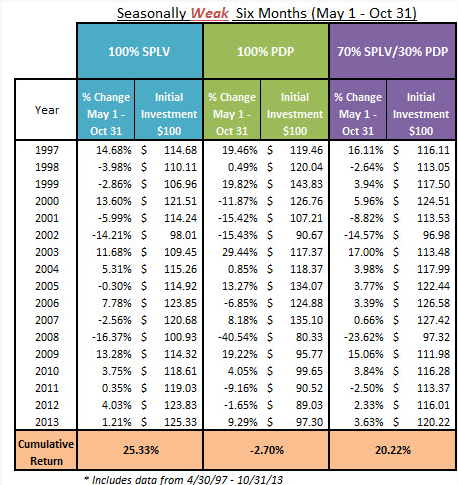

“The SPLV has generally provided greater returns during the seasonally weak six months (cumulative of 25.33% since 4/30/1997) than the PDP (-2.70%). However, the SPLV has notably lagged the return of the PDP during the seasonally strong six months, up 127.08% compared to 597.42%, respectively. Therefore, a 30% PDP/70% SPLV split during the seasonally weak six months has seen a cumulative return of 20.22%, while a 70% PDP/30% SPLV split during the seasonally strong six months has seen a return of 435.8%, according to Dorsey Wright.

A 10-year backtest running through April 17, 2014 shows the PDP/SPLV switching strategy generated averaged annualized returns of almost 7.1%, nearly 200 basis points better than the S&P 500 over the same time. The three-year standard deviation on the PDP/SPLV strategy was just under 10% compared to almost 12.4% for the S&P 500, according to Dorsey Wright data. [An ETF Strategy for the Best Six Months]

The strategy is not a holy grail. For example, U.S. stocks were strong during the seasonally weak period last year, leading to 3.63% return for 70% SPLV/30% PDP portfolio when being 100% in PDP offered better than double that upside. However, the long-term track record is stout and the PDP/SPLV switch is a way for investors to stay involved in stocks during the weakest six months.

{kind=link}

Table Courtesy: Dorsey Wright & Associates

Tom Lydon’s clients own shares of IWM.