First, some quick ground rules. This article will not attempt to make a bond market forecast. It will, however, attempt to show how interest rate hedging can be an important alternative to short duration or floating rate bonds (whether they represent a long term position or represent a tactical position in a rising rate environment). Investing in bonds with “average” duration—say, 5-10 years—and hedging the interest rate risk by shorting Treasury bonds or futures of similar duration can substantially offset interest rate risk while delivering higher yields than short-term instruments.

The alchemy of the credit term premium

It is of course impossible to buy long-duration Treasurys, hedge out the interest rate risk, and have a yield in excess of T-bill rates. That’s why we feel hedging the interest rate risk of a position in the Barclays US Aggregate Bond Index—an index comprised of roughly 1/3 U.S. Treasurys—is not necessarily effective. After all, hedging has a cost, so hedging U.S. Treasurys simply recreates cash, at a cost.

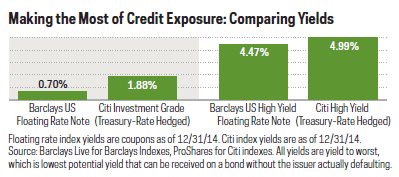

How is it, then, that one could invest in longer duration investment grade and high yield bonds, hedge out the interest rate risk, and have a yield in excess of floating rate instruments? The alchemy here comes from the credit term premium, which—all else being equal—is the spread between Treasury and non-Treasury securities. Credit spreads are generally wider for longer duration bonds. So, even after hedging out interest rate risk, the yields on interest rate hedged investment grade and high yield bonds of “average” duration have been higher than their floating rate counterparts.

That’s not a risk-free proposition, of course. Movements in credit spreads could be proportionally larger for bonds of “average” duration than they’d be for bonds of shorter duration or floating rate instruments. Additionally, there’s a cost associated with hedging, and any hedge has the potential to fail. Still, it is a compelling source of additional yield—one that is often sought by credit arbitrage hedge funds but is also achievable through an index-based approach.

Divorcing credit exposure from interest rate exposure

Another benefit of this approach is that it separates the credit exposure decision from the interest rate exposure decision. Many investors have been conflating the two of late, most obviously by investing in bank loans. While the floating rate aspect of bank loans can reduce interest rate exposure, bank loans are, by and large, below investment grade. Many investors have likely unwittingly increased credit exposure through these investments.

{kind=link}