Meanwhile, on the supply side, global coal producers show no signs of cutting back as while oil prices helped cut input costs and depreciating currencies help offset some of the lost coal revenue.

“Australian mines are in a relatively strong position compared with higher cost suppliers—particularly those in the U.S.—which are at much greater risk of closures this year,” according to Wood MacKenzie.

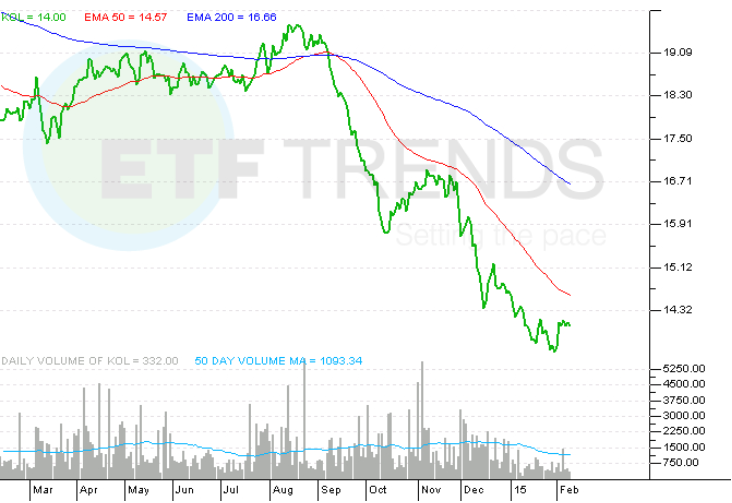

KOL includes a heavy 34.7% tilt toward U.S. coal producers, along with a 10.9% weight in Australian companies.

Market Vectors-Coal ETF

{kind=link}

For more information on the coal industry, visit our coal category.

Max Chen contributed to this article.