Pension reform is gaining traction. It’s no secret that oversized pension burdens have been a drain on state and local governments. Even with improving stock markets, pension funded levels have languished. Ironically, the financial crisis brought the pension problem to the fore, and the hard work of addressing the issue has already begun. Between 2009 and 2011, 43 states enacted some sort of pension reform, according to the National Conference of State Legislatures. Detroit’s large pension burden added an exclamation point to the conversations, and may be the impetus for increased reform — and relief for overburdened municipalities. We cite the California city of San Bernardino as another potential precedent setter in our September market update, with some expecting an eventual Supreme Court decision before all is said and done. Ultimately, there seems to be a growing acknowledgement that achieving greater local budget flexibility will require a more aggressive approach to pension reform.

We are not Polyannas. We know the recent market correction has been painful for muni bond holders. The ugly truth, however, is that corrections are necessary. They restore value in the market and present the opportunity for investors to buy in at attractive levels — a new base from which your investment can grow. I think that is exactly what the market is doing here — recreating value from a point of very low, unsustainably low, interest rates.

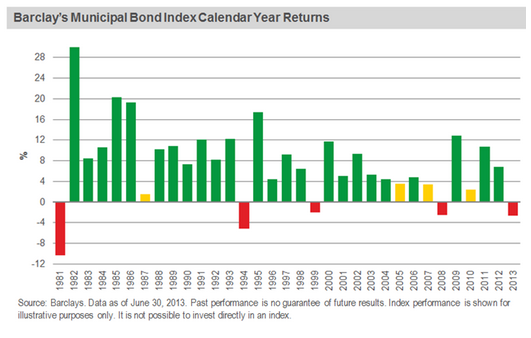

As illustrated in the chart below, over time, negative periods in the municipal market have been followed by boons. For those who are able to weather the near-term uncertainty, we think this may be a good time to capture muni exposure at levels not seen since 2011. The fundamentals in the overall municipal bond market are strong, and we believe the market will acknowledge that fact — and patient investors will be rewarded.

{kind=link}

Bonds and bond funds will decrease in value as interest rates rise and are subject to credit risk, which refers to the possibility that the debt issuers may not be able to make principal and interest payments or may have their debt downgraded by ratings agencies. A portion of a municipal bond fund’s income may be subject to federal or state income taxes or the alternative minimum tax. Capital gains, if any, are subject to capital gains tax.

Peter Hayes, Managing Director, is head of BlackRock’s Municipal Bonds Group.