Our stress testing assumes oil stays sub-$35 for a considerable period of time, and that many companies pulling oil out of the ground will face bankruptcies, which will lead to substantial restructurings of the revenue contracts for the oil-based pipelines.

Even in a scenario like this, Riverfront Investment Group believe that the underlying businesses would present an attractive valuation; however, for reasons outlined below, we believe many of the inputs in our stress test are potentially overly pessimistic.

Riverfront Investment Group have asked and received a lot of questions in doing this research and thought we would ask and answer them below.

- Are MLP’s driven by oil prices or not?

It’s complicated, and our best answer is, “Directly, no. But indirectly, yes”. Pipeline leases to oil extractors (known as Exploration & Production, or E&P’s) are based on oil volume and have minimum volumes baked into them to protect the MLPs. As oil prices have fallen, expectations of future oil volume have fallen. As many of the companies that are running oil through the MLPs have faced pressure due to low oil prices, investors have feared that pipelines’ revenues will suffer if energy companies go bankrupt. This fear has raised borrowing costs and further reduced earnings expectations. All of these indirect effects have greatly affected the price of MLPs.

- What is likely to happen in a bankruptcy of an E&P?

Whether there is a bankruptcy or sales of assets by a troubled E&P, the MLP contract is likely to carry with the assets and the new owner will likely have lower debt service. This would make it easier for the new owner to pay for MLP services. MLPs are typically listed as critical vendors through bankruptcy proceedings, which keeps oil flowing. Riverfront Investment Group chose to downplay this advantage in our stress test to be conservative.

- How much of the MLP space has this “indirect” oil exposure?

Luckily, only about 30% of pipelines in the US transport oil from extractors to refiners. Approximately 50% of the pipelines in the US transport natural gas and about 20% of pipelines transport processed oil from refineries, business lines that have seen volume and revenue growth during this volatile period. This is a great source of stability in our stress scenario.

Signs That Indicate the Tide Might Be Turning

Riverfront Investment Group have begun to see that MLPs have positive returns even on days when dividends cuts are announced in companies, which we interpret as a sign that the market has now better understood the relationship between MLPs and oil prices. We are also expecting an increase in pipeline M&A activity in 2016 driven by underperformance, cheap valuations, and low oil and natural gas prices as well as interest from large, value-driven institutional investors.

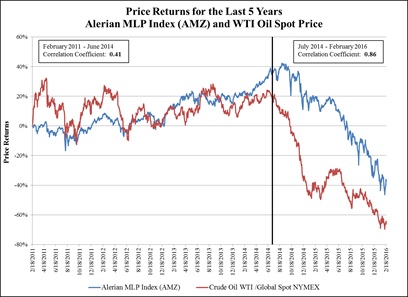

The following chart illustrates price returns for the Alerian MLP Index and WTI Oil Spot Price over the last 5 years. As the chart depicts, the correlation between oil prices and the Alerian MLP index have increased considerably since oil’s precipitous decline, beginning in July of 2014.

{kind=link}

Adam Grossman is the Chief Global Equity Officer and Scott Hays is the Quantitative Portfolio Manager at Riverfront Investment Group, a participant in the ETF Strategist Channel.

Source: FactSet Research Systems. Past performance is no guarantee of future results. The Alerian MLP Index is the leading gauge of large- and mid-cap energy Master Limited Partnerships (MLPs). The float-adjusted, capitalization-weighted index, which includes 50 prominent companies and captures approximately 75% of available market capitalization, is disseminated real time on a price-return basis. It is not possible to invest directly in an index.

Important Disclosure Information

Master Limited Partnerships (MLP) investing includes risks such as equity- and commodity-like volatility. Also, distribution payouts sometimes include the return of principal and, in these instances, references to these payouts as “dividends” or “yields” may be inaccurate and may overstate the profitability/success of the MLP. Additionally, there are potentially complex and adverse tax consequences associated with investing in MLPs. This is largely dependent on how the MLPs are structured and the vehicle used to invest in the MLPs. It is strongly recommended that an investor consider and understand these characteristics of MLPs and consult with a financial and tax professional prior to investment.

Buying commodities allows for a source of diversification for those sophisticated persons who wish to add this asset class to their portfolios and who are prepared to assume the risks inherent in the commodities market. Any commodity purchase represents a transaction in a non-income-producing asset and is highly speculative. Therefore, commodities should not represent a significant portion of an individual’s portfolio.

In a rising interest rate environment, the value of fixed-income securities generally declines.

RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation.

RiverFront Investment Group, LLC, is an investment advisor registered with the Securities Exchange Commission under the Investment Advisors Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). Any discussion of the individual securities is provided for informational purposes only and should not be deemed as a recommendation to buy or sell any individual security mentioned. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

Index Definition:

The Alerian MLP Index is the leading gauge of large- and mid-cap energy Master Limited Partnerships (MLPs). The float-adjusted, capitalization-weighted index, which includes 50 prominent companies and captures approximately 75% of available market capitalization, is disseminated real time on a price-return basis.

Copyright © 2016 RiverFront Investment Group. All rights reserved.

[1] Master Limited Partnerships (MLP) investing includes risks such as equity- and commodity-like volatility. Also, distribution payouts sometimes include the return of principal and, in these instances, references to these payouts as “dividends” or “yields” may be inaccurate and may overstate the profitability/success of the MLP. Additionally, there are potentially complex and adverse tax consequences associated with investing in MLPs. This is largely dependent on how the MLPs are structured and the vehicle used to invest in the MLPs. It is strongly recommended that an investor consider and understand these characteristics of MLPs and consult with a financial and tax professional prior to investment.