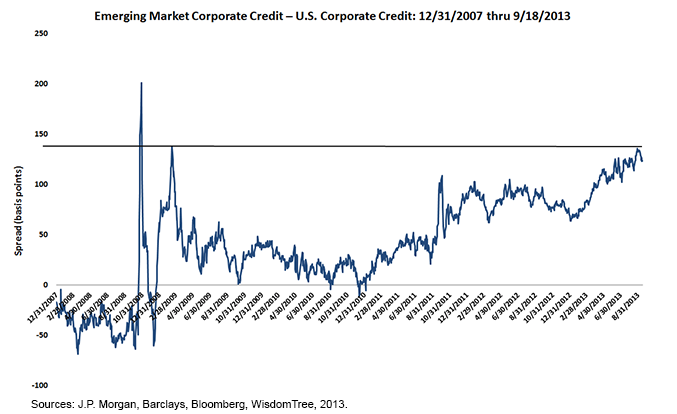

As shown in the chart above, credit spreads have generally trended lower over the last five years. With a recovering global economy and healthy corporate profits, companies posed less of a risk to lenders. After a momentary spike in September 2011 (caused by concerns in Europe), credit spreads continued to tighten through mid-2013. For much of this period, EM corporate spreads moved largely in concert with those of U.S. companies. However, due to a combination of moderating Chinese growth and better than expected U.S. data, yields in emerging market corporate bonds began to diverge. Even though spreads in U.S. credit continue to trade at or below their 12-month average, spreads in emerging markets have widened to 368 basis points, currently near their closest relative spread to U.S. high yield in history. Although emerging markets present an additional wrinkle for investors’, the narrowing of the spread between EM corporates (an asset class that is currently rated 69% investment grade1) to an all high-yield portfolio should have EM popping up on more investors’ radars. In perhaps an even more interesting development, the so-called “EM premium” is currently trading at levels not seen since the bottoming of the global financial crisis in early 2009.

{kind=link}

In the chart above, we compare a similarly rated composite of U.S. corporate bonds to the J.P. Morgan Corporate Emerging Markets Bond Index Broad. In the last week, the relative credit spread between emerging markets and the U.S. was trading at all-time wide levels. In our view this implies that either EM corporate bonds are undervalued or that U.S. credit is overvalued, at least when using credit ratings as a proxy for risk.

Overcoming the EM Stigma

Even though they understand the quantitative advantages of EM credit investing (higher yields for comparable credit quality businesses), the thought of lending to companies headquartered in a foreign country seems to cause some investors concern. However, just like equity investing, by limiting your investable universe to developed markets, you severely restrict your investment opportunity set (and the potential for declining correlations and excess returns). With EM lagging across virtually all asset classes this year, it might be trendy to decry the end of EM investing. But many of the companies represented in the EM corporate investable universe are multi-billion dollar, multinational corporations with significant track records and credit histories. The combination of solid fundamentals and above market interest rates due to their country of domicile could make for an attractive investment if investors can put their biases behind them.

While investor interest has been increasing in recent years, EM corporate credit comprises only 4% of the Barclays Global Aggregate Corporate Index.2 At current levels, EM corporate debt appears to be attractively priced compared to U.S. credit. Should investors believe in the long-term opportunity of emerging markets, EM credit may provide an attractive way to generate income in their portfolios while at the same time reducing volatility relative to traditional equity investments in these markets.

Rick Harper is head of fixed income and currency for WisdomTree Asset Management. This post was republished with permission from the WisdomTree blog.

1Source: J.P. Morgan, August 31, 2013.

2Barclays, August 31, 2013