{kind=link}

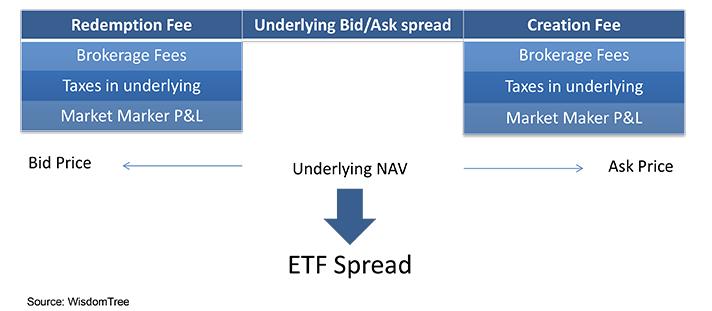

Again, this is a simple spread, and other costs will be considered in different scenarios. For example, if the underlying securities (the perfect hedge) are not open or accessible to the trader, they will then have to hedge with something else and thus incur risk from the imperfect/proxy hedge. That element of risk will be built into the spread, making it wider. Another cost that might be considered by a market maker when creating a spread is how long the position will be kept in inventory. If there isn’t a way to immediately liquidate it, balance sheet costs would then be included, because there is a cost to tying up cash of the firm.

It’s important to understand that a spread including the maximum cost scenario is for smaller on-screen quoted sizes. If a larger size is quoted, costs such as creation/redemption fees and balance sheet costs become a smaller part of the spread, and it is thus possible to get tighter markets for larger-size trades.

An ETF spread is a function of cost. The spreads in the marketplace are not arbitrary but a formulaic combination of maximum costs and market maker assessments of the probability of incurring those costs, which are constantly changing. As assets under management and volume increase, that probability decreases, and so does, usually, the width of the spread.

Anita Rausch is a Director on the Capital Markets team at WisdomTree Investments (NasdaqGM: WETF). This post was republished with permission from the WisdomTree blog.

The content of this post is relevant to institutional investors interested in trading ETFs in significant size. Individual investors do not always have access to liquidity providers to trade ETFs as referenced above.