{kind=link}

Recent retirees with low non-portfolio income and high early expenses are particularly vulnerable to sequence risk.

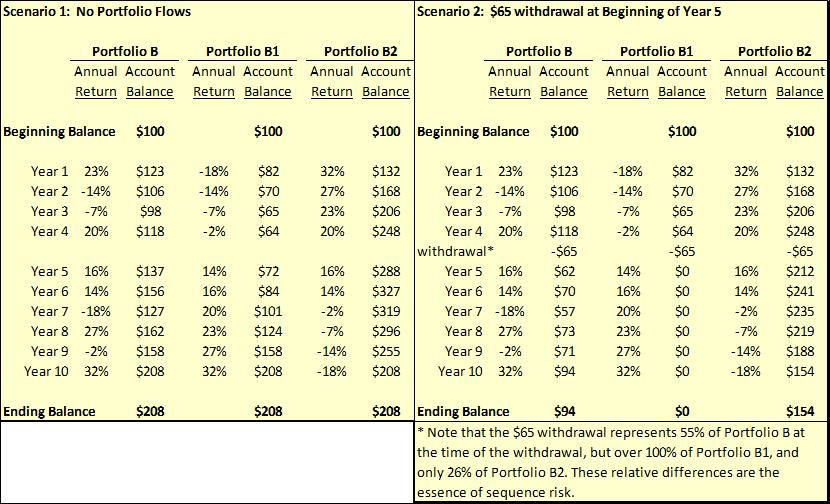

There are a few ways to mitigate sequence risk. One is to have no flows — deposits or withdrawals — into or out of the portfolio (as in Scenario 1). However, this is patently unrealistic for most investors. Another way is to successfully avoid making withdrawals for a time after a significant decline in the portfolio’s value. This might be accomplished by keeping a sizeable cash reserve outside the portfolio to cover this contingency. However, the size of the reserve necessary to achieve meaningful immunization against contingencies of unknown frequency and severity may be so large that the long-term “cash drag” on performance may outweigh the benefits, as a number of studies in the financial literature have demonstrated.[1]

The most productive way to control sequence risk is to not have an erratic series of returns — the more stable the return stream, the less the sequence risk. A perfectly smooth return stream, such as that of Portfolio A in first example, has precisely zero sequence risk. (This is a given, since all sequencings of identical periodic returns are indistinguishable from each other.) It does not matter when deposits or withdrawals occur in such a portfolio. While no practical RMI technique can totally eliminate return volatility, every step in that direction adds value from a sequence risk perspective.

The value of stability in mitigating sequence risk should be clear and can be quantified using the approach we have outlined.

There are likely many questions you have about RMI, including those we posed earlier in this series. How can RMI actually provide equity risk management? At what cost? Is the cost so high and/or the upside potential of equities so diminished by RMI that it is not cost-effective over a full market cycle? What would an RMI-infused portfolio look like, and what would its risk/return profile be? We will address these questions in future installments. As always, we encourage your feedback along the way.

Jerry Miccolis is the Founding Principal and Chief Investment Officer at Giralda Advisors, a participant in the ETF Strategist Channel.

This material is for informational purposes only. Nothing in this material is intended to constitute legal, tax, or investment advice. Investing involves risk including potential loss of principal.

Giralda Advisors, located in New York City, is an asset management firm that focuses on providing risk-managed exposure to the equity markets with a goal of limiting asset depreciation during both protracted and catastrophic market downturns while allowing substantial asset appreciation in up-trending markets. The Giralda Advisors team welcomes your inquiries. Please call (212) 235-6801 or visit us at http://www.giraldaadvisors.com/

[1] See, for example, “Sustainable Withdrawal Rates: The Historical Evidence on Buffer Zone Strategies” by Walter Woerheide and David Nanigan, Journal of Financial Planning, May 2012; and “Research Reveals Cash Reserve Strategies Don’t Work… Unless You’re A Good Market Timer” by Michael Kitces, Retirement Planning, June 2012.