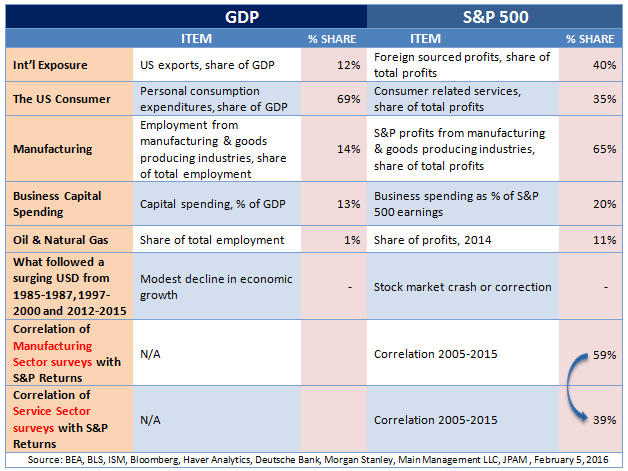

Furthermore it’s a common refrain that two thirds of GDP is driven by the consumer. Various data sources bear this out highlighting that, in fact, personal consumption makes up a 69% of the economy. By contrast consumer related services are almost half this figure as a percentage of S&P 500 earnings at 35%.

Accordingly factors that significantly move the economy appear to have a far lesser impact on equity market profits. To underscore the point the higher correlation of Manufacturing Sector surveys to S&P 500 profits (59%) again points to a greater impact that Service Sector inputs with a correlation of just 39%.

Another key element to note is the currency impact on S&P earnings. Given manufacturing’s influence on corporate profits it is noteworthy that this sector tends to be more influenced by a strong dollar. As the greenback surges, US goods appear more expensive in foreign markets, while overseas goods feel more affordable stateside. So while US exports are a mere 12% of GDP, foreign sourced profits are a considerably larger 40% share of S&P earnings.

{kind=link}

There remains little doubt that the economic factors that drive GDP clearly influence corporate earnings. However it’s important to identify the sectors with a more meaningful impact on each metric. The role of manufacturing on corporate earnings may be underappreciated by investors at their peril.

If the Fed does raise rates more than once during the balance of 2016 foreign buyers, seeking relatively higher yields than the sovereign debt of most developed nations, may look to accumulate more US Treasuries. If that does occur this could bring about further dollar strength. As such this could be an important factor in S&P profits for the balance of 2016 and is certainly worth watching.

Hafeez Esmail is the Chief Compliance Officer at Main Management, a participant in the ETF Strategist Channel.

A pioneer in managing all-ETF portfolios, Main Management LLC is committed to delivering liquid, transparent and cost-effective investment solutions. By combining asset allocation insights with smart implementation vehicles, Main Management offers a unique approach that translates into distinct advantages for our clients, including diversification, tax awareness and cost efficiency. http://www.mainmgt.com