Given the unprecedented shifts impacting the bond markets, we have talked a lot about the need to rethink fixed income holdings, and in my last post, I discussed three potential strategies that investors could follow to prepare portfolios for an unconventional rising rate environment.

In this blog post, I want to drill down on what we mean when we talk about rethinking the core—or disaggregating the Barclays US Aggregate Bond Index (Agg)—and why it may be time to build portfolios that are better suited to weather the new fixed income environment.

The tide is turning

Over the past 30 years, many investors have done well with investments that tracked broad fixed income benchmarks such as the Agg. But the Agg has become vulnerable and investors who stick with it may find it’s an unseaworthy vehicle for navigating rising rates, economic growth and higher inflation.

Here’s why:

Going back to 1985 the Agg has returned 7% while rates on the 10-year Treasury fell from 10% all the way to 2.3% today.1 Additionally, the Agg’s yield-to-worst has fallen in similar fashion. In this environment, it is increasingly difficult to use a standard bond portfolio to generate the kind of returns, let alone income, that many investors require.

The Agg also represents a narrower slice of the fixed income market than bond investors realize, and it excludes an important source of much recent growth—high yield corporate bonds. At the same time, its market-cap-weighting means it’s tilted to the biggest investment grade issuers, which include the lowest-yielding and most rate-sensitive sectors of the market.

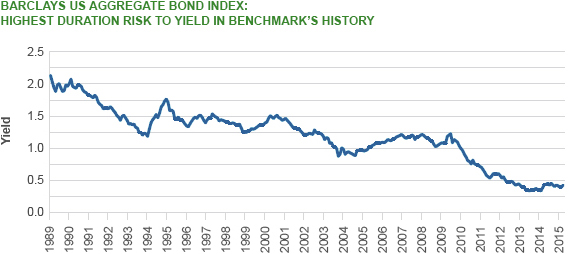

Meanwhile, the Agg’s duration has lengthened, pushing the index to its highest ratio of duration risk to yield since the index’s inception in 1986.2 That means today’s Agg, as shown in this chart, reflects a historically elevated level of duration risk for a relatively low level of yield.

{kind=link}

Source: Bloomberg, State Street Global Advisors, as of 6/30/2015. Past performance is not a guarantee of future results.

Reconstruct your core

To potentially compensate for the Agg’s diminished risk-return profile, investors may be well served by supplementing their core exposure with less-traditional fixed income asset classes. But this may have unintended consequences if a portfolio’s credit risk exposure is increased beyond a client’s preferred comfort zone.

The research team at SPDR ETFs and SSGA Funds believes the time has come to disaggregate the Agg and reassemble core fixed income portfolios that may be better suited for today’s environment. This involves rearranging the Agg’s components—overweighting some, underweighting others—and adding in core-like exposures to certain fixed income asset classes that aren’t currently covered in the index.