Still, XAR as enough leverage to the commercial aircraft business to benefit from significant order backlogs.

“Orders for new commercial aircraft are at historic highs due to airlines replacing aging fleets and/or expanding current fleets. In an effort to increase fuel efficiency, airlines are also retrofitting current fleets with more fuel efficient engines which is driving strong order flow among parts manufacturers and suppliers. This activity has created a large backlog of orders for the Aerospace industry segment, and offsets weakness in the Defense industry segment, which supports a bullish outlook for the industry,” said Mazza in an email exchange with ETF Trends.

Adding to the bull case for XAR is that aerospace and defense firms are part of the industrial sector, which is historically one of the better performing sectors at this time of year. Perhaps more importantly, industrials perform well when interest rates rise because rising rates can go hand-in-hand with economic growth. [Industrial ETFs: November Strong]

As Mazza points out, “the A&D industry has a beta of 1.9 to US GDP growth relative to the S&P 500’s beta of 1.7.”

XAR has a weighted average market cap of $21.8 billion, according to State Street data, but the average market cap in one of its rivals is close to $29 billion. The slight tilt toward small and mid-cap A&D names could benefit XAR because some of those names are less leveraged to the defense spending cycle.

“Going forward, earnings seem poised to increase as evidenced by the record aircraft orders announced at the recent Dubai Airshow,” said Mazza. “This may provide further support to share prices as investors seek out growth opportunities and, in fact, may benefit small companies that have less exposure to defense spending.”

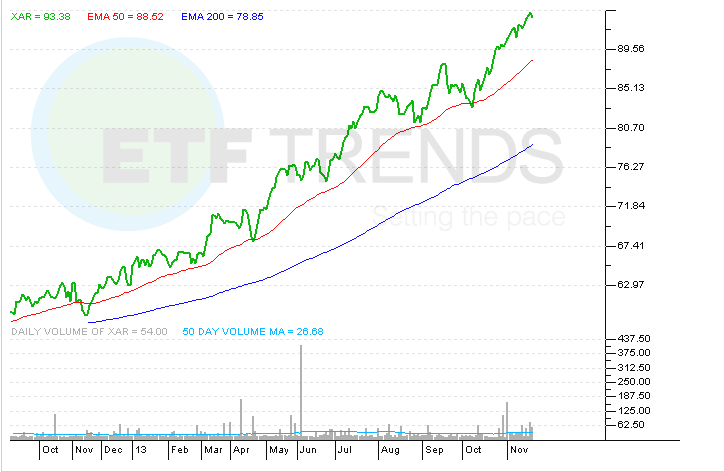

SPDR S&P Aerospace & Defense ETF

{kind=link}