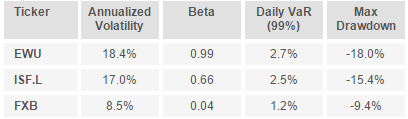

Another important reason to consider local currency denominated ETF is the possibility to purify exposures. Looking at risk parameters of EWU calculated on a freely available investor resource utilizing 12 months historical data, it appears that the fund’s annualized volatility was 18.4%, whilst its beta against SPDR S&P 500 ETF (NYSEarca: SPY) almost equalled to 1.

However, if we look at ISF.L in isolation, it turns out that the underlying index actually has a bit lower volatility and is substantially less dependent on S&P 500. I have included Guggenheim CurrencyShares British Pound Sterling Trust (NYSEarca: FXB) in the table below as a proxy for GBPUSD.

{kind=link}

Source: InvestSpy

The fact that relationship between FTSE 100 and S&P 500 is not so close is further confirmed by correlations, which show that ISF had a coefficient of only 0.58 as opposed to 0.80 of EWU.

This means that an investment in FTSE 100 has more potential to offer diversification benefits to a US investors than it may appear at the first sight. Not surprisingly, the well-known and documented home country bias among investors only gets aggravated when market participants look at distorted statistics.

Not only investing in local currency denominated ETFs gives a clearer picture of the underlying index, but it also forces an investor to make a conscious decision about the FX risk. In contrast, using a US listed ETF for international exposure leaves the investor with a convenient alternative of not doing anything. As documented by behavioural economists and Nobel Prize winners Kahneman and Tversky, “opt in” vs “opt out” questions can lead to completely different outcomes.

Systematic models

Finally, for investors that rely on quantitative or technical analysis, it is important to distinguish whether their models are suitable for stocks, FX, or both. A moving average on SPY is not the same thing as a moving average on EWU because the latter is effectively a wrapper for both equities and FX components. If your model has been tailored for equities, ILS would be a more appropriate choice with the FX decision left as a standalone issue.

Conclusion

The aim of the article was to offer a different perspective into international investing via ETFs. Using the case of the UK, I have illustrated that in some cases a local currency denominated ETF listed outside the US can be a better way to achieve the desired exposure. One reason for this is that some foreign ETFs are cheaper and larger than their US counterparts. Another important point is that using a local currency denominated fund purifies exposures arising from the underlying index and foreign currency.

One point of caution though is the tax treatment of investments in funds domiciled abroad. Every investor should assess their individual circumstances as part of the decision making process. But if your tax situation does not preclude you from investing in ETFs listed abroad, such an approach may bring more transparency to your portfolio. It is a rare feat in the world of finance nowadays.