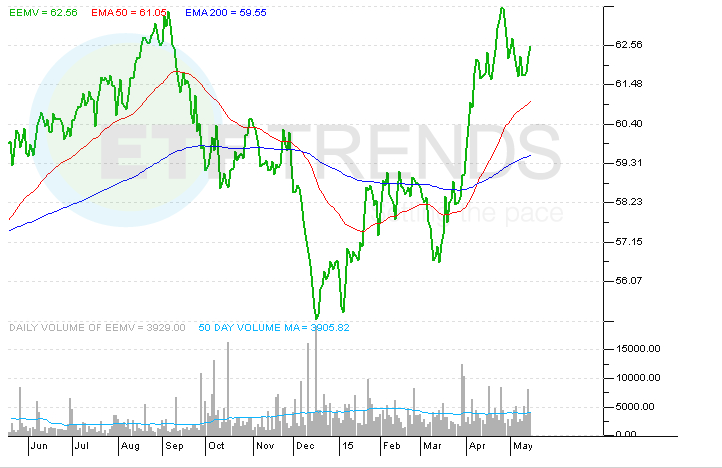

Although emerging markets stocks have bounced back this year, EEMV’s out-performance of EEM and superior risk-adjusted returns relative to VWO are not surprising.

“Historically, low-volatility stocks have outperformed high-volatility stocks over the long term. This “volatility anomaly” was first discovered in 1968 by financial economist Robert Haugen, who theorized that behavioral factors were behind this phenomenon. More specifically, investors tend to chase risky stocks, expecting these companies to deliver higher returns. This drives up stock prices of riskier, which ultimately results in weaker future returns relative to less-volatile names,” notes Morningstar.

Low volatility takes on a different meaning at the sector level with EEMV than it does with equivalent U.S.-focused ETFs. For example, EEMV’s combined consumer staples and utilities weight of 22% does not exceed the almost 27% the ETF devotes to financial services stocks. However, when combining EEMV’s weights to bank stocks, utilities, energy and materials names, the ETF does present some risk from state-controlled enterprises. [Ditching State-Run Companies in a new ETF]

“Record-low interest rates in the developing world during the past few years have helped drive strong portfolio flows into emerging-markets assets. A sudden reversal in flow, because of a sudden spike in market volatility or weakening macro fundamentals in the emerging world, could hurt both asset prices and currencies and drive short-term volatility in this fund. Like most foreign-equity funds, this exchange-traded fund does not hedge its foreign-currency exposure,” notes Morningstar.

iShares MSCI Emerging Markets Minimum Volatility ETF

{kind=link}

Tom Lydon’s clients own shares of EEM.