Still, we are seeing some early signs that the slowdown of economic growth in China may be bottoming, though we think that growth is far below the official numbers, and the collapse of economic activity in Brazil is starting to get less worrisome. Therefore, we are becoming more confident that emerging markets will likely not be a complete disaster going forward.

The Chinese government has been working hard to stimulate their economy through a number of measures, such as increased lending and a reduction in their required bank reserves. These measures will take time to bear fruit, but the situation is beginning to look more stable. Slowing growth in China and the large debt overhang reminds us of Japan in the early 1990s. An aging demographic, a lot of bad debt, and an infrastructure overbuild may result in slow growth in China for years to come. However, that is not necessarily terrible for U.S. investors. For example, Japanese economic growth peaked in the early 1990s and then declined, but the 1990s were also a very good period for U.S. growth and stock price appreciation.

{kind=link}

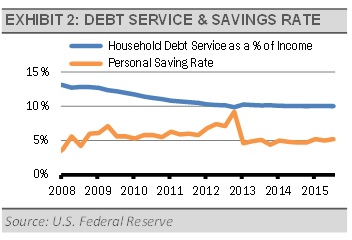

Even if there is a global economic shock, our financial system is much better prepared to absorb risk today than it was prior to 2008. For example, the U.S. household debt service ratio, the amount necessary to cover current debt payments as a percentage of disposable income, is lower today than at the beginning of 2008. Additionally, the savings rate is higher.

Meanwhile, U.S. banks are better able to withstand a global shock as their balance sheets are stronger and exhibit less leverage. One measure of risk in the banking system is the Tier 1 capital ratio. The higher the ratio, the stronger the bank. In 2008, the Tier 1 capital ratio for the U.S. banking system was roughly 10% compared to today’s level of roughly 13%. The current, higher ratio reflects less risk. Overall, we think U.S. financial system is in better shape and potentially more stable than in 2008.

In our view, the current environment looks similar to the early 1990s, when the financial markets stumbled due to a global economic slowdown, followed by a long period of U.S. expansion. Please see our 2016 Outlook for further explanation of our near-term caution and long-term optimism.

Gary Stringer is the CIO, Kim Escue is a Senior Portfolio Manager, and Chad Keller is the COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.