{kind=link}

Source: Giralda Advisors analysis of Bloomberg data

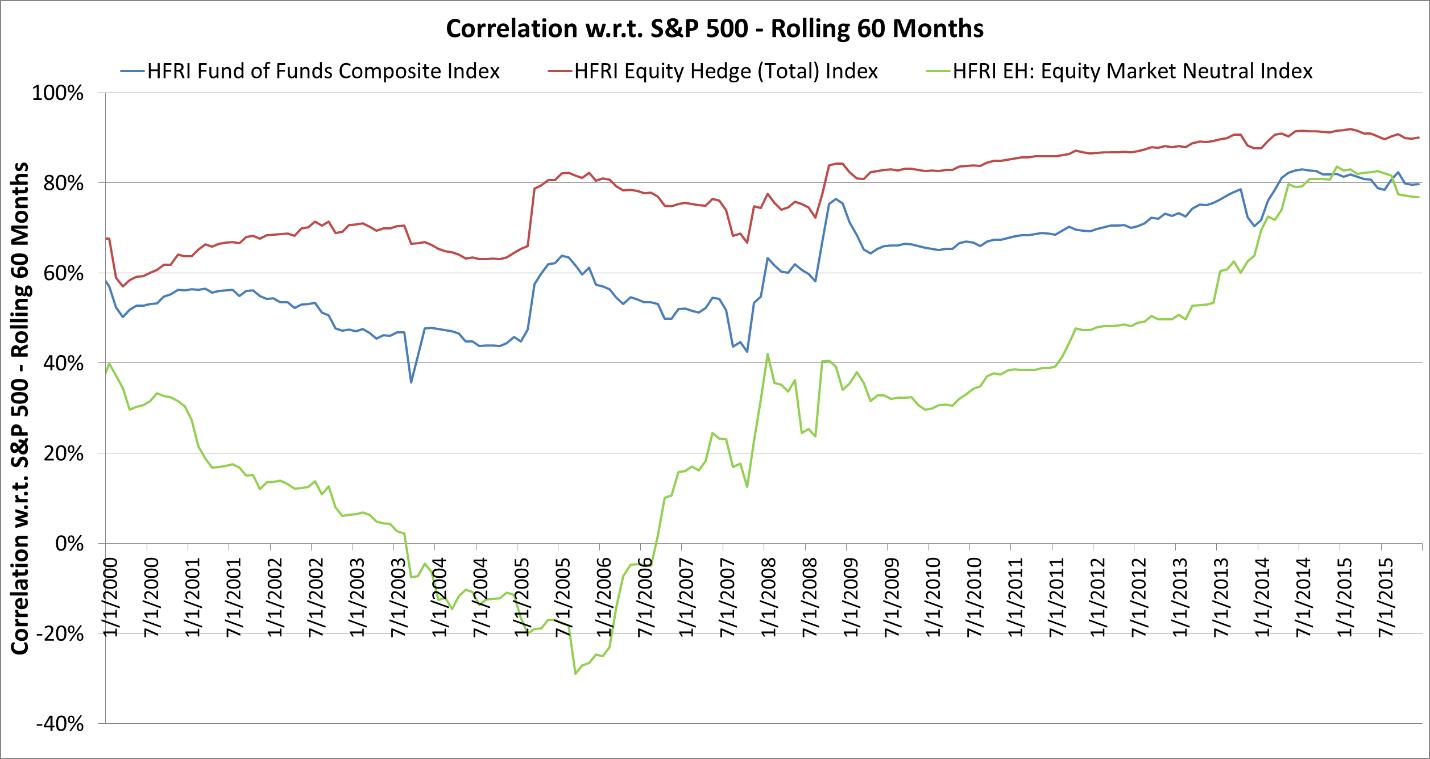

Here again, the picture is disturbing. The correlations have trended upward over time into the neighborhood of 80% to 90%. To the extent that portfolio managers are relying on liquid alts to buffer the risk of equities in client portfolios, it would appear from this evidence that the asset class has failed to deliver. This erosion of diversification benefit is even more concerning to us than the erosion of return when we consider the portfolio problem. Making matters more pressing for advisors is the fact that clients have become quite vocal in their impatience with the poor performance of hard-to-explain investments that do not appear to be doing their fundamental job of portfolio risk reduction.

Enter RMI, the Risk-Managed Investing approach we introduced earlier in this series. Recall that the objective of RMI is to embed downside risk management explicitly into the equity investment itself. This, as we have pointed out, makes the portfolio less reliant on non-equity asset classes to do this job and attacks the portfolio problem more directly, right at its source. We submitted that the implications of this are paradigm-shifting and may change the way we think about portfolio construction, noting that “80/20 could be the new 60/40,” with RMI investments in the 80% portfolio component replacing part of the conventional equity exposure that constitutes the traditional 60% component.

For those investors not yet prepared to shift their portfolio-construction paradigm in this way (as promised, we’ll be delving into RMI in much more detail later in this series), let’s simply consider an RMI investment in direct “competition” with a liquid alt investment. If a portfolio manager considers successful a liquid alt strategy that delivers two-thirds of an equity return with half the volatility, then how might said manager regard RMI? A successful RMI strategy would deliver near-100% of an equity return and the volatility it removes would be the “bad” (i.e., downside) volatility. RMI would thus appear to be a category-killer in the liquid alt space.

In addition to exploring RMI’s broader potential to inspire the rethinking of portfolio construction, future installments in this series will investigate RMI’s role in mitigating “volatility drag” and “sequence of returns risk,” calibrate its tolerable cost, and discuss its implementation. We trust you will continue to find this discussion thought-provoking, and we look forward to your feedback along the way.

Jerry Miccolis is the Founding Principal and Chief Investment Officer at Giralda Advisors, a participant in the ETF Strategist Channel.

This material is for informational purposes only. Nothing in this material is intended to constitute legal, tax, or investment advice. Investing involves risk including potential loss of principal.

Giralda Advisors, located in New York City, is an asset management firm that focuses on providing risk-managed exposure to the equity markets with a goal of limiting asset depreciation during both protracted and catastrophic market downturns while allowing substantial asset appreciation in up-trending markets. The Giralda Advisors team welcomes your inquiries. Please call (212) 235-6801 or visit us at http://www.giraldaadvisors.com/