Throughout the 1980s, 1990s and 2000s, many financial plans were constructed with the assumption that the portfolio could produce enough income to allow for 4 to 5% annual withdrawals during retirement. Over the past 35 years, interest rates have fallen around the globe and today bond yields are too low to meet a typical 4-5% annual withdrawal from a retirement portfolio.

Today the ten year U.S. Treasury bond yield is around 1.9%; ten years ago this yield was about 2.5 times higher and was around 5%¹. Of course an investor can stretch for higher yield, but this invites additional and often unintended risks; whether it be credit risk, maturity or duration risk and/or other unforeseen portfolio threats such as liquidity and issuer concerns.

Today’s dividend yields are also at relatively low levels compared to historical payout rates. The current dividend yield of the S&P 500® Index is 2.1% compared to the long term average of 4.4%². With both interest and dividends rates so low, how do we as an industry meet our client’s retirement living needs? We believe the answer is a Total Return strategy.

The concept of using total return to meet retirement income needs is relatively simple. One starts by combining the dividend and interest income from the portfolio and supplementing this with, usually modest amounts of, capital gains. If executed properly over time, the combination of the two can create adequate income, positions the portfolio to keep up with inflation and maintains a more stable asset base over time.

Equity returns over short time periods have, and likely will, vary widely. Since 1945 the long term annual growth rate for the S&P 500 has averaged about 7.2% before dividends³. We are going to be more conservative and assume equities will grow at 6.0% per year over time. The 6% annual growth over time (CAGR) is split into two with each half being assigned a different task: 3% will be used for supplemental income and the other 3% will be tasked to grow and keep up with inflation.

What about equity risks?

All markets, especially equity markets, undergo periods of failure. To account for this risk, we further recommend two additional policies to complete this overall strategy:

First, we would mandate 2-3 years’ worth of income needs to be invested in cash and ultra-short bonds so when markets do fall, such as during 2008-09, there is sufficient cash available to meet client income needs during these downturns. Knowing that there is a secure income source that is not exposed to typical market volatility

helps mitigate client anxiety and helps prevent additional drawdowns when the investment’s prices are depressed.

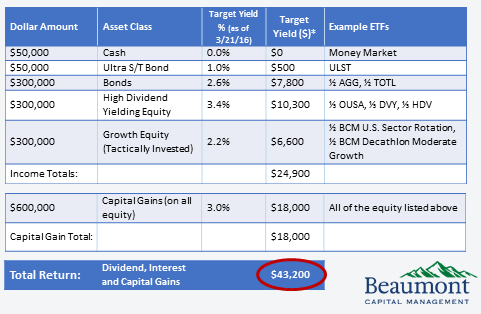

As an example, let’s use a $1 million portfolio, and a $40,000 annual income need which is 4% of the portfolio. If the portfolio were to drop 30% to $700,000, the same $40,000 would represent a 5.7% withdrawal. Given the historical 2-3 year time period that most bear markets have lasted, the markets would be well on their way to recovery and our portfolio’s stock and bond principal would still be intact and poised to recover. Having this cash reserve allows the investor to leave the portfolio alone during the bear market and assumed recovery period.

Second, for the equity portion of the portfolio, we would recommend investing a portion in tactical vs. strategic management. Using tactical management as a piece of the portfolio allows part of the equity allocation to avoid at least a portion of the drawdowns that occur during bear markets. This can shorten recovery time and reduce client anxiety even further, and keeps the client from making emotional buy and sell decisions.

As an example, the table below uses a $1 million hypothetical portfolio, a 4% annual income need and assume investing in low cost, long only ETFs to represent each asset class to show how this would work:

{kind=link}

The example has 2.5 years of income allocated to either a money market or ultra-short bond ETF; while $300,000 of the portfolio is allocated to other bond ETFs. Of this, the example would recommend investing ½ passively in a low cost bond index ETF such as the Barclay’s Aggregate Bond Index ETF (AGG) and ½ in an actively managed bond ETF, such as the SPDR DoubleLine Total Return Tactical ETF (TOTL), where the manager has the ability to seek additional alpha during most bond market environments.

