If one were to name two innovations that have had the biggest impact on the average investor over the last decade or two, the answer would probably be ETFs and target date funds.

Hardly a blip on the radar screen 20 years ago, both have grown into trillion dollar ideas. Both provide diversification and liquidity in a simple, straightforward manner.

However, the growth of target date funds has primarily been in defined contribution plans, whereas ETFs are used by a much wider audience.

Given the prevalence and importance of target date funds to the average worker’s retirement plan, it is worth asking just how well target date funds have delivered on their promise.

Sadly, results have been less than impressive. Below we see a risk-return plot of several “vintages” of Morningstar Target Date funds category averages.

While the risks do increase as one goes from conservative portfolios to aggressive portfolios, what has been lacking is a corresponding increase in returns. Given the low rates of savings by most Americans, annualized returns in the 5% range are unlikely to get them to a comfortable retirement.

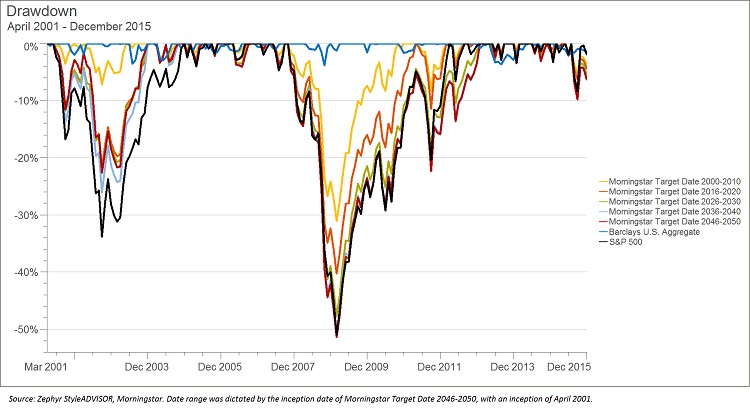

Of particular concern has been performance of target date funds during bear markets. The yellow line shows the peak-to-trough losses on the average target date fund of the vintage 2000-2010.

{kind=link}

In theory, a fund in this classification would be appropriate for an individual in or near retirement during the first decade of the new millennium. And yet when the financial crisis of 2007-09 hit, target date funds in this vintage lost almost a third of their value.

Eventually these funds did recover their losses, but it seems unlikely anyone in the distribution stage of their life cycle would be comfortable with losses of that magnitude.

{kind=link}

First, most target date funds have a “buy and hold” mentality, where changes to the allocations are typically driven by the changing demographics of the investors rather than market conditions.

Systematic risk, or market risk, is simply the price of admission for target date funds. The assumption is the investor has a risk tolerance level high enough or a time horizon long enough to shoulder market risk. Second, most target date funds neglect to invest in any kind of “alternative” strategies, investing primarily in plain vanilla asset classes, in a long-only fashion.

We would argue that target date funds can and should do more for their shareholders. Moreover, we believe that ETFs are a great tool for improving the risk/return profile of target date funds. Two of the often-cited advantages of ETFs are 1) ability to provide liquid access to new, distinct asset classes and styles and 2) ability to short the market.

Both of these traits are frequently lacking in most target date mutual funds, which tend to direct the majority of their assets to traditional, long-only mutual funds. In addition, most target date funds are subject to “capture”, meaning that most or all of their assets tend to be invested solely in the mutual funds offered by a single fund family.

Of course, simply sprinkling a few new ETFs into a target date fund’s allocation isn’t a cure-all. If they are to bring any diversification value to a target date fund the portfolio manager needs to be sure the new ETFs are truly uncorrelated to existing positions.

See our previous article, Diversity Doesn’t Always Equal Diversification. Also, the risks of inverse funds, especially leveraged versions, have been widely documented. Unlike the end investors of target date funds, a target date portfolio manager using these kinds of ETFs cannot follow a “set it and forget it” strategy.

One exciting development, flying somewhat under the radar in terms of public awareness, is the development of collective unit trusts (CITs). CITs are legally prohibited from doing mass advertising, but according to Morningstar, there is over $300bn in CITs. Although CITs are broadly set up along the same risk-return spectrum as target date funds, they do offer some advantages. CITs are sponsored by a bank, trust, and/or a third party investment advisor, so they are less prone to the “capture” problem where a portfolio is comprised solely of funds from a single mutual fund family. The wide-open universe of ETFs can be used when constructing CITs.

We believe a more robust approach towards market risk, utilizing the best tools available, is needed if target date funds are to provide the kinds of returns required for baby boomers as they head into retirement.