Perhaps ironically, investors may need to look for their central bank-infused gains elsewhere. Consumer confidence in the Euro-Zone recently hit a 2-year high. Business confidence across manufacturing and service segments in Belgium reached its highest levels since February of 2012. What’s more, the European Central Bank (ECB) is maintaining an ultra-accommodating low rate stance; nobody at the ECB is thinking about tapering rates in the Euro-Zone.

The Euro-Zone is hardly out of the woods. Each of the economies for the PIGS (i.e., Portugal, Italy, Greece and Spain) is still shrinking. And record levels of unemployment rarely translate into increased spending. Moreover, if the U.S. Fed does travel the tapering path of slowing down its purchases of U.S. bonds, we may see Spanish and Italian yields climb back to unsustainable levels. Once more, the sovereign debt crisis abroad could come back to haunt.

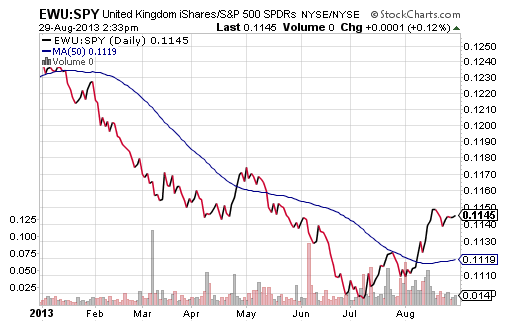

Nevertheless, there’s evidence to suggest that the performance of foreign developed markets (e.g., United Kingdom, Europe, etc.) relative to the U.S. have bottomed. Both the iShares United Kingdom (EWU):SPDR S&P 500 Trust (SPY) price ratio as well as the WisdomTree Hedged Europe Equity (HEDJ):SPDR S&P 500 Trust (SPY) price ratio favor the increasing relative strength of EWU and HEDJ.

{kind=link}

Keep in mind, the key will still be U.S. housing. If XHB cannot climb back above and stay above its long-term moving average (200-day), stock assets clear across developed and undeveloped markets are likely to suffer. Make sure that you have stop-limit loss orders on existing risk assets. If you’re looking to put cash to work, consider increments where you might make a purchase when the S&P 500 is 5%, 7.5%, 10% and/or 12.5% off an all-time record.

Gary Gordon is president of Pacific Park Financial, Inc.