Next the example invests $300,000 in three passive, high dividend yielding equity ETFs: OUSA, O’Shares FTSE US Quality Dividend ETF; DVY, iShares Select Dividend ETF; and HDV, iShares Core High Dividend ETF. Multiple ETFs are intentionally used to diversify from over reliance on one asset class such as Utilities or REITs. Each ETF follows a different index and together they could produce a dividend yield that is more than 50% higher than the S&P 500. This core equity allocation does much of the heavy lifting…it is positioned to grow over time and should provide an elevated income stream for the client.

[related_stories]Finally, the $300k Growth Equity allocation could be equally invested into two tactical growth ETF strategies. Of course we are biased and have used two of our strategies which we know well. However, you could use other tactical strategies that seek to provide defense when markets struggle. The purpose here is to show the benefit of diversification using one ETF strategy that is tactically constrained to the sectors of the S&P 500 and the second being a tactically unconstrained, global growth strategy. Tactical strategies can be selected where the defensive mechanism used by each can vary. For example a tactically constrained sector strategy may use cash for a defensive position while a tactically unconstrained, global growth strategy may remain fully invested and rely on geographical and asset class selection to try to avoid failing markets. The idea, in general, is to seek diversification by using multiple, actively managed portfolios.

The results of this sample portfolio construct shows numerous advantages. The portfolio is a 60% equity/40% fixed income portfolio. It has exposure to both international and domestic bond and equity. While the portfolio above is tilted to large cap equity, all market caps can be used in the allocation. Thirty percent of the portfolio has the ability to be defensive during periods of market failure and 2.5 years of income are in more conservative positions to help ensure clients can take their withdrawals without compounding the negative effects of a bear market. The portfolio is designed to meet both current and future income needs by allowing for growth to counter the effects of inflation. Most importantly, this total return construction should smooth out portfolio drawdown and volatility when compared to an all equity portfolio, allow the client to remain invested, and help them avoid making emotional buy/sell decisions at the worst possible times.

David Haviland is a Managing Partner and Portfolio Manager at Beaumont Capital Partners, a participant in the ETF Strategist Channel.

1 Source: U.S. Treasury

2 Sources: S&P 500, Investopedia.com

3 Source: DQYDJ.net

* The Target Yield % are based on the average 30-day yield for the ETFs listed within each category as of the date provided. The yield for the BCM strategies is based on the positions within the strategies as of the date listed.

This material is provided for informational purposes only and should not be taken as investment advice. Each client has their own unique circumstances and the investment themes described above may not be appropriate for all investors but rather seeks to illustrate the Total Return concept in portfolio construction. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. Any conclusions or assumptions described are to illustrate potential benefits, however are not guaranteed. The information presented is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

Beaumont Capital Management (BCM) is a tactical ETF strategist and use the ETFs listed above when investing its strategies. Several ETF families were included to illustrate there are a number of choices and countless combinations of ETFs that can be used to implement the Total Return concept. BCM is not recommending any ETF, or ETF family over another.

Past performance is no guarantee of future results. Diversification does not ensure a profit or guarantee against loss. An investment cannot be made directly in an index.

Sector investments concentrate in a particular industry and the investments’ performance could depend heavily on the performance of that industry and be more volatile than the performance of less concentrated investment options and the market as a whole. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments include interest rate and inflation risks. All investments have inherent risks including principal risk.

The Standard & Poor’s (S&P) 500® Index is an unmanaged index that tracks the performance of 500 widely held, large-capitalization U.S. stocks. Indices are not managed and do not incur fees or expenses. “S&P 500®” is a registered mark of Standard & Poor’s Financial Services, LLC a division of McGraw Hill Financial, Inc.

Beaumont Capital Management is a separate division of Beaumont Financial Partners, LLC. All rights reserved. Copyright © 2016.