Master Limited Partnerships[1] (MLPs) are primarily companies that build pipelines connecting oil and natural gas extractors to refiners and distributors. In a steady economic/oil price environment, they can be thought of as “toll roads” for the energy industry.

Coming out of 2008, MLPs went through a significant period of generating income and capital for their owners. However, when oil prices began their steep decline in August 2014, the price of the popular Alerian index of MLPs also fell dramatically.

Riverfront Investment Group believe MLP investors (including ourselves for a time) made some key errors in assessing the value and stability of the assets during this time. Having been out of the sector for the past eight months as prices have continued to fall, Riverfront Investment Group believe we now have a better understanding of how to assess MLPs. As a result, last week Riverfront Investment Group invested in the sector again across all our balanced and growth portfolios.

Understanding mistakes made in valuing MLPs

Riverfront Investment Group believe the primary mistake that was made in valuing the assets was the use of cash yields as the basis of determining value, and the belief that the cash distributions would be safe in almost any oil price environment since they were just “toll roads.” The reality has been very different.

As oil prices have fallen and borrowing costs have escalated (pipelines are built with borrowed money, largely in high yield debt), companies have had to reduce their distributions, creating a “value trap” for investors using those metrics.

Unfortunately, MLPs’ position as a high-yielding investment in a low interest rate world has led to them being used in a lot of retail portfolios, and even led to leveraged products being created in closed-end funds. The declines in prices have precipitated a series of panicked sales in the past year, and many MLPs are now being forced to cut those cash distributions that investors expected.

The market volatility of the past several weeks has frightened a lot of market participants, and it has created the opportunity to buy attractive assets at discounted prices – so called “distressed assets.” Riverfront Investment Group believe MLPs fit this profile. One of the risks of buying immediately after a large price decline is that, rather than the price decline being an overreaction of panicked sellers, it is actually a fair warning of the increased risk of the business being unable to operate profitably in the future. This is a classic example of a “value trap”.

In the interest of avoiding these value traps, Riverfront Investment Group try to look at distressed assets with a jaundiced eye, seeking to ensure that we understand why the asset has fallen and whether the fundamentals of the company underneath the asset pricing are sound, and then applying a rigorous stress test of the current valuation to make sure that we believe the security is worth buying even if the market continues to be volatile. We believe that MLPs now pass this test, and we wanted to summarize the work we did and the conclusions we came to that led us to make that call.

Our recent analytical approach differed from the way in which many market participants value MLPs in that Riverfront Investment Group focused on the core drivers of the business rather than cash flow yields, and then we stressed these valuation assumptions under fairly adverse oil price environments.

At current prices, Riverfront Investment Group believe that MLPs are trading at 25% discounts to historic valuations based on relatively pessimistic assumptions about future oil prices. The key to whether this is value or a trap lies in our stress test and our understanding of the business fundamentals.

Our stress testing assumes oil stays sub-$35 for a considerable period of time, and that many companies pulling oil out of the ground will face bankruptcies, which will lead to substantial restructurings of the revenue contracts for the oil-based pipelines.

Even in a scenario like this, Riverfront Investment Group believe that the underlying businesses would present an attractive valuation; however, for reasons outlined below, we believe many of the inputs in our stress test are potentially overly pessimistic.

Riverfront Investment Group have asked and received a lot of questions in doing this research and thought we would ask and answer them below.

- Are MLP’s driven by oil prices or not?

It’s complicated, and our best answer is, “Directly, no. But indirectly, yes”. Pipeline leases to oil extractors (known as Exploration & Production, or E&P’s) are based on oil volume and have minimum volumes baked into them to protect the MLPs. As oil prices have fallen, expectations of future oil volume have fallen. As many of the companies that are running oil through the MLPs have faced pressure due to low oil prices, investors have feared that pipelines’ revenues will suffer if energy companies go bankrupt. This fear has raised borrowing costs and further reduced earnings expectations. All of these indirect effects have greatly affected the price of MLPs.

- What is likely to happen in a bankruptcy of an E&P?

Whether there is a bankruptcy or sales of assets by a troubled E&P, the MLP contract is likely to carry with the assets and the new owner will likely have lower debt service. This would make it easier for the new owner to pay for MLP services. MLPs are typically listed as critical vendors through bankruptcy proceedings, which keeps oil flowing. Riverfront Investment Group chose to downplay this advantage in our stress test to be conservative.

- How much of the MLP space has this “indirect” oil exposure?

Luckily, only about 30% of pipelines in the US transport oil from extractors to refiners. Approximately 50% of the pipelines in the US transport natural gas and about 20% of pipelines transport processed oil from refineries, business lines that have seen volume and revenue growth during this volatile period. This is a great source of stability in our stress scenario.

Signs That Indicate the Tide Might Be Turning

Riverfront Investment Group have begun to see that MLPs have positive returns even on days when dividends cuts are announced in companies, which we interpret as a sign that the market has now better understood the relationship between MLPs and oil prices. We are also expecting an increase in pipeline M&A activity in 2016 driven by underperformance, cheap valuations, and low oil and natural gas prices as well as interest from large, value-driven institutional investors.

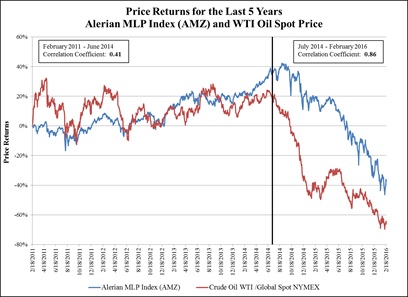

The following chart illustrates price returns for the Alerian MLP Index and WTI Oil Spot Price over the last 5 years. As the chart depicts, the correlation between oil prices and the Alerian MLP index have increased considerably since oil’s precipitous decline, beginning in July of 2014.

{kind=link}

Adam Grossman is the Chief Global Equity Officer and Scott Hays is the Quantitative Portfolio Manager at Riverfront Investment Group, a participant in the ETF Strategist Channel.