With the final numbers for the second quarter of 2015 now available, the research firm ETFGI today brought some long-anticipated news: the size of the exchange traded funds market has finally exceeded that of its older, more well-to-do cousins. It may have taken a little longer than we expected, but ETFs are now a bigger part of the market than hedge funds.

In order to explain why hedge funds might be losing out in the race for assets, we thought we would re-examine the challenge of replicating hedge fund performance. When it comes to individual hedge funds, which are typically unconstrained by assets, leverage or geography, replication is a difficult objective. When it comes to a broad hedge fund portfolio, replicating performance is easier than you might think.

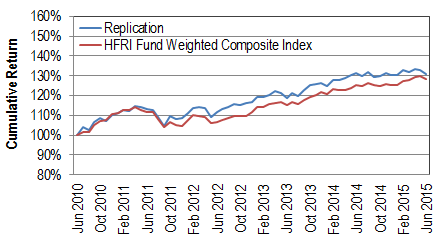

To begin the replication process, our “hedge fund” is going to invest half its money in U.S. bonds, and the remainder in global equities. (We’ll use the S&P U.S. Aggregate Bond index to represent the first portion and the S&P Global 1200 for the second.) Assuming we also rebalanced on a monthly basis, here’s how our hedge fund would have performed over the past five years. For purposes of comparison, we also show research firm HFR’s benchmark of hedge fund performance. The HFR Fund-Weighted Composite Index includes funds which are no longer open to new investors, so it is a fair representation of what only the largest and best-connected asset owners may have available to choose from:

Sources: S&P Dow Jones Indices, HFR as of 30th June, 2015.

The pattern of returns seems similar, which is encouraging. And our decision to allocate to equities and bonds in equal proportions means that the overall return from our replication strategy is much higher. Well done us!

But congratulations are premature. Our replication strategy does not include costs, or fees. The replication costs of broad-based, passive indices are de minimis, but we should not undervalue our unique insights (we are replicating a hedge fund, after all). A fee of 1.50% per annum seems reasonable, and we’ll take 15% of any profits (provided we’re at least breaking even over the past 12 months). Here’s how our performance looks now: