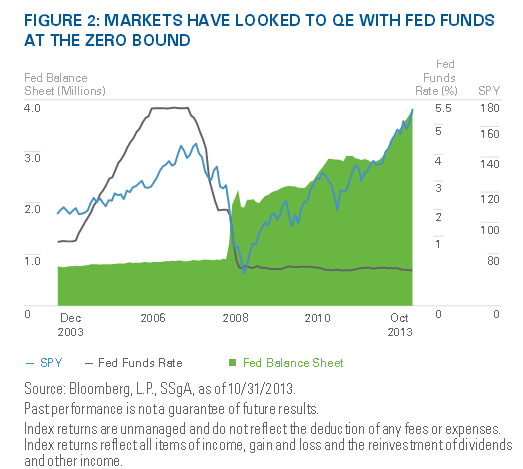

With Bernanke ending his term at the end of January, Yellen will be tasked with implementing and executing the Fed’s exit strategy from its great monetary policy experiment. The Fed’s balance sheet expansion under QE has been a powerful force in propelling equity markets to all-time highs, as illustrated in Figure 2. While tapering is not tightening in the traditional sense, market participants may want to brace for a period of consolidation now that markets have experienced a sizable re-rating with lackluster earnings growth thus far in 2013.

The S&P 500 Index has not traded below its 200-day moving average all year. Going forward, most believe that markets need to see greater signs of positive earnings growth for further gains. In a worrisome sign, earnings revisions are not terrible, but less than inspiring. In light of this, some investors are tempted to believe that we will likely see the end of the positive market run.

{kind=link}

However, we may simply be entering a new regime where investors are willing to assign a higher multiple to US equities due to the continued low inflation and other asset classes offering less attractive investment opportunities. With this tension between the short-term and long-term playing out, this means that investors may look outside of the US to see further gains, especially since the US has outperformed other countries and regions by wide margins.

While US earnings have recovered to pre-crisis levels, Europe has yet to do so. Stabilizing economic growth coupled with economic reforms and improved credit conditions may be the boost that European shares have needed. In addition, investors will do well to focus on using this as a chance to take on more targeted EM exposures. In 2013, EM economies grew four times faster than developed markets, but this gap will decrease to two times next year. Much of the outlook for emerging markets centers around China, which consensus expects to grow by 7.4% next year averting fears around a hard landing.

As China rebalances its economy to be less export driven, opportunities are arising to add targeted exposures to smaller companies with greater exposure to the growing middle class. Traditional fixed-income investors have seen some reprieve, but the Barclays U.S. Aggregate Index remains in the red year-to-date.

Thus, recent market moves are likely reflective of what the next couple of months may bring until the market begins to price in tapering again. With the long-term picture not changing much, investors may continue to migrate from traditional fixed-income exposures and focus on creating portfolios for today’s and tomorrow’s bondmarkets. Specifically, corporations remain attractively valued from a fundamental and technical perspective. Focusing on floating rate notes, short-term high yield bonds and senior secured loans may offer attractive current income with low interest- rate risk.