For several years now there has been a hotly contested debate among investors regarding equity market valuation. We often hear that the U.S. equity market is overvalued because the current P/E (Price/Earnings) ratio (16.5) is above the long term average (15). Some prefer to look at the Cyclically Adjusted P/E ratio (CAPE) which is even further above the long-term average. Other models indicate that Equities are fairly valued or even cheap at current levels.

The most important distinction between these models, and their results, is whether they take current interest rates into account or not. Models that disregard interest rates such as the CAPE, also known as the “Shiller P/E”, suggest we should expect low-to mid single digit (3-5%) returns per annum over the next 10 years since the P/E based on 10 year real earnings is higher than the long-term average.

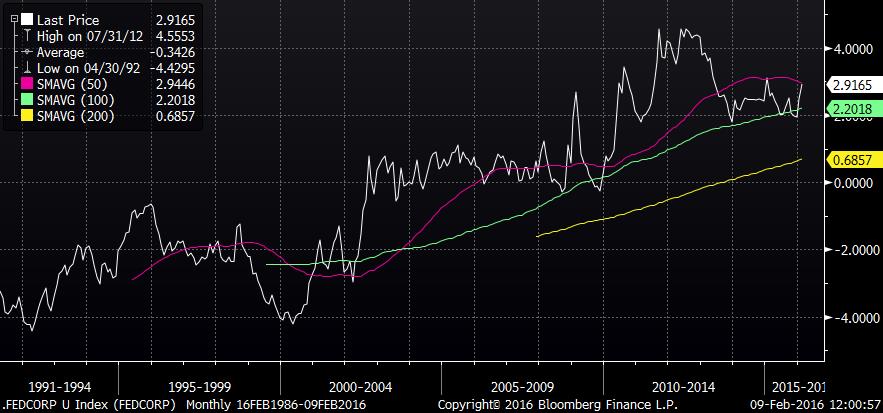

Other models relate the current earnings yield (inverted P/E) for the S&P 500 Index to nominal or (preferably) real treasury or corporate bond yields. These models suggest that equities are somewhat cheap, in particular relative to the last 25 years. The average ex-ante (forward-looking) spread between the S&P 500 Index earnings yield and corporate bond yields since 1991 has been a negative 34 basis points (see chart below) and we are now (Feb 9, 2016) at a positive 2.91%. So, in other words, for the last two and a half decades equity investors were, on average, happy to earn a lower earnings yield than they could have gotten in the corporate bond market, but in the last few years they have demanded a much higher earnings yield than corporate bonds.

The average is of course skewed by readings of more than negative 4% in 1992 and again during the end-stage of the Dotcom boom in 1999/2000, but the example illustrates that equities still look attractive versus corporate bonds at current yield levels.

{kind=link}

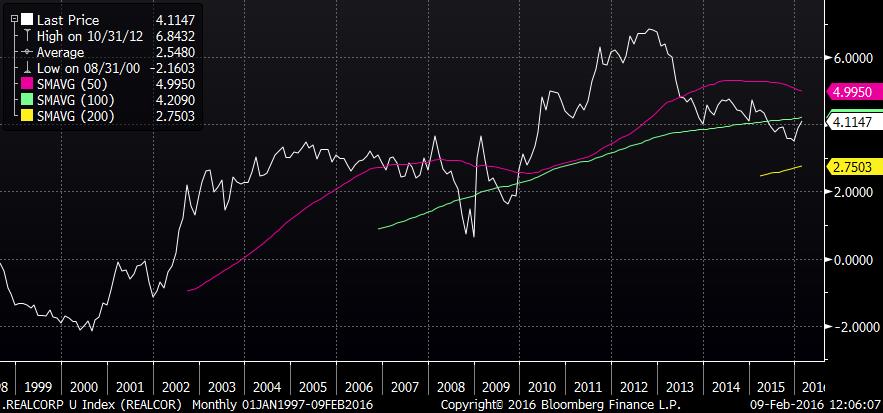

Another perspective can be had by comparing the equity earnings yield with corporate bonds on a real (after inflation) basis. If we assume that corporate earnings increase in line with inflation over time, then it makes more sense to compare them to bond returns after deducting inflation, since bond coupon payments are fixed.

The chart below shows the spread, in real terms, between A-rated Industrial Bonds and the Earnings Yield on the S&P 500 Index. The extreme values observed were -2.16% in August of 2000 and + 6.84% in October 2012. We are currently at + 4.11%. This chart only goes back to 1998 since it uses TIPS prices to determine the forward-looking real yield.

{kind=link}

While the above models are versions of the so-called “Fed Model”, which in its original form relates the earnings yield to the nominal yield on Treasury Bonds, the key distinction in both examples is the use of Corporate Bonds instead of Treasuries. This allows us to think about the spread as the cost of alternative forms of capital from the corporation’s perspective. Imagine that you are the CFO of a large corporation with a single-A rating and faced with the possibility of issuing debt to buy back stock in your company. If the P/E on your stock is, say 15, the corresponding earnings yield would be 1/15 or 6.67%. Since this is an after-tax number, it corresponds to roughly 10% before tax. Since interest is tax deductible this is the earnings yield that should be compared to the marginal cost of debt financing, which would be roughly 3.1%. In other words, there is a 690 basis point arbitrage gain, in nominal pre-tax terms, from issuing debt to purchase outstanding stock. In real terms, the spread is even wider, since earnings are likely to follow inflation while the Interest on the bonds is fixed. This goes a long way towards explaining why corporations are issuing debt to buy back their own shares.

So in conclusion, taking current low bond yields into account, the Equity market does not appear to be overvalued. Rather, it looks to offer a significant yield cushion versus the corporate bond market.

Jan Erik Wärneryd is a Senior Portfolio Manager at Hillswick Asset Management, a participant in the ETF Strategist Channel.